Now keenly aware of the threat of Britain exiting the European Union, investors this week will be fixated on the potential for Thursday’s referendum to wreak havoc on markets.

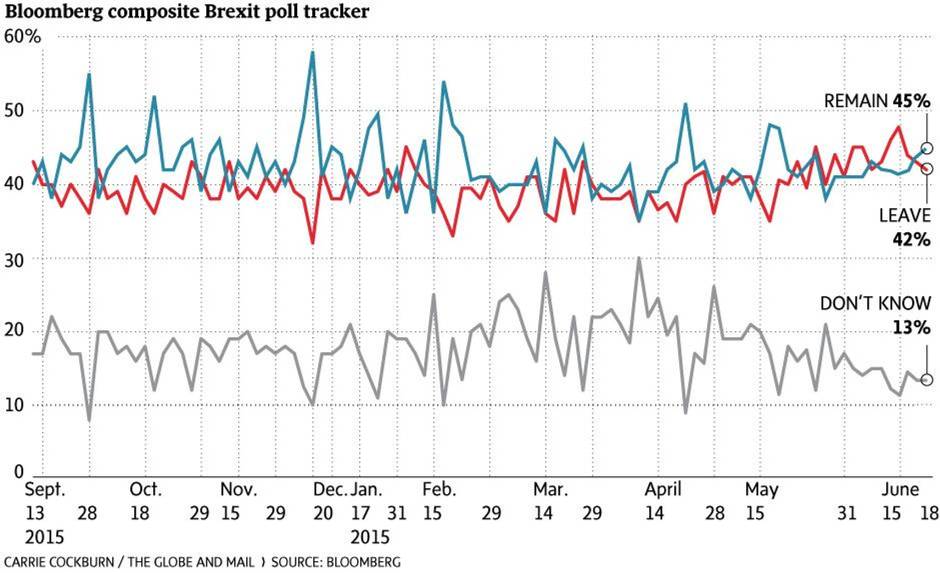

As the Brexit camp went from distant long shot to thin favourite in the polls last week – though the ‘Remain’ campaign pulled ahead by a few points over the weekend – the surge in global sentiment has shifted in favour of safety.

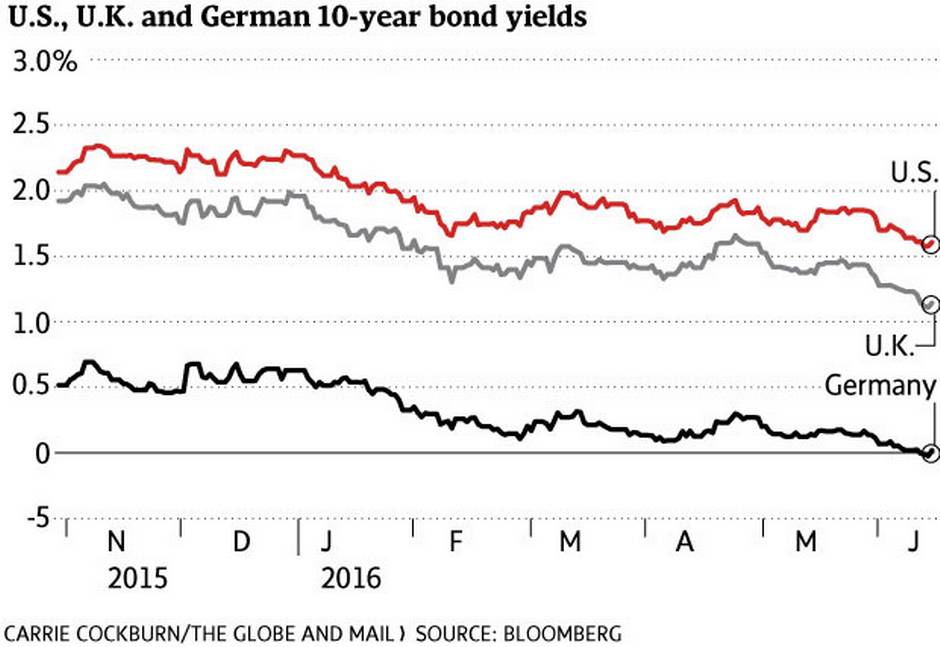

Markets last week bore the typical hallmarks of the risk-off trade: rising demand for government bonds and gold, and downward pressure on the prices of stocks, lower-quality bonds and oil.

This week likely holds more in the way of emotion-driven volatility until the result of the vote is known on Thursday night or Friday morning. And should the Leave campaign prevail, the immediate market reaction could be harsh.

“In certain respects, this ‘black swan’ effect is difficult to calculate since it is both unprecedented and almost impossible to assess the impact,” Tobias Levkovich, Citigroup Inc.’s chief U.S. equity strategist said in a report. “In our opinion, investor sentiment is the factor that could be most disrupted by a vote for Brexit.”

But that disruption could ultimately prove to be excessive, given the tendencies of investors once panic takes hold. Just as the consensus seems to be seeking shelter from a potential shock, opportunists are preparing to capitalize on an overreaction.

“Is it going to change the entire landscape of the global economy? If not, and the market is treating it as such, that’s when opportunities arise,” said Craig Fehr, an investment strategist at Edward Jones.

Growing support for leaving the EU has been met with portents of doom from European officialdom.

The British Treasury warned that a post-Brexit recession could last one year and cost half a million jobs. The International Monetary Fund forecasted a 5.5-per-cent reduction in national GDP, as its managing director Christine Lagarde pleaded for European unity. British Finance Minister George Osborne warned on Sunday the economic fallout “could be quite a lot worse than that.” And Bank of England Governor Mark Carney said the vote’s outcome represents the “largest immediate risk facing British financial markets, and possibly also global financial markets.”

Meanwhile, Mr. Carney’s U.S. counterpart, Janet Yellen, used uncertainty surrounding the referendum as one justification for refraining from raising U.S. policy rates.

Investors heeded the warnings. Global stocks, as measured by the MSCI All-Country World Index, sold off by week’s end by 4.4 per cent from an intraday peak on June 8, around the time the Leave vote began to claim a majority in polling. British equity funds saw their second-largest net weekly outflow in the past decade, Merrill Lynch said.

Gold prices rose to their highest in almost a year and a half in excess of $1,300 (U.S.).

And the risk aversion added momentum to the interminable decline of government bond yields. U.S. 10-year government bond yields fell to their lowest since February, British gilt yields to their lowest on record and German 10-year bonds went into negative territory for the first time ever. Friday saw a respite in the flight to safety, with those yields posting marginal gains.

Despite the sell-off of riskier assets, and despite the shift in the polls, two-thirds of fund managers polled by Merrill Lynch think a Brexit vote is unlikely. Odds makers are still pegging a Leave result as unlikely on the expectation that the status quo will rise in support once it comes time to cast votes.

That indicates that a Brexit is probably not yet priced into markets, leaving plenty of potential downside.

“European equity markets would be very likely to drop further and peripheral bond yields could rise further, raising the threat of a re-ignition of the [euro zone] debt crisis,” Jonathan Loynes, chief European economist at Capital Economics, said in a note.

But the medium-term costs, at least outside Britain, should be minimal, according to Benjamin Tal, CIBC World Markets’ deputy chief economist.

Britain accounts for less than 5 per cent of trade between both Canada and the United States, and represents a small share of earnings for Canadian and U.S. corporations, Mr. Tal said.

“A relief rally is guaranteed if a Remain vote prevails. But even in the case of a Leave victory, the initial sell-off should provide some interesting buying opportunities. Markets will realize that beyond the rhetoric, Brexit is nothing more than another Y2K.”