Bay Street is full of junior bankers who weren’t even alive the last time Canadian capital markets had a year as slow as 2022.

The total value of new stock issues by companies last year fell 73 per cent to $14.4-billion from $52.7-billion in 2021, according to financial data service Refinitiv. While 2021 was a particularly strong year for Canadian equity capital markets, the 2022 total was also 64 per cent below the most recent 10-year average of $40.4-billion.

Tyler Swan hasn’t seen an annual figure that low since the 1990s.

“You’d have to go back in your database very far, probably 25 years or more, to see an absolute level of issuance as low as it was last year,” said Mr. Swan, the managing director and global head of equity capital markets for Canadian Imperial Bank of Commerce. “It is not just equity markets either, but bond markets, housing markets, and this has created an enormous amount of uncertainty about the direction of the economy.”

Government and corporate bond offerings were also down compared with 2021 levels, though corporate debt took a much more substantial dive as recession fears grew over the course of last year. Total debt offerings were down 18 per cent in 2022 to $198.3-billion from $240.9-billion in 2021, Refinitiv data show, but corporate debt fell much more sharply, by 29 per cent, to $62.7-billion last year from $88.3-billion the year before.

Merger and acquisition activity was down from 2021, though still resilient from a long-term perspective. Over all, however, continuing economic uncertainty and market volatility continue to generate a cloudy outlook for the year ahead.

Nitin Babbar, global co-head of equity capital markets at RBC Capital Markets, the top investment bank for stock deals in 2022, said issuance levels last year fell to “generational lows [and] represented the hangover from 10 years-plus of free money.”

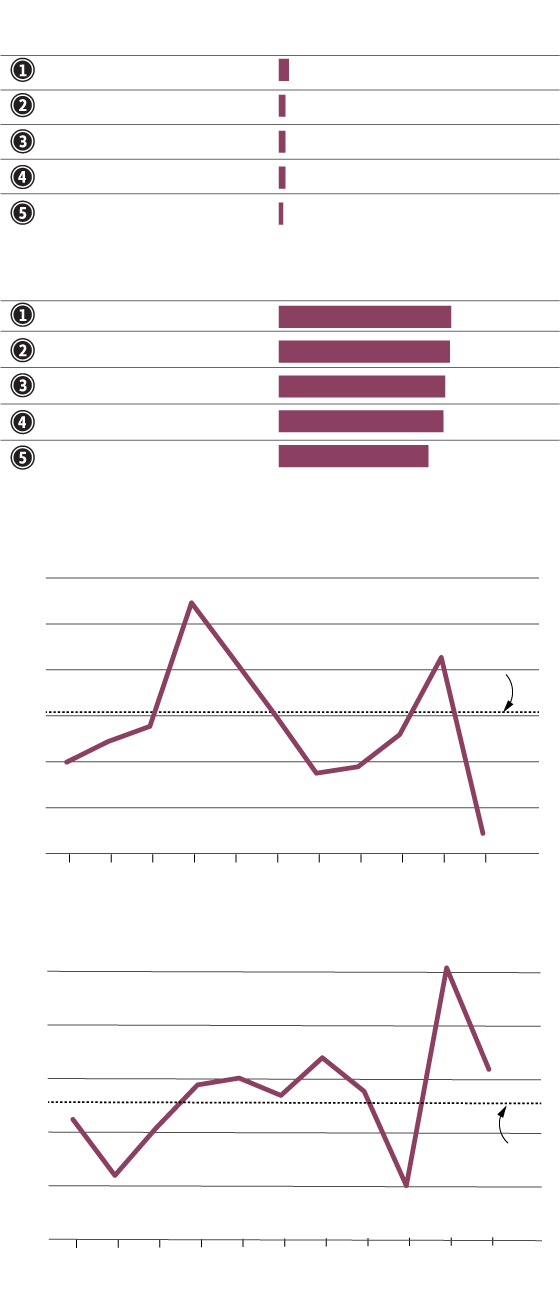

Top banks for equity underwriting

Rank

Banks

Value (billions)

No. of issues

$2.3

RBC Capital Markets

21

1.5

Scotiabank

13

1.5

BMO Capital Markets

26

1.5

CIBC World Markets

15

3

1

Goldman Sachs

top 5 law firms for M&A

Rank

Law firm

Value (USD billions)

No. of deals

$39.2

Torys

63

38.9

Stikeman Elliott

116

37.8

Blake Cassels & Graydon

101

37.4

McCarthy Tetrault

88

34

Skadden

17

HISTORICAL CANADIAN equity issuance

Value (billions)

$70

10-year

average:

$40.4

60

50

40

30

20

10

2012

2014

2016

2020

2022

2018

HISTORICAL CANADIAN M&A

Value (in billions of U.S. dollars)

$350

300

250

200

10-year

average:

$230.2

150

100

2022

2020

2018

2016

2014

2012

THE GLOBE AND MAIL, SOURCE: refinitiv

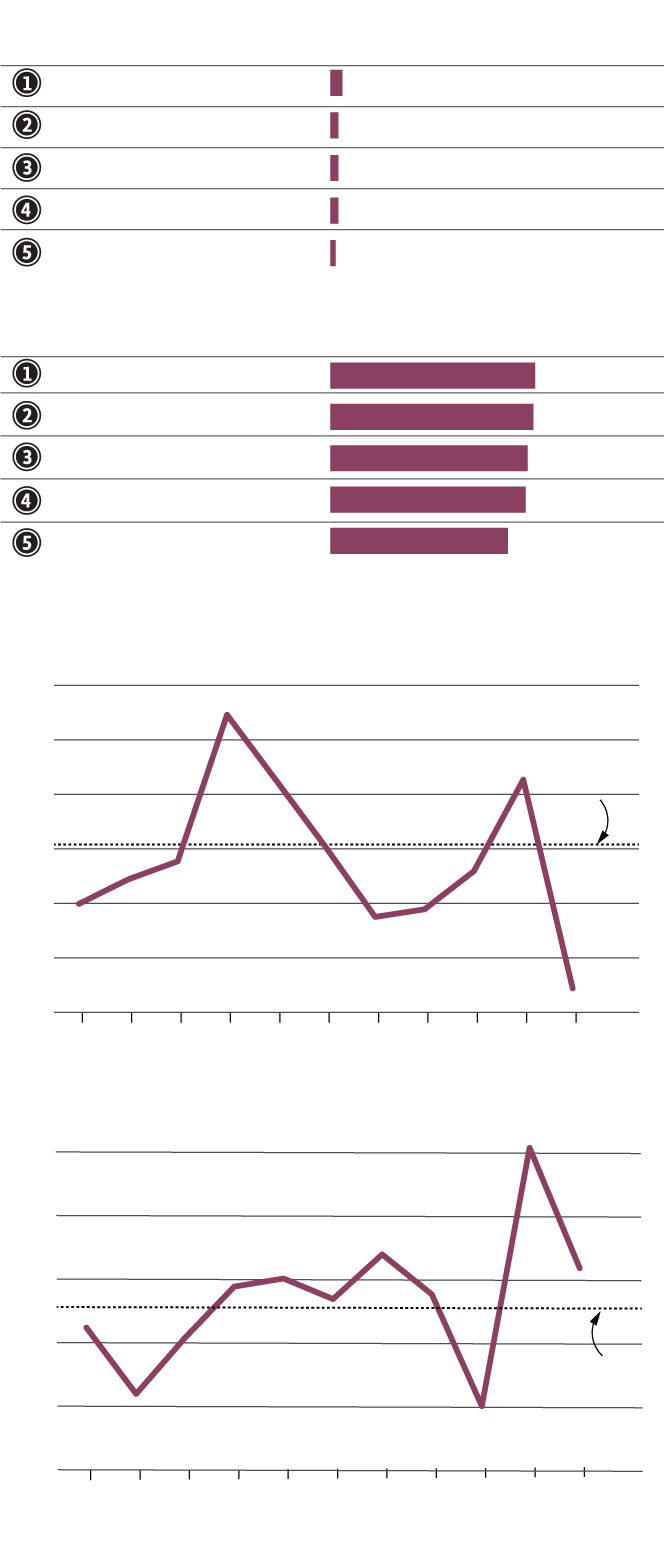

Top banks for equity underwriting

Rank

Banks

Value (billions)

No. of issues

$2.3

RBC Capital Markets

21

1.5

Scotiabank

13

1.5

BMO Capital Markets

26

1.5

CIBC World Markets

15

3

1

Goldman Sachs

top 5 law firms for M&A

Rank

Law firm

Value (USD billions)

No. of deals

$39.2

Torys

63

38.9

Stikeman Elliott

116

37.8

Blake Cassels & Graydon

101

37.4

McCarthy Tetrault

88

34

Skadden

17

HISTORICAL CANADIAN equity issuance

Value (billions)

$70

10-year

average:

$40.4

60

50

40

30

20

10

2012

2014

2016

2020

2022

2018

HISTORICAL CANADIAN M&A

Value (in billions of U.S. dollars)

$350

300

250

200

10-year

average:

$230.2

150

100

2022

2020

2018

2016

2014

2012

THE GLOBE AND MAIL, SOURCE: refinitiv

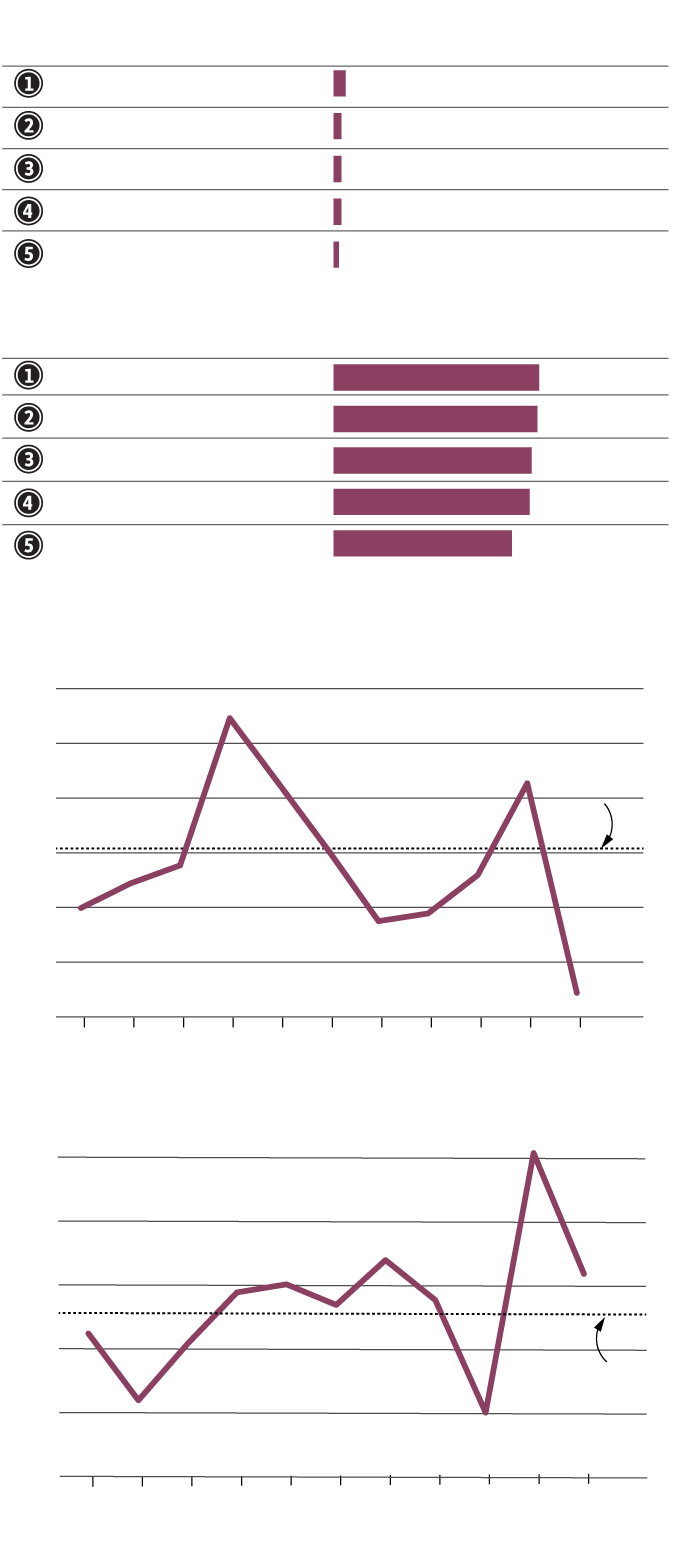

Top banks for equity underwriting

Rank

Banks

Value (billions)

No. of issues

$2.3

RBC Capital Markets

21

1.5

Scotiabank

13

1.5

BMO Capital Markets

26

1.5

CIBC World Markets

15

3

1

Goldman Sachs

top 5 law firms for M&A

Rank

Law firm

Value (USD billions)

No. of deals

$39.2

Torys

63

38.9

Stikeman Elliott

116

37.8

Blake Cassels & Graydon

101

37.4

McCarthy Tetrault

88

34

Skadden

17

HISTORICAL CANADIAN equity issuance

Value (billions)

$70

10-year

average:

$40.4

60

50

40

30

20

10

2012

2014

2016

2020

2022

2018

HISTORICAL CANADIAN M&A

Value (in billions of U.S. dollars)

$350

300

250

200

10-year

average:

$230.2

150

100

2022

2020

2018

2016

2014

2012

THE GLOBE AND MAIL, SOURCE: refinitiv

Interest rates rising with historic speed was part of the reason for the decline in sales of both stocks and bonds, though the rate-hike cycle itself was driven by stubbornly persistent inflation, which Mr. Babbar said was exacerbated by Russia’s invasion of Ukraine. The resulting market volatility that dominated much of 2022 meant there were fewer windows of relative tranquility where investors would willingly respond to a deal.

“As difficult a year as it seems to have been – and the headlines can be jaw-dropping – there really isn’t a market that you can’t do stuff in, not for long,” Mr. Babbar said. “As long as you have flexibility and patience and as long as you’re creative, you can get transactions to market.”

One such transaction came in mid-December, when Keyera Corp. tapped RBC for a bought deal offering of $230-million to help fund the acquisition of a Plains Midstream asset.

“We focused on how to get the transaction done amidst oil price volatility and we picked a day when the Fed came out and got to market,” Mr. Babbar said. “Things got volatile afterwards, but [the Keyera deal] got to market and it was priced right and investors supported it.”

Merger and acquisition activity, meanwhile, was actually a bright spot for Canadian capital markets last year. Although the total 2022 deal value fell 27 per cent to US$256-billion from 2021′s record-breaking US$350.9-billion, last year’s total was still more than 11 per cent above the historical average of US$230.2-billion for the 10-year period from 2012 through 2021, according to Refinitiv data.

“If you are comparing the level of [M&A] activity to the level we enjoyed in 2020 or 2021, then I think we’ll all feel discouraged in 2023,” said Jeffrey Singer, the chair of Stikeman Elliott LLP, which placed second to Torys LLP as the top law firm for M&A in Canada last year, having advised on 116 deals collectively worth US$38.9-billion. Torys advised on 63 deals worth a combined US$39.2-billion last year.

One of the trends that CIBC’s Mr. Swan is expecting to drive new stock sales in 2023 is companies raising equity in order to reduce the amount of debt on their balance sheets as debt servicing costs rise.

“For some companies, I think that will mean just raising some equity to deleverage,” he said. “For others it might mean raising equity to facilitate an acquisition, particularly if the current period of economic slowdown and volatility also creates opportunities that they haven’t seen to make acquisitions in recent years.”

Mr. Singer has a similar outlook. He said take-private transactions could be especially popular in the year ahead as the vast majority of companies that have gone public in recent years are currently trading well below their initial offering price. He also expects to see an uptick in distressed M&A as well as larger conglomerates selling off non-core assets in order to shore up their balance sheets.

“I continue to expect a more robust 2023 from historic standards,” he said, “but not by 2021 standards.”

What the market is going to focus on overall this year, according to Mr. Babbar, is inflation and consumer confidence.

“If we find ourselves in a world where inflation starts to roll over, not only in the data but in the lives we all live – where a head of broccoli is no longer 11 bucks – investors will start to feel like we’ve got this under control,” he said. “And the good news is that the market always leads the data, so we don’t necessarily need perfectly good data, we just need a trend that points to good data down the road.”