If you’re an investor looking for clues about which way the economy will swerve in the months ahead, let me suggest keeping tabs on an often overlooked number – how many people the U.S. construction sector is employing.

This may seem an odd statistic to obsess over, but bear with me.

My reasoning begins with the overwhelming importance of the U.S. economy. While Canada has some power to chart its own course, a downturn (or a boom) in the United States inevitably ripples across the border, with major impact here.

So what determines the health of the giant U.S. economy? Most of the time, it’s housing, according to Edward Leamer, an economist at UCLA. In 2007, he wrote an influential research paper with an admirably succinct title: Housing IS the Business Cycle.

As the title suggests, Prof. Leamer showed that most U.S. recessions are preceded by problems in the housing market.

There have been exceptions to this rule – the dotcom recession of 2001 or the pandemic downturn of 2020, for instance – when the economy was sideswiped by out-of-the-blue factors that had nothing to do with housing. But most of the time, recessions proceed in a more predictable fashion. A slowdown in housing starts provides early warning of a broader recession ahead.

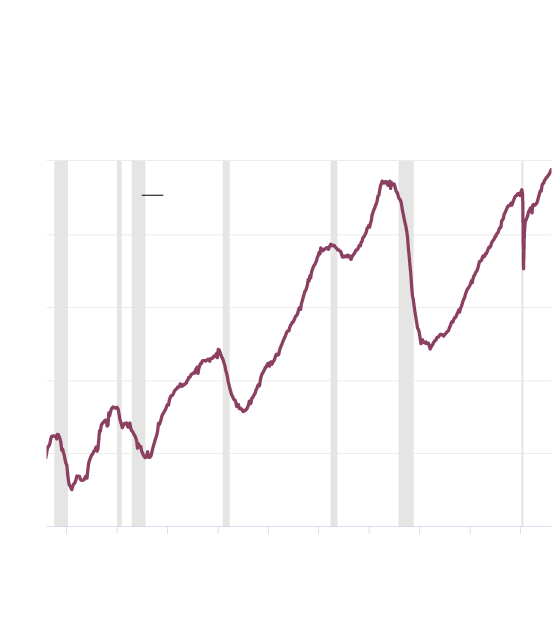

No slowdown here

Falling numbers of construction workers often provide an early

warning of a broader U.S. recession ahead. So far, though, employ-

ment in the sector is proving remarkably robust.

(All construction employees, in millions)

8

U.S.

recessions

7

6

5

4

3

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

the globe and mail, Source: u.s .federal reserve bank of st. louis

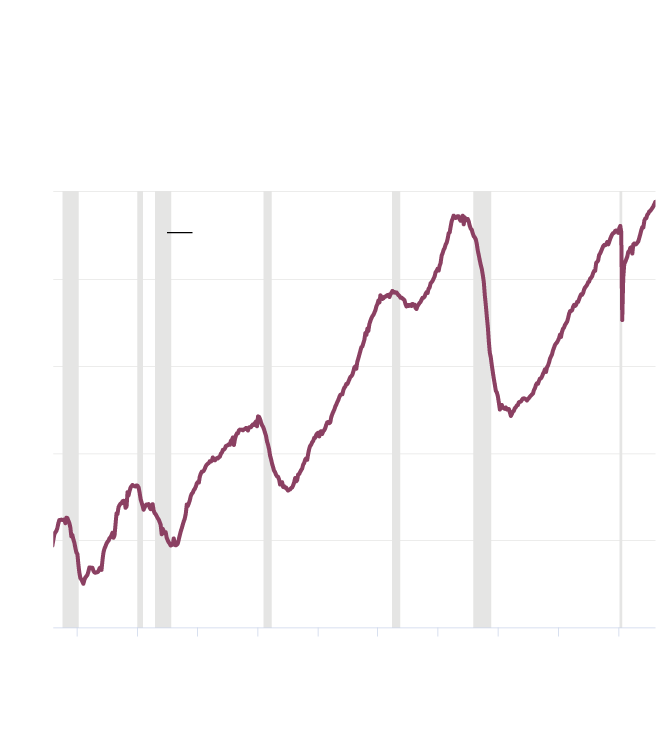

No slowdown here

Falling numbers of construction workers often provide an early

warning of a broader U.S. recession ahead. So far, though, employ-

ment in the sector is proving remarkably robust.

(All construction employees, in millions)

8

U.S.

recessions

7

6

5

4

3

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

the globe and mail, Source: u.s .federal reserve bank of st. louis

No slowdown here

Falling numbers of construction workers often provide an early warning of a broader U.S. recession

ahead. So far, though, employment in the sector is proving remarkably robust.

(All construction employees, in millions)

8

U.S.

recessions

7

6

5

4

3

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

the globe and mail, Source: u.s .federal reserve bank of st. louis

This makes sense given the powerful knock-on effects that housing exerts across the economy. Any tremour in housing starts and home prices is felt in areas ranging from appliance sales and renovation spending to home-equity loans and lumber prices. In the words of David Rosenberg of Rosenberg Research, housing is “the quintessential leading indicator” for the broad economy.

Right now, the housing indicator is flashing red. Single-family housing starts in the U.S. have dropped sharply in four of the past five months, Mr. Rosenberg wrote in a note Friday. Single-family housing permits – which lead housing starts – have slid 11 months in a row. All of this would be in keeping with a recession beginning in the second quarter of this year, he said.

But here is where the picture gets murky, at least to my eye. If the housing market were teetering on the verge of a major slowdown, you would expect to see the stock prices of major U.S. homebuilders such as D.R. Horton Inc., Lennar Corp. and PulteGroup Inc. taking it on the chin.

That isn’t happening. Instead, rather remarkably, each of these homebuilder stocks has gained over the past year, at the same time as the Federal Reserve has been aggressively hiking interest rates to slow down homebuilding and the broader economy.

Just as odd is the construction sector’s continuing pattern of hiring. Ordinarily, employment in the building trades flattens or falls before a recession – just what you would expect to see if developers and contractors were growing cautious about what is to come and wanted to trim payrolls to stay ahead of a slowing economy.

There is no evidence of such payroll trimming in the current numbers. In fact, employment in the sector rose by about 300,000 people over the year to the end of January, 2023, according to the Bureau of Labor Statistics.

How can construction employment and homebuilder stocks be rising at the same time as housing permits and housing starts are falling? The conflicting signals are a puzzle.

Maybe we’re at a Wile E. Coyote moment, when the housing sector has run off the cliff and is continuing to churn frantically without realizing that there is nothing but air beneath it.

That false confidence would be in keeping with recent work from Jim Reid, a research strategist at Deutsche Bank. He acknowledges that economic data have been improving around the globe, but disagrees with the growing number of people hoping for painless resolution to the inflationary spike.

He argues that the current euphoria is typical of what has happened historically when central banks have started to raise interest rates to tamp down inflation. Nothing much happens in the first year after the hikes begin. People start to believe that the economy is on target for a soft landing. However, problems commence in the second year – just about exactly where we are now.

“We’ve always thought that the second half of this year will be where the lag kicks in and U.S. recession risks skyrocket,” Mr. Reid wrote in a note this week.

On the other hand, homebuilders are perfectly capable of reading the economic tea leaves along with everyone else. Perhaps their confidence in hiring will prove to be justified. If so, and the housing market remains relatively strong, the U.S. may actually achieve a soft landing. That would be good news not just for the U.S. but for Canada as well.

I don’t pretend to know which it will be. But I do intend to keep close tabs on U.S. construction employment. (You can too: Just search for “all employees, construction” at fred.stlouisfed.org) If housing determines the broader economy, any signs that the sector is reducing its headcount would constitute a powerful signal for investors to get cautious fast.