Glencore and Teck first talked marriage three years ago, Glencore CEO Gary Nagle said in a press conference on April 3, but could never reach agreement on terms.ARND WIEGMANN/Reuters

Glencore chief executive Gary Nagle is clearly a student of Canadian corporate history.

The Swiss CEO knows that in recent years, investors willingly sold the heart and soul of the domestic mining industry – global players Inco, Falconbridge and Alcan – for just a few dollars more than where their stocks were trading. In asset management, performance trumps nationalism every time.

After three years of unsuccessful merger talks with Teck Resources Ltd. TECK-N, Mr. Nagle is now bringing the same dynamic to bear to what’s become the country’s flagship base metal miner. With Vancouver-based Teck in the midst of a complex restructuring that’s received lukewarm reviews, Glencore GLNCY pitched a simpler transaction on Monday that has a greater short-term upside.

Teck’s future, supposedly assured because of family control of the company, is suddenly very much in doubt.

Teck is vulnerable because investors were underwhelmed by February’s announcement of plans to spin off the company’s British Columbia steelmaking coal mines into a new TSX-listed company, Elk Valley Resources Ltd. The complexity in the deal includes an agreement that sees Teck receive a minimum of $14-billion in cash from Elk Valley over up to 11 years, through royalty payments.

For investors who want nothing to do with coal of any flavour, over concerns with its carbon emissions, Teck’s proposed spin-out is a slow-motion divorce, where they want a quick, clean breakup.

Eric Reguly: Teck’s coal spinoff is greenwashing and a blow to the ESG movement

Teck has two classes of shares. On most issues, control rests with multiple-vote A shares owned by the founding Keevil family, along with Japan’s Sumitomo Metal Mining Corp. Ltd. and fund manager China Investment Corp. (CIC). There are also widely held single-vote B shares.

Later this month, all of Teck’s owners get a rare chance to flex their muscle. Teck needs two-thirds of both its A-class and B-class shareholders to separately approve the Elk Valley spin-out at a meeting scheduled for April 26.

The planned vote, later this month, created a vulnerability Glencore is exploiting.

On Monday, Mr. Nagle proposed a merger that would see all Teck shareholders swap their stock for Glencore shares at a 20-per-cent premium to where their stock traded prior to the announcement of the offer. The moment the deal is done, Glencore intends to spin out both companies’ massive coal businesses, and move forward as one of the world’s largest copper producers. There will be no ties between the two miners.

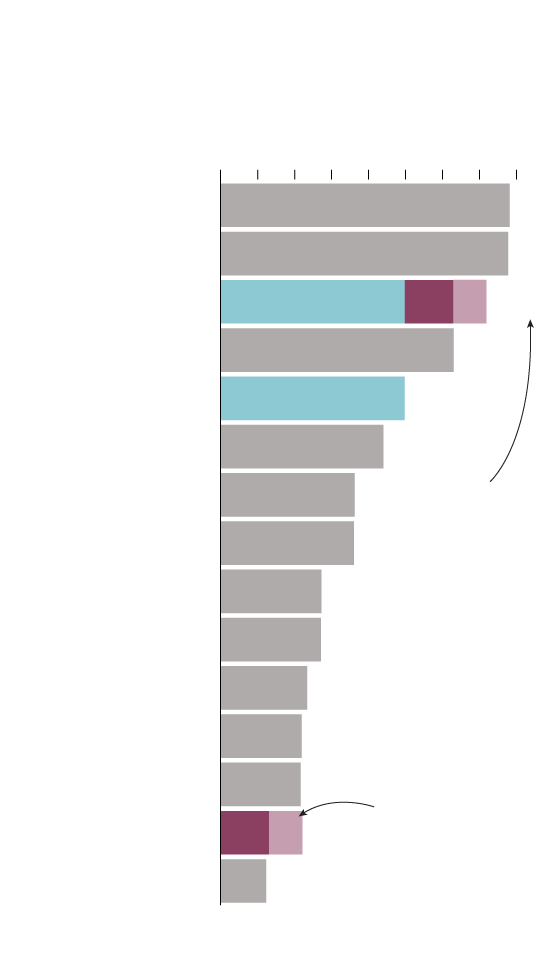

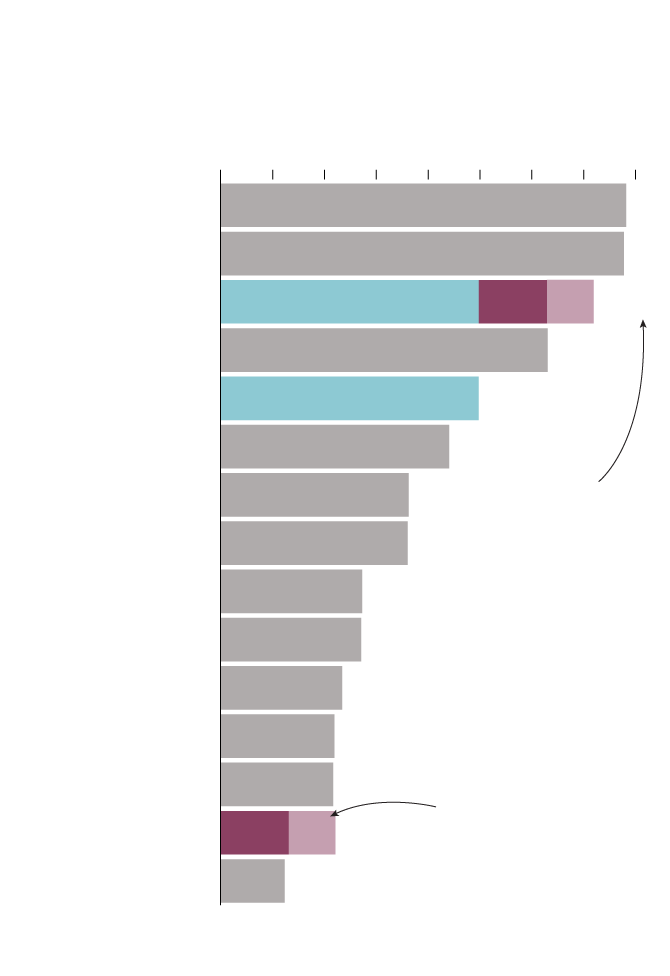

Largest copper-producing companies

in the world, 2022

Estimated production in kilotonnes

0

400

800

1,200

1,600

Freeport

Codelco

1,436

Glencore and Teck

BHP

Glencore

994

Grupo Mexico

First Quantum

A Glencore-Teck merger would make it the third-largest copper producer

Zijin

KGHM

Rio Tinto

Anglo American

Antofagasta

Nornickel

Quebrada Blanca Phase 2 mine ramped up

Teck

262

442

Vale

THE GLOBE AND MAIL, SOURCE: GLENCORE

Largest copper-producing companies

in the world, 2022

Estimated production in kilotonnes

0

400

800

1,200

1,600

Freeport

Codelco

1,436

Glencore and Teck

BHP

Glencore

994

Grupo Mexico

First Quantum

A Glencore-Teck merger would make it the third-largest copper producer

Zijin

KGHM

Rio Tinto

Anglo American

Antofagasta

Nornickel

Quebrada Blanca Phase 2 mine ramped up

Teck

262

442

Vale

THE GLOBE AND MAIL, SOURCE: GLENCORE

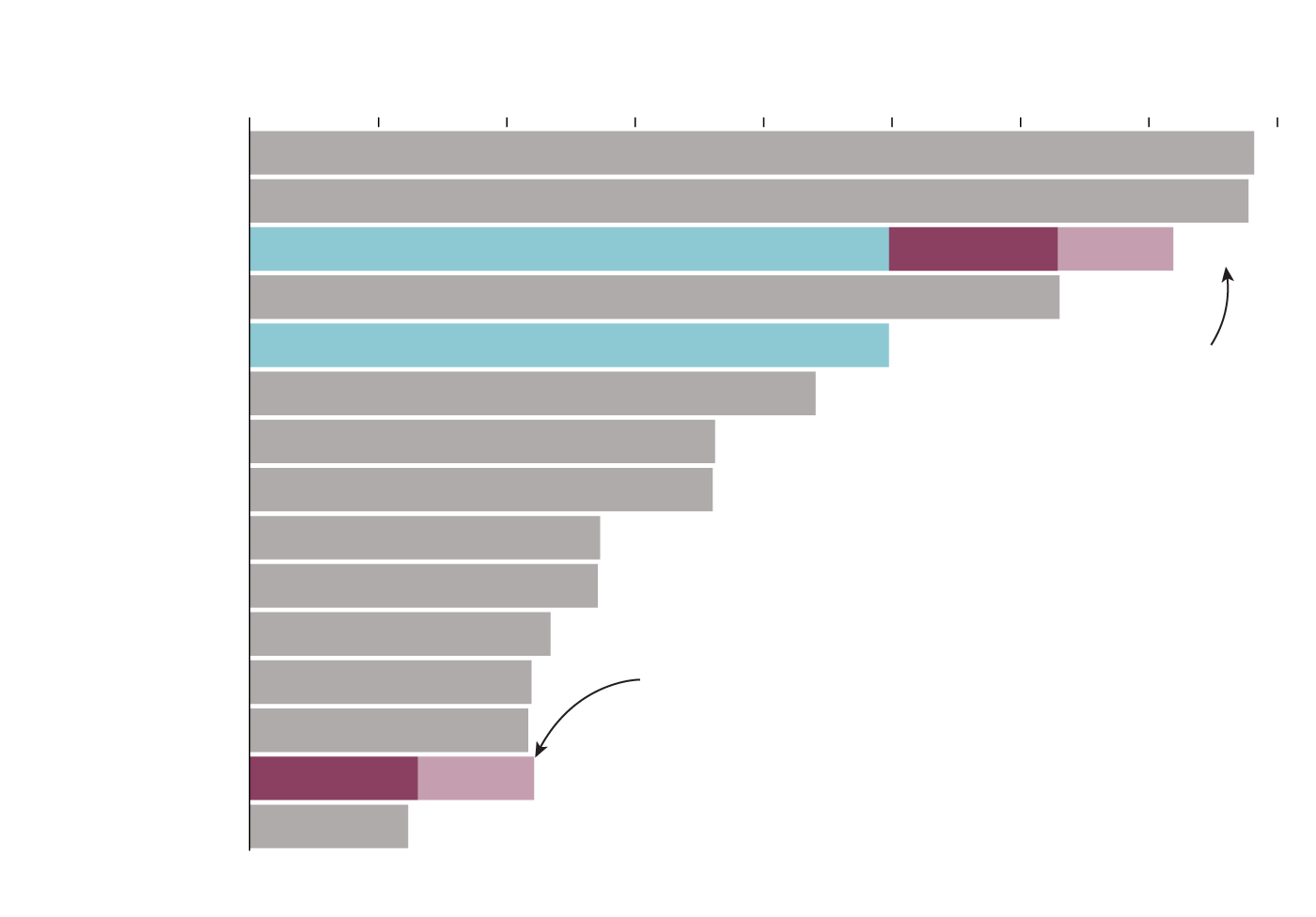

Largest copper-producing companies in the world, 2022

Estimated production in kilotonnes

0

400

800

1,200

1,600

Freeport

Codelco

1,436

Glencore and Teck

BHP

Glencore

994

A Glencore-Teck merger would make it the third-largest copper producer

Grupo Mexico

First Quantum

Zijin

KGHM

Rio Tinto

Anglo American

Quebrada Blanca Phase 2 mine ramped up

Antofagasta

Nornickel

Teck

262

442

Vale

THE GLOBE AND MAIL, SOURCE: GLENCORE

Glencore and Teck first talked marriage three years ago, Mr. Nagle said in a press conference on Monday, but could never reach agreement on terms. He said the latest bid is a “significant” improvement on past offers. Glencore also held out the possibility of further increasing the price if Teck’s board is willing to engage in talks.

With an eye to potentially gaining government approval, Glencore made a string of Canada-friendly promises, including a pledge to headquarter operations in either Vancouver or Toronto. Those details will matter in Ottawa. For the investors who will decide Teck’s future, Mr. Nagle won hearts simply by saying 20-per-cent premium.

Glencore is betting the prospect of a better offer will entice Teck class-B shareholders to vote against the planned Elk Valley spin-out. Glencore can also pressure Sumitomo and CIC to turn down the plan – Mr. Nagle said the Swiss company has strong relationships with both entities. (Pause for a moment to consider the prospect of state-backed CIC propping up flagship Canadian miners.)

Until Glencore went public on Monday, the vote on Teck’s restructuring seemed a foregone conclusion. Investors didn’t love the concept, but in the absence of an alternative, they would support splitting up the company, a prospect sweetened by the Keevil family’s pledge to get rid of Teck’s dual-class structure in six years, if the creation of Elk Valley is approved.

The landscape is now completely different. In Glencore, Teck shareholders have a potentially lucrative option to the spin-out. In an open letter in Monday, Teck chair Sheila Murray, a veteran corporate lawyer, listed a host of problems with Glencore’s plan and dismissed the proposal as “opportunistic.” She’s right. And Canadian mining history is filled with successful, opportunistic takeovers.