Buy low, sell high. That’s what they tell you when you are starting out as a wet-behind-the-ears investor, and it has been sound advice over the very long haul.

But over the past couple of decades? Not so much. For much of that period, the people who did best were those who insisted on buying high.

The biggest beneficiary of this love affair with pricey investments has been U.S. stocks. They have been strikingly more expensive than their international counterparts for more than a decade. Yet rather than losing ground to their cheaper rivals, they have clambered higher and higher, becoming more highly valued against underlying earnings with the passing years.

The performance gap between U.S. stocks and non-U.S. stocks has now reached staggering proportions. Over the past 15 years, Wall Street has generated average returns of 9.9 per cent a year. Stocks in the rest of the world have churned out barely half that – 5.4 per cent.

For investors, this sets up a difficult decision. Should they stick with the hot hand and tilt heavily toward U.S. stocks? Or should they take all those long-ago lessons about buying low to heart and run in the other direction, toward bargain-priced non-U.S. stocks?

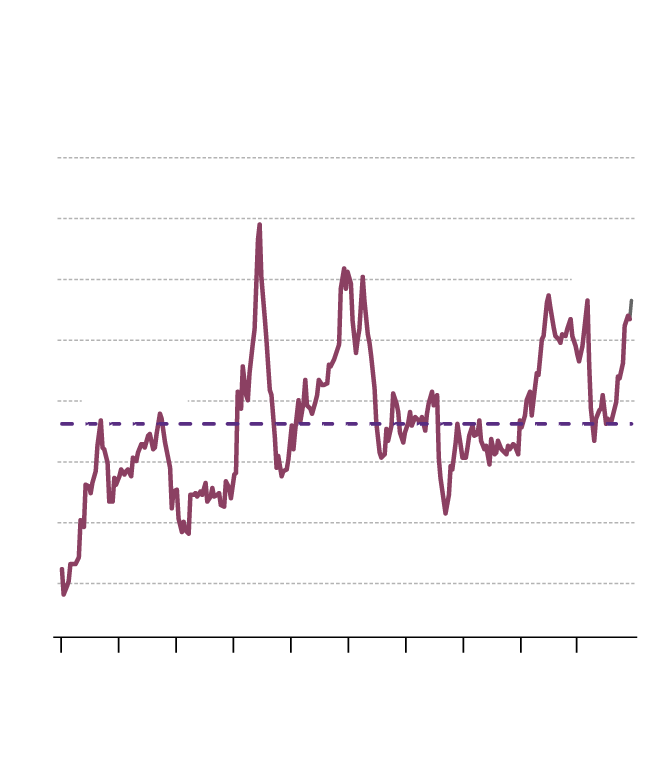

International stocks pay more in dividends

than U.S. stocks

Dividend yields on stocks outside the U.S. minus

the dividend yield on S&P 500

2.0%

1.8

Nov. 16, 2021:

1.5%

1.6

1.4

Avg. 1.1%

1.2

1.0

0.8

0.6

0.4

'01

'03

'05

'07

'09

'11

'13

'15

'17

'19

the globe and mail, source: j.p. morgan

asset management

International stocks pay more in dividends

than U.S. stocks

Dividend yields on stocks outside the U.S. minus

the dividend yield on S&P 500

2.0%

1.8

Nov. 16, 2021:

1.5%

1.6

1.4

Avg. 1.1%

1.2

1.0

0.8

0.6

0.4

'01

'03

'05

'07

'09

'11

'13

'15

'17

'19

the globe and mail, source: j.p. morgan

asset management

International stocks pay more in dividends than U.S. stocks

Dividend yields on stocks outside the U.S. minus the dividend yield on S&P 500

2.0%

1.8

Nov. 16, 2021:

1.5%

1.6

1.4

Avg. 1.1%

1.2

1.0

0.8

0.6

0.4

'01

'03

'05

'07

'09

'11

'13

'15

'17

'19

the globe and mail, source: j.p. morgan asset management

It is a tough call. On the one hand, it is difficult to overlook the long history of U.S. outperformance. On the other hand, U.S. stocks now look screamingly expensive no matter how you slice the numbers.

Consider the cyclically adjusted price-to-earnings ratio, or CAPE, a gauge of how stock markets stack up against their long-run earnings. To arrive at its long-view judgment, CAPE compares the current level of stock prices to their inflation-adjusted average annual earnings per share over the past decade.

U.S. stocks are now trading at a CAPE of more than 42, according to Citigroup analysts. That is more than double the historical average and the highest level since the dot-com bubble of the late 1990s. By comparison, Canadian stocks are selling for a CAPE of 27, European stocks for a CAPE of 23, Japanese stocks for a CAPE of 24 and Asian stocks outside of Japan for a CAPE of 20.

The takeaway is clear: Everything outside the U.S. looks cheap in comparison to a made-in-America portfolio.

The same message comes through when you look at other yardsticks of value.

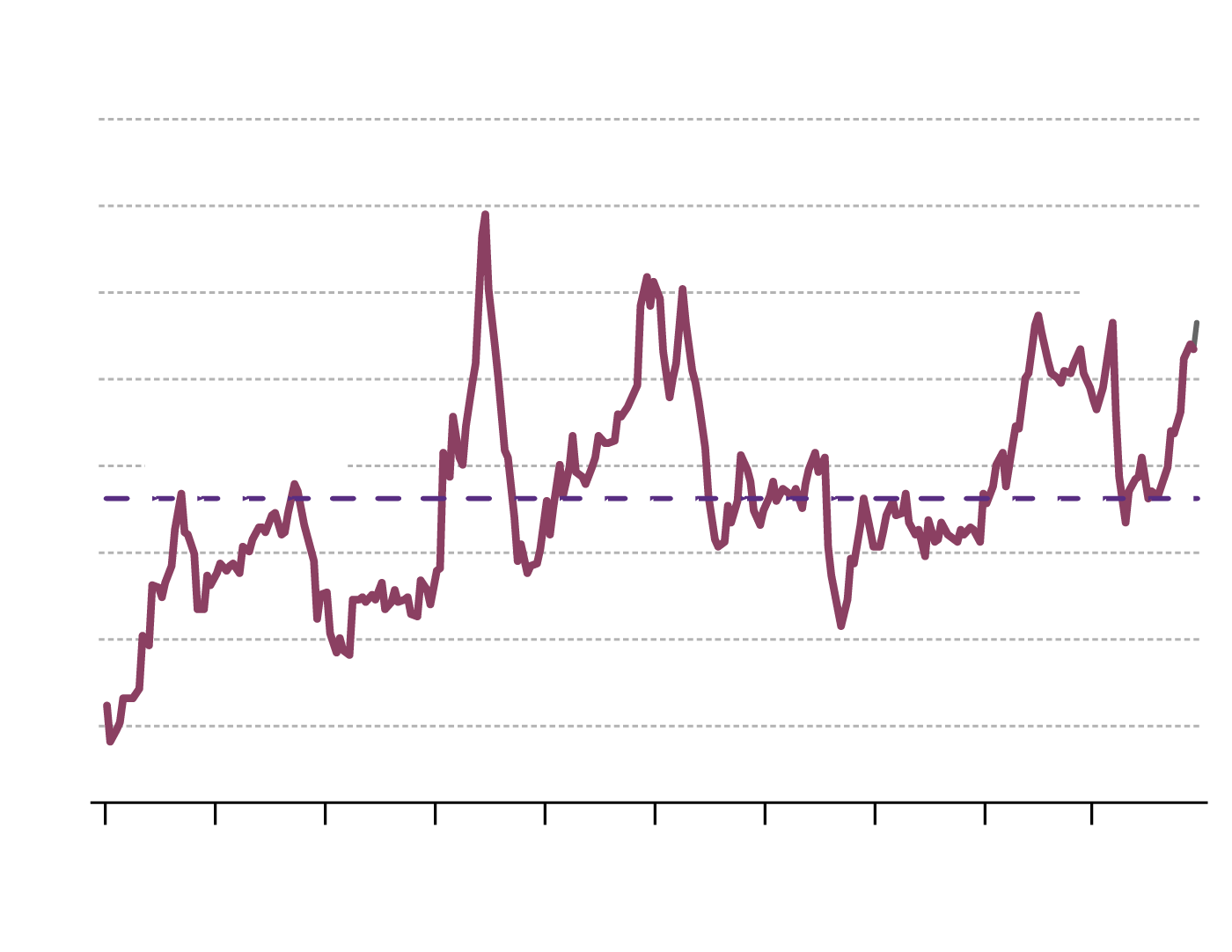

International stocks are now trading at a valuation discount of more than 30 per cent against U.S. stocks when measured on their prices versus expected earnings over the next 12 months, according to analysts at J.P. Morgan Asset Management.

International stocks are also delivering much higher dividends than U.S. stocks, according to the J.P. Morgan crew. On both measures, they appear cheap, and their relative cheapness vis-à-vis U.S. stocks has been growing.

Is there some logical way to explain this widening valuation gap? Some argue it is a composition effect. Tech stocks have been the big success story of the past two decades, and the U.S. market holds far more of them as a proportion of the market index than non-U.S. markets.

International stocks look cheap vs. U.S. stocks

Price-to-earnings ratio of stocks outside the U.S.

compared to price-to-earningsratio of the S&P 500

10%

5

0

-5

-10

Avg. -13.1%

-15

-20

-25

-30

Nov. 16, 2021:

-31.6%

-35

'01

'03

'05

'07

'09

'11

'13

'15

'17

'19

the globe and mail, source: j.p. morgan

asset management

International stocks look cheap vs. U.S. stocks

Price-to-earnings ratio of stocks outside the U.S. compared

to price-to-earningsratio of the S&P 500

10%

5

0

-5

-10

Avg. -13.1%

-15

-20

-25

-30

Nov. 16, 2021:

-31.6%

-35

'01

'03

'05

'07

'09

'11

'13

'15

'17

'19

the globe and mail, source: j.p. morgan

asset management

International stocks look cheap vs. U.S. stocks

Price-to-earnings ratio of stocks outside the U.S. compared to price-to-earningsratio of the S&P 500

10%

5

0

-5

-10

Avg. -13.1%

-15

-20

-25

-30

Nov. 16, 2021:

-31.6%

-35

'01

'03

'05

'07

'09

'11

'13

'15

'17

'19

the globe and mail, source: j.p. morgan asset management

But this explanation doesn’t satisfy. When you compare apples to apples – an Asian automaker to a U.S. automaker, for instance, or a European bank to a U.S. one – investors typically assign a higher valuation to the U.S. company, according to a recent analysis by Capital Economics.

“The valuation of U.S. equities has long been higher than that of their counterparts in the rest of the world, but the gap is much larger than usual at the moment,” wrote Oliver Jones, senior markets economist.

The challenge for investors is what to make of this gap. A good first step is to be aware of the dangers lurking behind those record stock market closes on Wall Street. For now, rock-bottom bond levels are supporting lofty U.S. share prices. Strong earnings could propel stocks even higher in the short term. But if rates start moving up, or earnings growth tapers, U.S. stock valuations have a long, long way to fall to get back to historically average levels.

On a more positive note, the valuation gap suggests investors should open their eyes to potential elsewhere in the world. Canadian stocks offer a good starting place, for sure, but Europe, Asia and Latin America also hold promise and can be easily purchased through low-cost exchange-traded funds from the likes of Vanguard and iShares.

Now is an excellent time to ensure your portfolio is globally diversified. At some point, buying low will come back into fashion.

Be smart with your money. Get the latest investing insights delivered right to your inbox three times a week, with the Globe Investor newsletter. Sign up today.