Merrill Lynch quantitative strategist Savita Subramanian calls U.S. equity purchases a “no brainer” relative to bonds. But are equities the clear choice over fixed income in Canada?

Ms. Subramanian’s conclusions are based on the relative yields of the S&P 500 and the 10-year U.S. Treasury bond. The yield on the U.S. equity benchmark climbed above the 10-year bond yield in August, and has stayed there since. Historically, 94 per cent of the instances in which this happened in the past saw stocks outperform bonds over the next 12 months – and by a significant 23.1 percentage points on average, she said in a report this week.

Using data from 1993 (Merrill Lynch has access to a longer series), I was able to confirm that there were 37 monthly instances when the S&P 500 trailing 12-month yield was higher than the 10-year bond for the period. The average simple return for the equity benchmark in the following 12 months was 20 per cent.

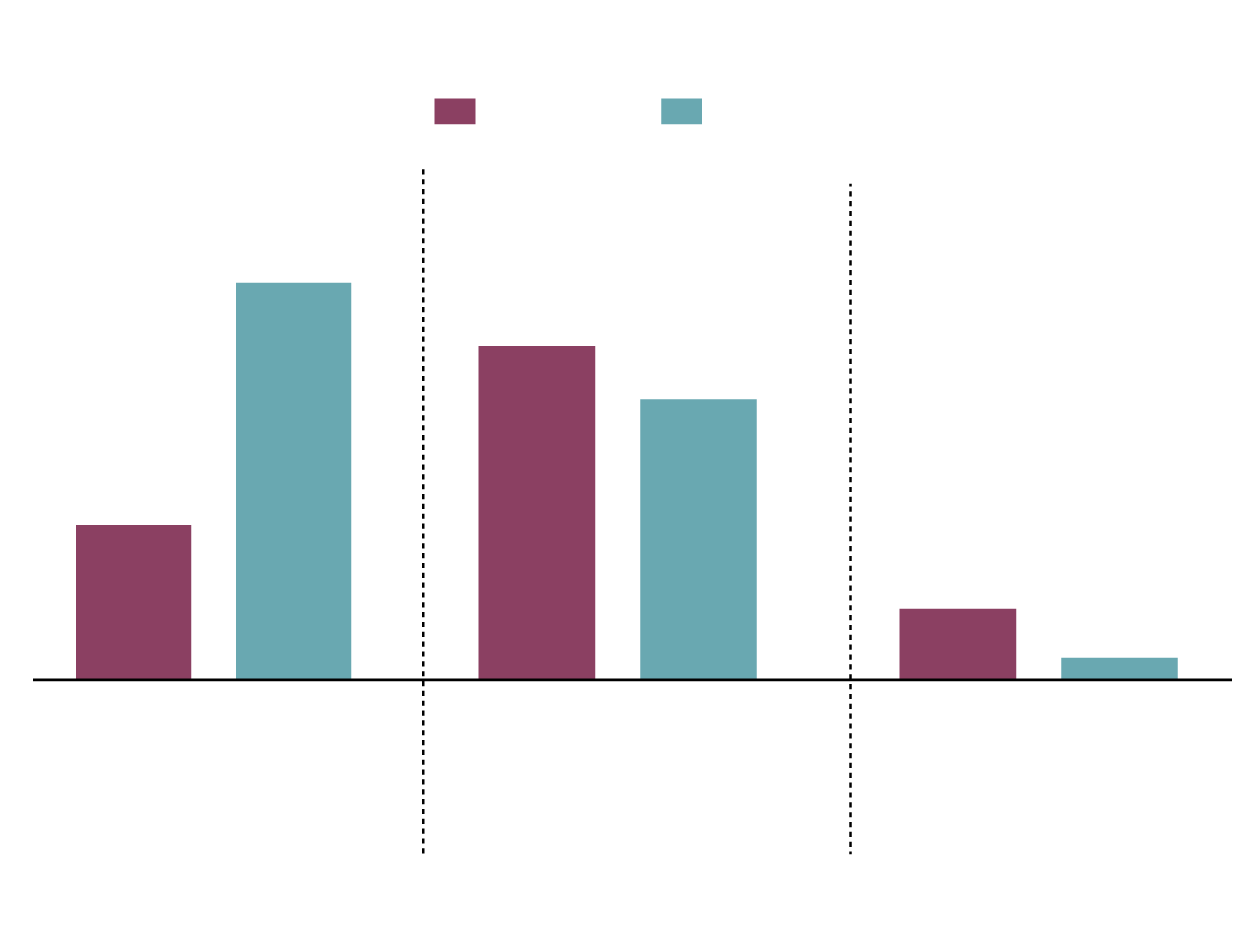

Equity yields vs. bond yields

1993 to present

S&P 500

S&P/TSX Composite Index

95

94%

78%

37

20%

6.2%

Months when

equity yield >

10Y gov’t

bond yield

Success rate:

Positive Fwd

12M equity return

Average equity

index return

JOHN SOPINSKI/THE GLOBE AND MAIL

SOURCE: scott barlow; bloomberg

Equity yields vs. bond yields

1993 to present

S&P 500

S&P/TSX Composite Index

95

94%

78%

37

20%

6.2%

Months when

equity yield >

10Y gov’t

bond yield

Success rate:

Positive Fwd

12M equity return

Average equity

index return

JOHN SOPINSKI/THE GLOBE AND MAIL

SOURCE: scott barlow; bloomberg

Equity yields vs. bond yields

1993 to present

S&P 500

S&P/TSX Composite Index

95

94%

78%

37

20%

6.2%

Months when equity

yield >10Y gov’t

bond yield

Success rate: Positive

Fwd 12M equity return

Average equity

index return

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: scott barlow; bloomberg

There were only two cases where the U.S. equity benchmark declined in the 12 months after the equity yield was above the bond yield (using monthly data).

The same analysis applied to the S&P/TSX Composite Index provided promising, but less clear-cut advice for domestic investors.

The 1993-present period provided a lot more instances – 95 – when the TSX yield was above the 10-year government of Canada bond yield. But the success rate was lower, at 78 per cent. Put another way, there were 21 occasions (out of 95) when the TSX yield was above the bond yield – and the equity market declined in the following 12 months.

The average 12-month simple return for the Canadian equity benchmark following months when the equity yield was higher than the bond yield was 6.2 per cent. This is an okay return, but significantly lower than the 20 per cent average gain in the S&P 500.

The collapse in oil prices in 2014 played an important role in making Canada’s trend different than the United States. From June, 2014, to June, 2015, the dividend yield on the S&P/TSX Composite was higher than the 10-year bond yield, but stock-market returns were negative for the next 12 months in each case because of the continued weakness in the oil sector.

The ability of the oil sector to neuter the success of this investing strategy (“buy equities when the benchmark yield is higher than the bond yield”), which has worked so well in the United States market, highlights the lack of diversification in the domestic benchmark. If metals, oil or bank stocks experience extreme volatility, all bets are off in terms of previous performance patterns.

On balance, however, Ms. Subramanian’s “no brainer” description does seem justified south of the border. The 94-per-cent success rate for positive equity returns when the S&P 500 dividend yield is higher than the 10-year Treasury yield is compelling. The case for Canadian equities is weaker based on market history, but the odds are still in favour of stocks over bonds for the next 12 months.