The world’s stupidest trade war shows no signs of letting up. Even if Donald Trump further postpones some or all of his tariffs on Canadian and Mexican goods in the weeks ahead, the possibility of more sudden, unpredictable bursts of U.S. hostility is going to continue to undermine the North American economy.

Just as damaging is Mr. Trump’s willingness to torch the pillars of global stability. By throwing Ukraine to the Russian wolf, walking away from European allies and cozying up to Vladimir Putin, he is incinerating the trust that Washington has built up over generations. He is demonstrating that no country can count on the United States to be a reliable friend.

Investors should think through the implications. Many of our bedrock notions about finance are beginning to shake and groan.

Start with the notion that the U.S. is a safe place for investors. That was once obviously true: Critics might deplore the country’s social failings, but for an investor the U.S. was near paradise – a stable, open economy with reasonable, fair government policies.

Not anymore. Mr. Trump’s crackpot economic beliefs have left respectable economists gaping. They keep trying to correct his falsehoods.

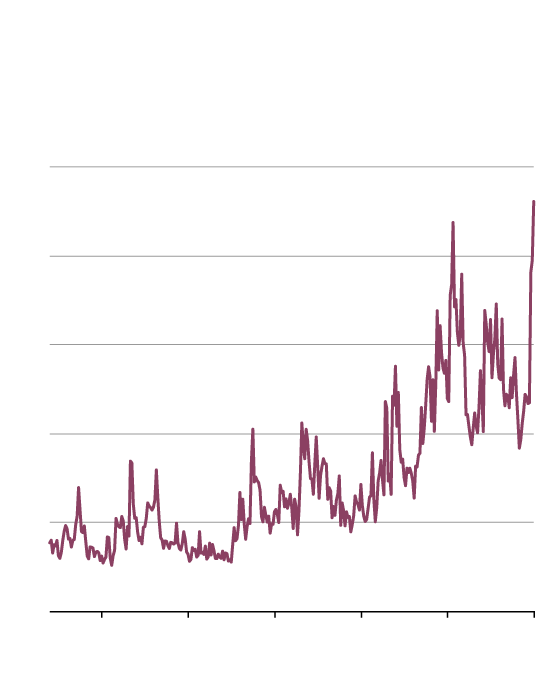

The war of fog

Donald Trump’s on-again, off-again tariffs and shambolic

policy-making has helped drive global economic policy

uncertainty to record highs, according to one gauge.

(Monthly Global Economic Policy Uncertainty Index)

500

400

300

200

100

0

2005

2010

2015

2020

2025

2000

the globe and mail, Source: Economic Policy Uncertainty

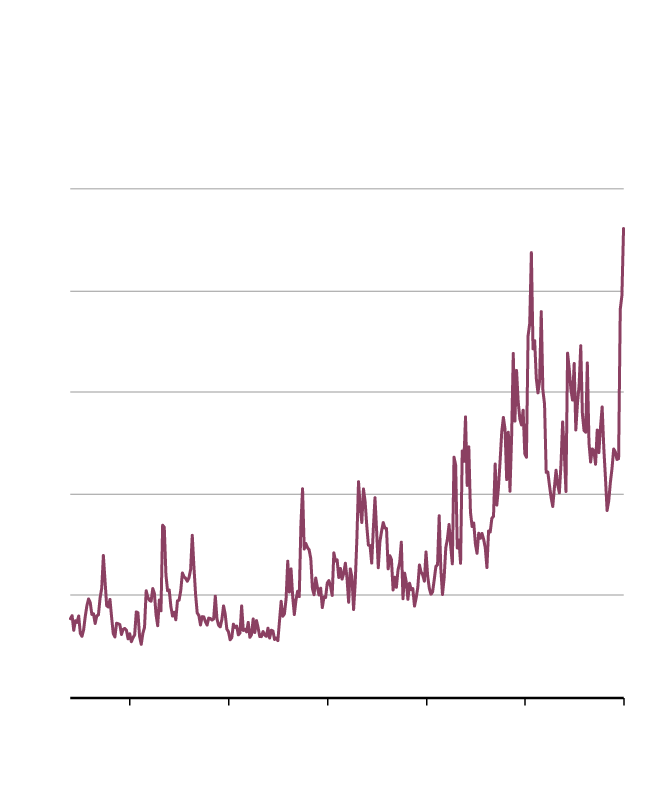

The war of fog

Donald Trump’s on-again, off-again tariffs and shambolic

policy-making has helped drive global economic policy

uncertainty to record highs, according to one gauge.

(Monthly Global Economic Policy Uncertainty Index)

500

400

300

200

100

0

2005

2010

Where to start? No, despite what the President insists, a trade deficit is not a “subsidy.” (Unless you believe that you’re somehow subsidizing your supermarket or your dentist by spending money on the things they provide.) No, despite his claims, you don’t make a nation richer by erecting comprehensive trade barriers. (If that worked, North Korea would be an economic dynamo.) And, no, despite his pronouncements, the U.S. does not need a strategic cryptocurrency reserve. (Because crypto has yet to find any useful purpose other than facilitating criminal transactions.)

It gets even worse. Mr. Trump’s policies are not only brainless, they are unpredictably brainless. Companies can adjust in time to bad policy; they can’t adjust at all if the bad policies are constantly shifting. Mr. Trump may think his frequent feints and delays on tariffs are somehow clever. In fact, the radical uncertainty he’s generating is deeply destabilizing to his own economy.

The self-harm that Mr. Trump is inflicting on the U.S. economy has led many people to speculate on his motives. One intriguing theory holds that he’s modelling himself on people such as Russia’s Mr. Putin, Hungary’s Viktor Orban and India’s Narendra Modi.

These leaders all practice “patrimonial” government. “They present themselves as powerful father figures who run the state itself as a family business, doling out its assets to cronies and sycophants in return for unquestioned personal loyalty,” write U.S. political scientists Stephen Hanson and Jeffrey Kopstein.

If Mr. Trump is aiming to become a patrimonial leader, the implications for the rule of law are ominous. Patrimonial governments tend to redefine what is legal as being what is acceptable to the boss.

“The letter of the law matters only for those lacking connections to the ruling household,” Prof. Hanson and Prof. Kopstein say. “Indeed, violations of even seemingly minor statutes and regulations can be used to launch lawsuits and criminal cases designed to punish enemies of the regime.”

Their observations should give investors pause. Mr. Trump and his minions are already running roughshod over legalities on matters such as firing public-sector workers. Will they be any more respectful of the law when it comes to property rights? Maybe not.

And then there is the related matter of taxation. If Mr. Trump is intent on punishing foreigners, imposing a hefty tax on non-U.S. holders of U.S. stocks and bonds would seem to be a natural policy move.

Foreign investors appear to have growing doubts about whether their money is now as safe in the U.S. as they once thought it was. Since Mr. Trump was elected, U.S. stocks have lagged behind both European and Chinese stocks – a striking reversal of the past few years.

Even more unusually, the U.S. dollar has been sliding in recent days against a basket of other currencies. This runs counter to the typical pattern in which investors run to embrace the greenback during times of stress. The slump in the U.S. dollar may speak to growing worries about U.S. economic growth and perhaps about the U.S. system in general.

So should investors simply exit the U.S.? It’s tempting to do so, but basing your stock picks on your political convictions is not usually something that works out well.

A more reasonable approach is to keep a toehold in U.S. stocks, but tilt your portfolio in other directions. Canadian dividend stocks have growing appeal. So do Canadian government bonds, guaranteed investment certificates and gold.

Investors should also consider the case for more radical diversification. European stocks have been surging and there is a strong case that they have more room to run after the German government signalled it will ease up on its notorious debt brake and spend more freely on defence and infrastructure.

Asian markets have their attractions, too. Both Chinese and Japanese stocks look cheap on many valuation measures. Yes, they carry political risks, but in Mr. Trump’s world, so does the U.S.