Enterprise Products Rises 19% in a Year: Is it the Right Time to Buy?

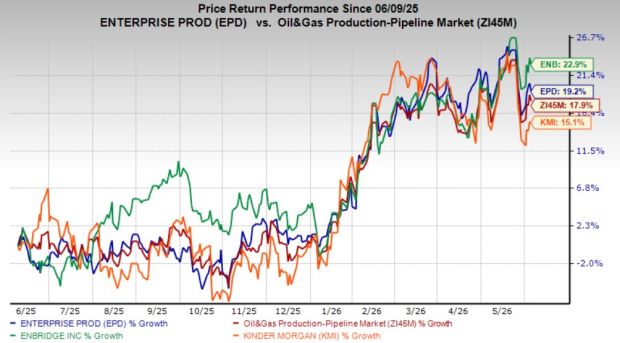

Enterprise Products Partners EPD units are trading close to their 52-week high of $40.17, closing at $37.81 on June 5. Over the past year, the EPD stock has gained 19.2%, outperforming the industry’s 17.9% growth. Shares of its peers, Kinder Morgan KMI and Enbridge Inc. ENB, have grown 15.1% and 22.9%, respectively.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The partnership owns and operates a midstream asset network that transports crude oil, natural gas, natural gas liquids and refined products across North America. It generates stable, fee-based revenues backed by long-term contracts that provide predictable cash flows.

While price performance demonstrates the attractiveness of a stock to some extent, it is prudent to closely assess the stock’s fundamentals before arriving at an investment decision.

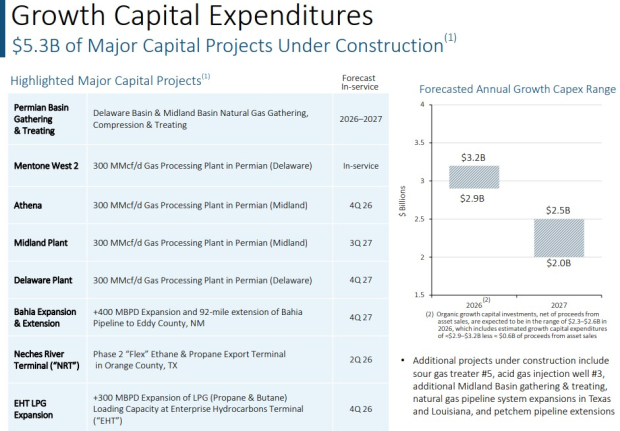

Enterprise’s Pipeline of Major Capital Projects

In its latest earnings presentation, Enterprise highlighted that it has major capital projects worth $5.3 billion under construction, which are expected to begin operations through 2026 and 2027. These growth projects are backed by favorable energy market fundamentals, including increased hydrocarbon production from the Permian Basin and higher natural gas demand from rising LNG exports and the rapid expansion of AI infrastructure.

The partnership anticipates U.S. oil production to reach 14.5 million barrels per day (BPD), while NGLs and natural gas production are expected to grow to 9.1 million BPD and 130.8 billion cubic feet per day (Bcf/d) by 2030, with the Permian Basin becoming one of the largest drivers of future volume growth. EPD has several growth projects under construction to capitalize on this trend, such as the Mentone West 2 processing plant and gas processing plants in Midland and Delaware, among others. Additionally, EPD has expansion projects under construction, which increase its ability to collect, transport and export hydrocarbons.

Since many of these projects are expected to enter service in 2026 and 2027, they should contribute to EPD’s earnings and cash flows, supporting increased profitability. The partnership generates stable, fee-based revenues that result in predictable cash flows across business cycles.

Image Source: Enterprise Products Partners L.P.

EPD’s Strong Financial Position Supports Returns to Unitholders

Enterprise has a strong balance sheet with nearly $3.3 billion in consolidated liquidity, which is comprised of liquidity available under its credit facilities and unrestricted cash on hand. The strong liquidity position enhances its financial flexibility and supports sustainable distribution growth. In the first quarter of 2026, the partnership announced a distribution of 55 cents per common unit, an increase of 2.8% year over year. This marks the partnership’s 27th consecutive year of distribution growth.

Additionally, Enterprise believes that its discretionary free cash flow could reach up to $1 billion in 2026 despite an increase in its growth capex. In the near term, the partnership plans to allocate free cash flows toward growing distributions, unit buybacks and debt reduction. EPD's robust liquidity and healthy free cash flow generation should enable it to capitalize on growth opportunities while prioritizing returns to unitholders and debt reduction, strengthening its balance sheet.

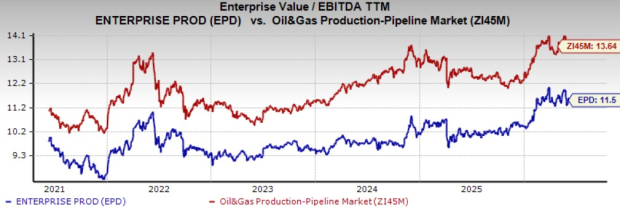

Valuation Snapshot

Considering the valuation snapshot, EPD is currently considered cheap on a relative basis. The stock is trading at a trailing 12-month Enterprise Value to Earnings Before Interest, Taxes, Depreciation and Amortization (EV/EBITDA) of 11.5x, which is a discount compared with the broader industry average of 13.64x. Notably, Kinder Morgan and Enbridge currently trade at a trailing 12-month EV/EBITDA of 14.07x and 17.3x, respectively.

Image Source: Zacks Investment Research

Final Verdict: Time to Buy or Hold?

Enterprise is expected to generate stable earnings and cash flows backed by its long-term contracts. The partnership’s pipeline of growth projects, backed by strong energy market fundamentals, should support higher earnings and cash flows in the coming years. Additionally, the partnership’s free cash flow growth should support sustainable distribution growth and opportunistic unit buybacks.

The EPD stock offers a compelling mix of stable returns and long-term growth potential. Given that the stock is currently undervalued, investors should consider buying the EPD stock, which carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).