Signs of trouble are emerging in the Canadian bond market, with foreign investors divesting nearly $10-billion worth of government debt in the first three months of 2025.Nathan Denette/The Canadian Press

Non-Canadians have sopped up vast quantities of government-issued bonds in recent years, making them enthusiastic creditors of the federal government.

Under normal circumstances, their participation is considered nothing more than an infusion of funds to finance federal spending and fill budget deficits.

But these are not normal circumstances.

A four-year economic winter has descended at the hands of a hostile American administration, and it suddenly matters how much of Canada’s debt is held outside the country.

With the federal deficit set to rise and a recession possibly already upon us, the country cannot afford for its debt-holders to get spooked. Signs of trouble are already emerging.

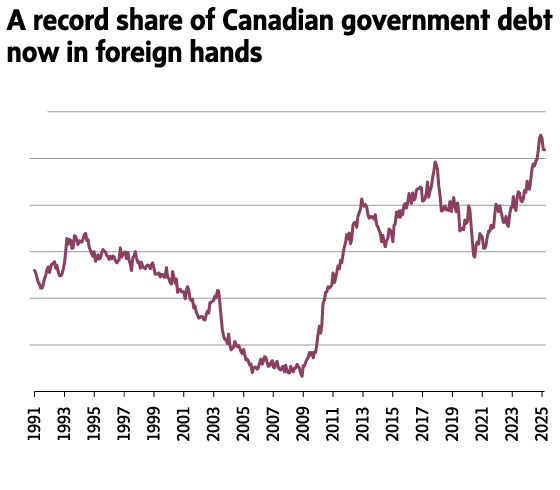

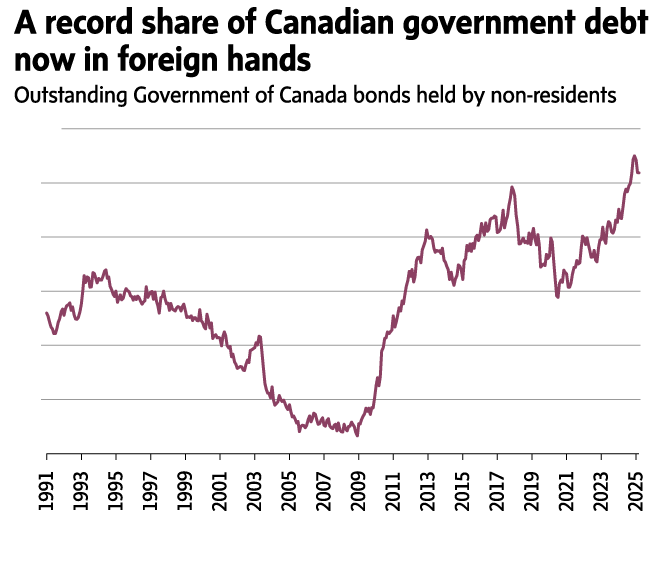

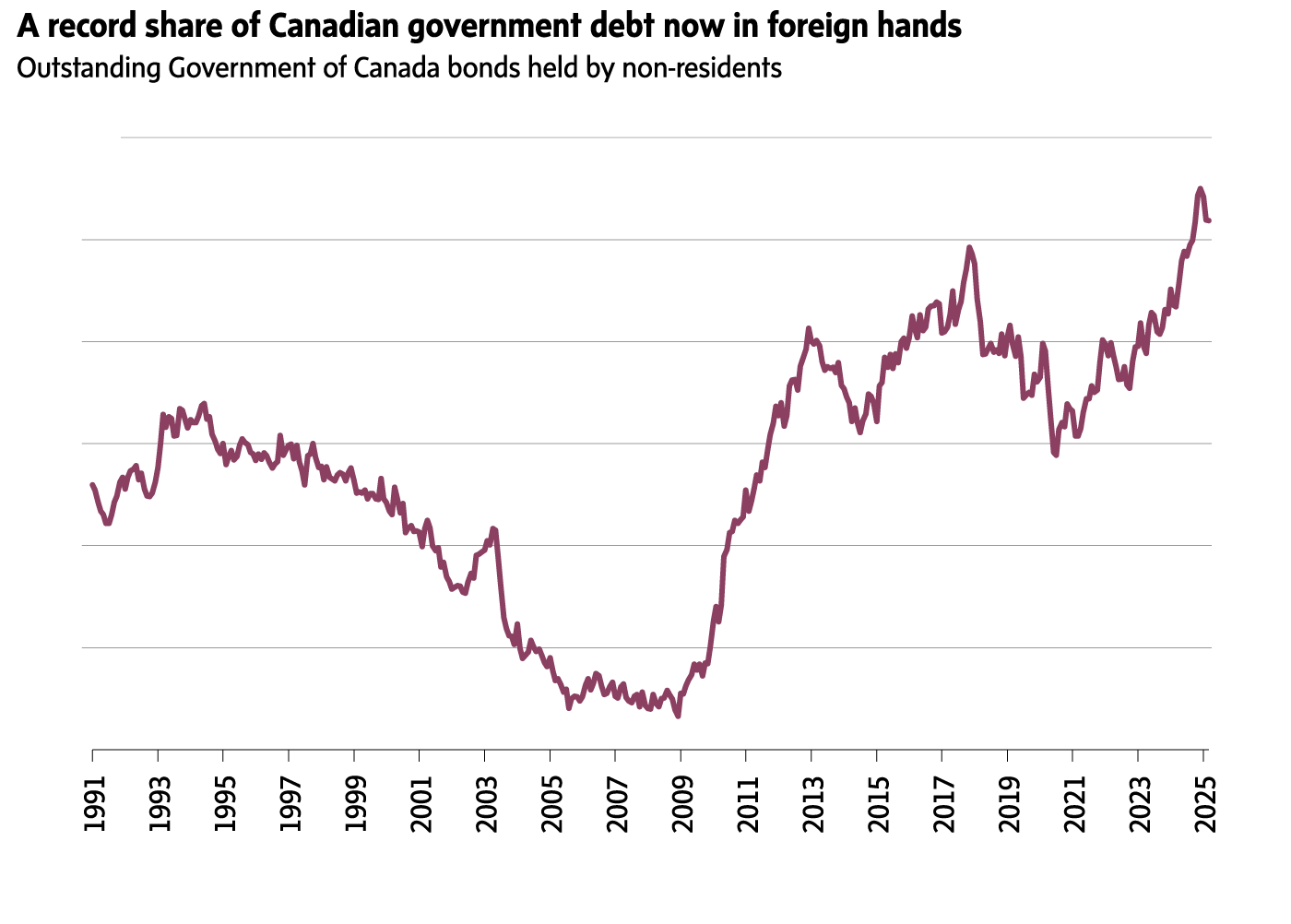

In the first three months of 2025, foreign appetite for Canadian government bonds vanished, as non-residents divested nearly $10-billion worth.

That’s not a huge number, but it is a big change in trend. International investors up to that point were ravenous for Government of Canada debt, absorbing 60 per cent of net new supply for a record $91-billion in fiscal 2024-25.

The ownership share held outside Canada’s borders now sits at 36 per cent, down slightly from the record set in December.

Outstanding Government of Canada bonds held by non-residents

40%

35

30

25

20

15

10

the globe and mail, Source: National Bank of Canada

40%

35

30

25

20

15

10

the globe and mail, Source: National Bank of Canada

40%

35

30

25

20

15

10

the globe and mail, Source: National Bank of Canada

If international creditors sour on Canada’s economy and its federal finances, they could simply stop buying its bonds or demand higher yields to get involved, wrote Warren Lovely, chief rates and public-sector strategist with National Bank of Canada, in a note to clients.

“In a sense then, non-resident investors may just hold the balance of power here,” Mr. Lovely said. “These investors should not be taken for granted as the Prime Minister sets off on an ambitious legislative agenda.”

Prime Minister Mark Carney has taken office in nation-building mode during what he recently called “the worst crisis of our lifetimes.” His agenda includes fast-tracking major infrastructure projects such as ports, mines and pipelines. Big fiscal promises include an income-tax cut for the middle class.

Big plans mean growing deficits and more bond auctions to pay for it all. Effective federal issuance could near a record of $200-billion in the fiscal year that got started in April, Mr. Lovely said.

Analysis: Here’s what really is going on in the bond market – and why I’m still very bullish

The country is relying on the favour of foreign investors now more than ever.

“The ultimate risk is if demand really does drop off substantially,” said Jeremy Kronick, vice-president of economic analysis and strategy at the C.D. Howe Institute.

Rising yields on Canadian government bonds would translate to higher costs throughout the domestic economy.

“That would make everything more expensive for households and businesses, and we’re a pretty highly leveraged economy as it is,” Mr. Kronick said.

And yet, Canada’s federal finances match up favourably to other developed countries, especially the United States, whose gigantic deficits earned it a credit rating downgrade from Moody’s two weeks ago.

To illustrate the gap between the two countries, 30-year benchmark yields in Canada are running about 140 basis points lower than comparable U.S. bonds. That’s the biggest differential since at least the 1970s, said Doug Porter, chief economist at Bank of Montreal, in a note.

“Canada, unlike its U.S. counterpart, is still in a good position to push out pro-growth tax cuts and infrastructure spending,” he said.

Maybe the first quarter was just a blip. It was, after all, a wild stretch during which U.S. President Donald Trump threatened Canada with economic obliteration and annexation. Not hard to imagine foreign investors taking a pause to see how it all shook out.

Alternative data sources on bond volumes suggest non-residents resumed buying Government of Canada debt in April, albeit at about half the pace of the previous year, Mr. Lovely said.

“It could be that the foreign divestment registered last quarter will prove fleeting.”

It had better be.