"To everything, there is a season." It's an important piece of wisdom for investors to keep in mind— a reminder that change is to be expected.

While we may all be enjoying the last weeks of summer, in the world of finance, it seems change is already upon us. Before the events of last week, it had been over four years since there had been a correction of 10 per cent or more in the US stock market; taken in that light, the current volatility was overdue.

Over the years I've worked with high-net-worth (HNW) individuals, I've noticed that they are particularly good at accepting how the "financial seasons" inevitably change. Most of them understand that preparing for a correction or downturn is an essential part of the investment process.

I've spoken before about how over the past several months, the HNW individuals I know have been shifting their focus from offence to defence. They had become increasingly cautious about most assets, closing out speculative positions and consolidating their portfolio around their strongest conviction ideas. They've been in the process of building up cash, hedging downside risk, and making capital preservation their top priority for some time. It's a move we've strongly endorsed and recommended to our clients.

Looking forward, the question becomes: will the markets bounce back strongly from the recent volatility? It's certainly possible. But even if we do see a short-term recovery, we will continue to think defensively. What specifically has us shifting into defensive mode right now?

Lack of market breadth in the U.S.

So far year to date, the S&P 500 stock market index is down about 7 per cent for the year. That's disappointing, but it's not a total disaster, particularly after several years of strong gains.

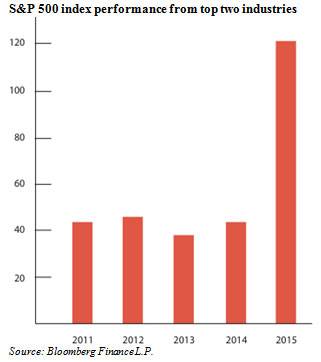

Dig a little deeper, however, and you realize that most of the performance had been driven by a very small group of companies. In fact, as of July 30, the top 20 companies (only 4 per cent of the total index) had been responsible for 56 per cent of the year-to-date returns.

You can see that clearly in the following chart, which tracks the contribution of the top two industries (this year, healthcare and retail) to total S&P 500 gains as of Aug. 4.

Historically, this lack of breadth has been a classic contrarian signal, and an indication that market performance isn't as rosy as it may seem. Until breadth returns to the market, we'll continue to remain cautious on U.S. stocks.

Increase in margin debt

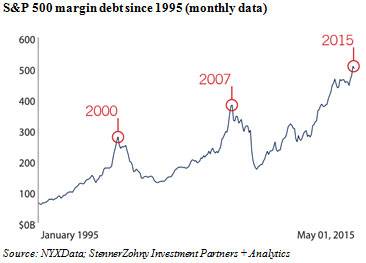

One of the data points I like to keep an eye on is the growth of margin debt (many investors have borrowed to invest). When margin grows, it can be a sign of stock market optimism and speculation.

The chart below makes it clear how margin has exploded over the past several years. As of May of 2015, there was $499-billion of margin debt in the U.S. financial system. Notice how this compares to two other times of extreme overconfidence.

This growth is fuelled both by low interest rates and a sense of exuberance. When speculation becomes the "new normal," its easy to understand the danger: if the market goes down, leveraged investors may be forced to sell to cover their loans, thereby making a downturn worse. We'll be watching this data point closely over the next several weeks, to see if leverage returns to a more moderate level—an indication that some of the emotion has been taken out of the market.

Cheap money has created a lot of market "noise"

Speaking of cheap money, ultra-low interest rates are fuelling a lot of things that don't have a lot to do with earnings: mergers and acquisitions, initial public offerings and also share buybacks.

These are often welcome events for shareholders, and, in many cases, they make good business sense. But they can create a lot of "noise" that can distract investors from the reality underpinning share prices. Until such activity decreases, we'll likely be wary of any market recovery.

Investors being forced into equities

The current ultra-low interest rate environment has been good for anyone with a mortgage. But it has presented a challenge for income investors. Should they sit in cash and earn nothing? Or lend it to the government for 10 years and earn 1.5 per cent (that's before taxes and inflation)?

Neither option is attractive. And that's caused many investors who would normally put their money in bonds to seek yield in other places, including dividend paying stocks. The result is a natural risk premium that has caused equities to be expensive by nearly every historic measure.

This is a mixed blessing. On one hand, anyone who owns big name blue-chip dividend paying stocks has enjoyed strong performance over the past several years. On the other hand, it has created an additional layer of market risk. What happens when investors who aren't used to seeing their positions drop by, say, 10-15 per cent (normal in a downturn) or potentially, 30 per cent (or more), as we saw back in 2008? We'd like to know the answer before we return to the stock market in force.

We're living in "interesting times"

Finally, I remember the famous "Chinese curse"—may you live in interesting times. I'm not a political scientist, but there seems to be a lot of international goings-on that could qualify as "interesting times," and many of them have a distinct economic slant. The ongoing crisis in Greece and the economic turmoil in China are at the top of the list. Iran's nuclear deal and its implications on the price of oil is also worth keeping an eye on, particularly because of the "ripple effect" that cheap oil may have on the Canadian oil patch. Russia's increasing belligerence toward the west is also something to think about, because of the profound and long-lasting implications on European business prospects.

None of these issues have really been resolved—they've just been kicked down the road, making it possible that any or all of them could end up being the "trigger" for a systemic economic event. We'd like to see more guidance on at least some of these issues (Greece and China particularly) before we give the "all clear" for stock market investors.

Some may look at this list and declare I'm simply gazing into a crystal ball, trying to predict the future. I understand that argument, and if I were talking about any one signal in isolation, I might agree.

But it's not one danger signal—it's many, flashing all at once. Taken together, these signals offer a very strong argument for caution being the prudent course right now.

Yes, there are still pockets of opportunity — and these may well increase, if volatility increases in the weeks to come. But they require deep digging, and some serious due diligence. Currently, HNW individuals are more interested in specialized, deep value opportunities than in the broader market. Following their lead seems the wise thing to do.

Thane Stenner is founder of StennerZohny Investment Partners+ within Richardson GMP Ltd., as well as Director, Wealth Management. Thane is also Chairman Emeritus for TIGER 21 Canada. He is the bestselling author of ´True Wealth: an expert guide for high-net-worth individuals (and their advisors)'. (www.stennerzohny.com) (Thane.Stenner@RichardsonGMP.com The opinions expressed in this article are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Ltd. or its affiliates.