Since the start of the COVID-19 pandemic, the S&P 500 Index has gained a little over 100 per cent.Spencer Platt/Getty Images

Investors these days have bubbles on the brain.

Fears of a speculative bubble in artificial intelligence have hijacked the conversation about financial markets, with everyone from the International Monetary Fund to the Bank of England to your next-door neighbour in agreement.

If people calling bubbles were an asset class you could invest in, that would be a bubble. Dread has become the consensus. Any time tech stocks stumble, as they did this past week, investors wonder whether the reckoning is upon them.

The stock market bubble that just won’t die

It’s time to pump the brakes. Things are not as scary as they might seem.

When the stock market is at its most irrational and dangerous, you see company valuations divorce themselves from underlying fundamentals. That’s not really what’s happening, at least not on the same scale as past financial bubbles.

Yes, this is a time of high hopes and high valuations. Trillions of dollars are riding on AI fulfilling its potential as the next great technological step change.

But this is not the dot-com bubble, which was fuelled by hype and torrents of debt. Today’s bull market is being led by companies with strong balance sheets and legitimate earnings.

“It’s really a different thing,” Federal Reserve chair Jerome Powell said last week. “These companies actually have business models and profits.”

It’s worth drilling into corporate profits, since they are at the heart of this era in financial markets that we can trace back to the start of the COVID-19 pandemic.

Over that time, the S&P 500 Index has gained a little over 100 per cent – a run made all the more incredible for the fact that it included a pandemic, a breakdown of the global supply chain, double-digit inflation, one of the most aggressive campaigns of interest-rate hikes in history and a global trade war.

Now, what has been the primary force guiding the stock market to such great heights? It wasn’t investor FOMO. Earnings growth, with dividends factored in, was responsible for more than three-quarters of the upside.

Corporate America has become a profit-making machine. Over the past 20 years, earnings per share generated by companies in the S&P 500 have more than tripled. And the Street’s estimates have them going up another 14 per cent in 2026.

Pretty much everyone expected the earnings streak to fall apart this year, when the Trump administration started slapping tariffs on everything it imports. Since tariffs are a tax on U.S. businesses, their effect would be twofold.

Some of the tariffs would be absorbed at the company level, squeezing profit margins, it was said. The rest would be passed onto consumers, raising inflation. Neither has happened. Inflation is muted and profit margins are up – 13.4 per cent as of the end of September and projected to rise further over the next year.

Big business has found ways to dodge tariffs, in part by stockpiling vast amounts of imports earlier in the year, before tariffs took effect. As they run out of levers to pull, it’s possible “the impact will start to bleed into earnings and margins,” Craig Basinger, chief market strategist at Purpose Investments, said in a note.

“But it may be gradual and probably less noticeable to a market hooked on headlines.”

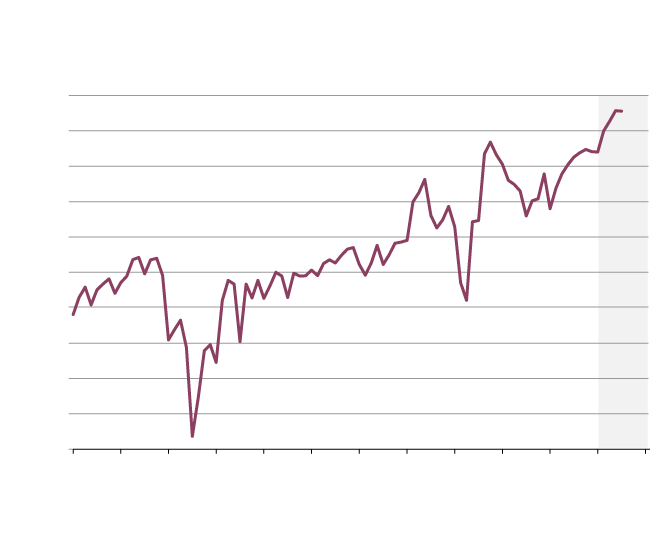

Record profitability fuels the bull market

S&P 500 quarterly profit margins (%)

15%

14

13

12

11

10

9

8

ESTIMATE

7

6

5

2003

‘05

‘07

‘09

‘11

‘13

‘15

‘17

‘19

‘21

‘23

‘25

‘27

the globe and mail, Source: Scotiabank GBM Portfolio Strategy

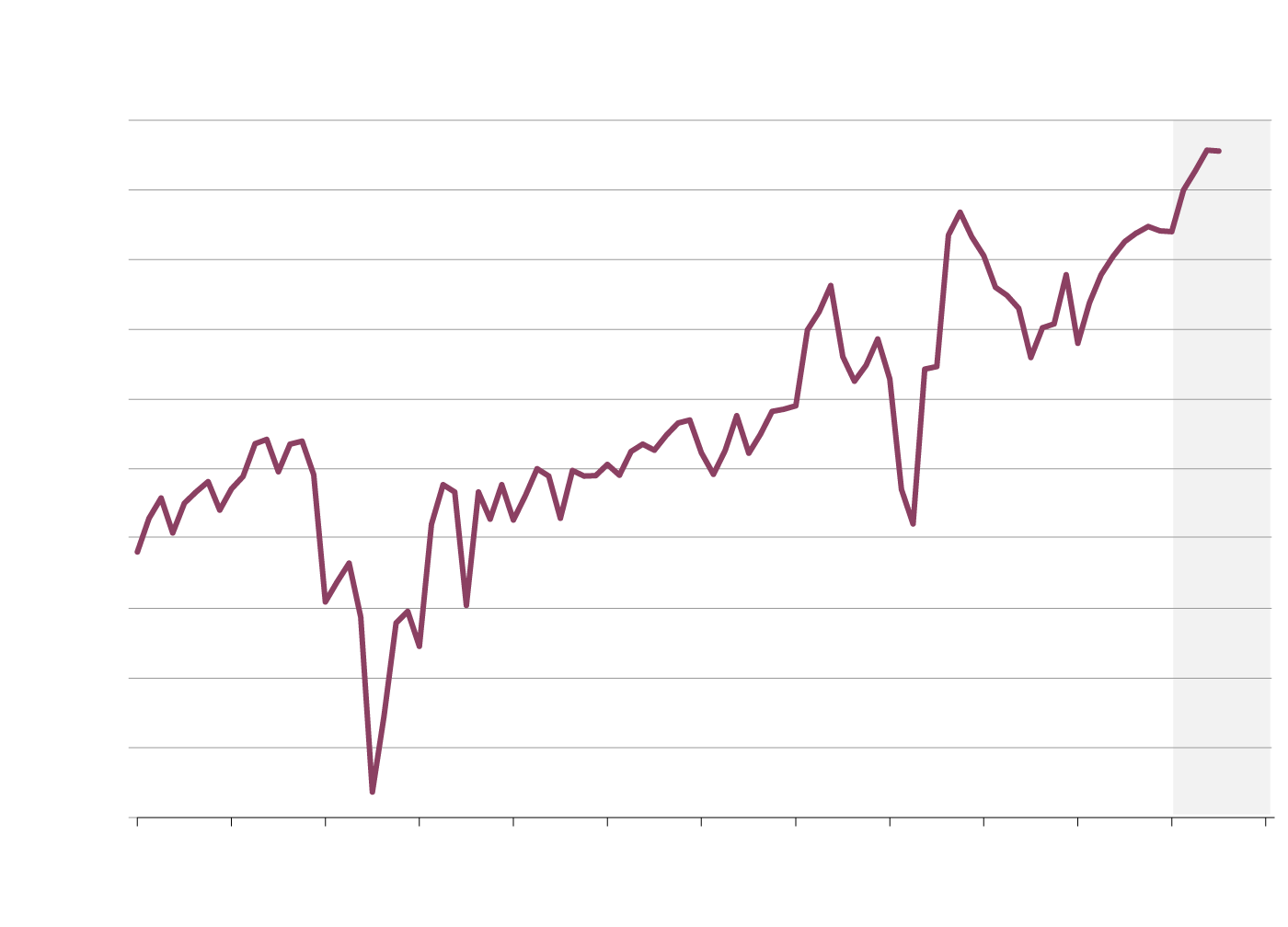

Record profitability fuels the bull market

S&P 500 quarterly profit margins (%)

15%

14

13

12

11

10

9

8

ESTIMATE

7

6

5

2003

‘05

‘07

‘09

‘11

‘13

‘15

‘17

‘19

‘21

‘23

‘25

‘27

the globe and mail, Source: Scotiabank GBM Portfolio Strategy

Record profitability fuels the bull market

S&P 500 quarterly profit margins (%)

15%

14

13

12

11

10

9

8

ESTIMATE

7

6

5

2003

‘05

‘07

‘09

‘11

‘13

‘15

‘17

‘19

‘21

‘23

‘25

‘27

the globe and mail, Source: Scotiabank GBM Portfolio Strategy

There’s not much to strike fear in the hearts of investors on the earnings side. What is making people nervous are rising valuations, which are responsible for around 25 per cent of the gains in U.S. stocks over the last five-plus years.

By any metric, U.S. stocks are richly priced, even worryingly so. Everywhere you look in financial media, you see parallels to the dot-com bubble, which set the high-water mark for speculative excess.

Back then, there was no price too high to get in on the action. Are investors making the same mistake with AI as they made with the advent of the internet?

“I don’t detect that level of mania at this time, so I have not put the bubble label on this incident,” Howard Marks, co-founder of Oaktree Capital, said in a recent interview on CNBC.

Other highly influential names are aligned with that view.

Larry Fink, CEO of BlackRock Inc.: “I don’t believe this is a bubble, but I believe this is capital that in most cases is going to be well spent.”

Peter Oppenheimer, chief global equity strategist at Goldman Sachs: “Valuations of the technology sector are becoming stretched but not yet at levels consistent with historical bubbles.”

Of course, I could just as easily build a case on the other side with a compilation of credible voices calling this a bubble.

At some point, it’s futile for the average investor to try to figure out which side they fall on. Bubble or no, you can continue to participate in the stock market without fixating on whether disaster looms.

If retirement is still a long way off, you don’t need to care at all. Even major market crashes fade to irrelevance over the course of a decades-long investing horizon. Older investors can hedge against tech froth with bonds, cash and diversified stocks.

Where you can get into real trouble is trying to pick winners and losers. When this all shakes out, there will be far more of the latter, precious few of the former and heartbreak for the many who pick wrong.