A SpaceX building and Starship rocket in Starbase, Tex., on June 11. SpaceX, which went public last month, is now trading about US$150 a share.Gabriel V. Cardenas/Reuters

If you’re looking for evidence that the stock market has lost its mind, a good place to start is by reading this week’s flood of adoring SpaceX SPCX-Q reports.

Investment banks that help to take stocks public are required to stay quiet for a period after an initial public offering. For SpaceX underwriters, that period just ended. They rushed to issue reports that lavished “buy” and “outperform” ratings on Elon Musk’s fledgling attempt to conquer the solar system.

To be sure, anyone familiar with the market realizes these recommendations aren’t meant to be taken literally. They’re just Wall Street theatre, a way for underwriters to demonstrate their unswerving loyalty to SpaceX (more properly known as Space Exploration Technologies Corp.). The banks’ public demonstration of enthusiasm helps to justify the massive fees they charged for taking the company public a month ago.

SpaceX shares slipped despite early Nasdaq-100 inclusion

That said, you still have to admire the fanboy fervour with which some of the bank analysts beat the drum for SpaceX, which is now trading around US$150 a share.

Deutsche Bank, in a note entitled “Apex of Civilizational Ambition,” put a one-year price target of US$255 on the stock and added that the company is “bending the arc of history to make humans multiplanetary.” Not to be outdone, Citigroup pasted a US$200 target on the stock but said even that gain is just “a milestone along the path to $900+ which becomes realistic assuming key engineering achievements are demonstrated at scale.”

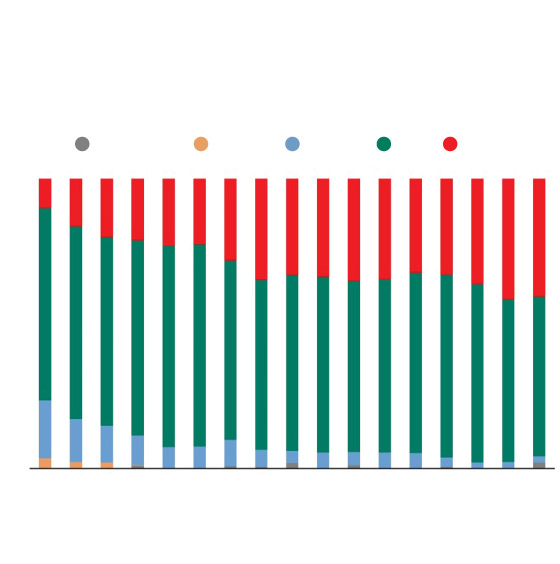

The battle for AI dominance

U.S. companies are pouring trillions of dollars into AI, but Chinese

competitors are gaining market share.

(Origin of the world’s 50 most used AI models, number)

Unattributed

Canada

France

U.S.

China

50

40

30

20

10

0

J

F

M

A

M

J

J

A

S

O

N

D

J

F

M

A

M

2025

2026

the globe and mail, Source: Apollo Global Management

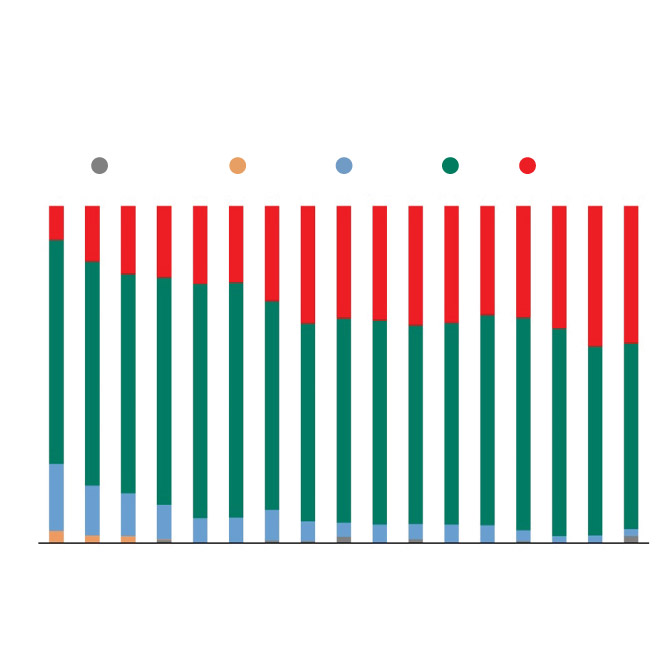

The battle for AI dominance

U.S. companies are pouring trillions of dollars into AI, but Chinese

competitors are gaining market share.

(Origin of the world’s 50 most used AI models, number)

Unattributed

Canada

France

U.S.

China

50

40

30

20

10

0

J

F

M

A

M

J

J

A

S

O

N

D

J

F

M

A

M

2025

2026

the globe and mail, Source: Apollo Global Management

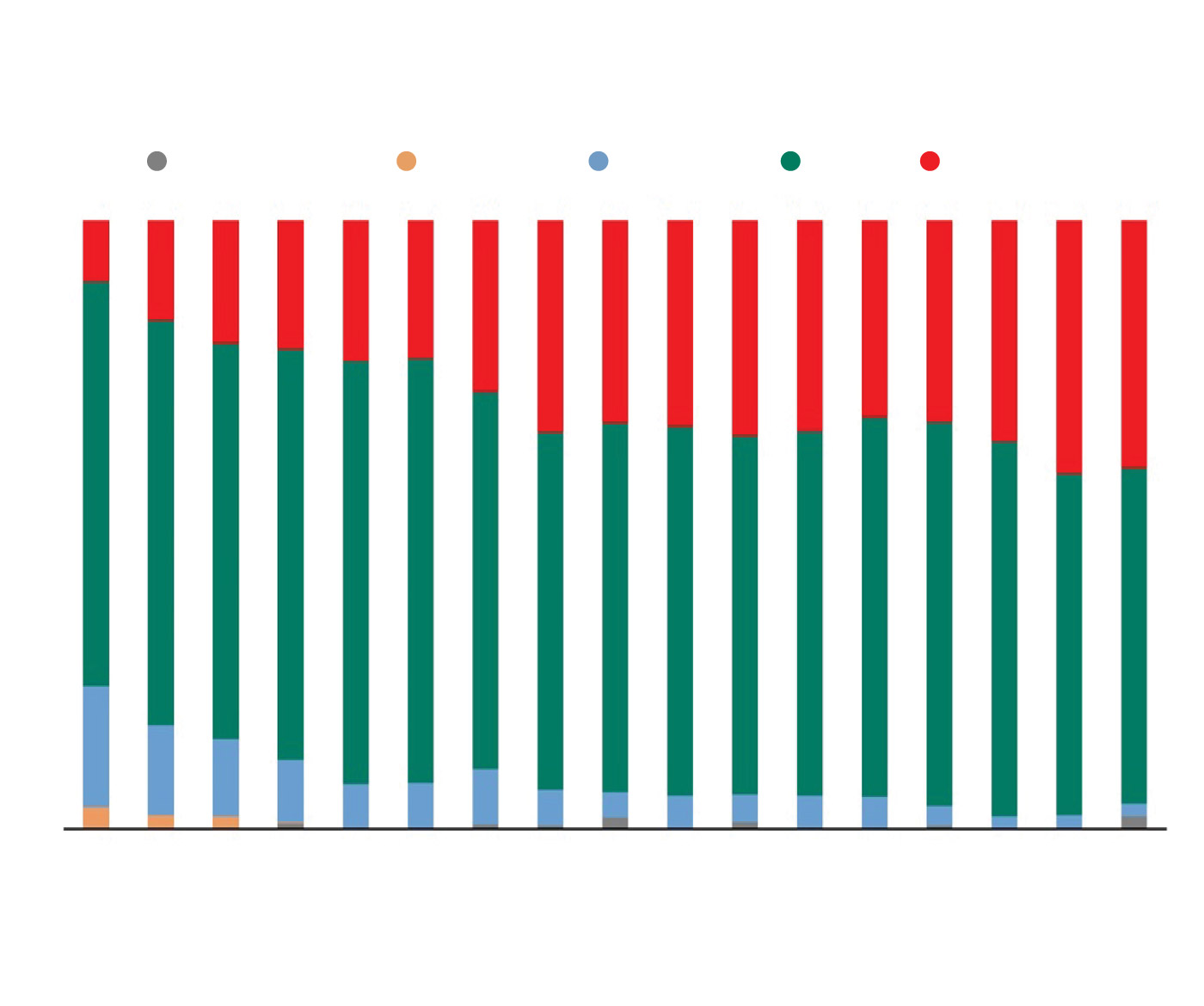

The battle for AI dominance

U.S. companies are pouring trillions of dollars into AI, but Chinese competitors are gaining market share.

(Origin of the world’s 50 most used AI models, number)

Unattributed

Canada

France

U.S.

China

50

40

30

20

10

0

J

F

M

A

M

J

J

A

S

O

N

D

J

F

M

A

M

2025

2026

the globe and mail, Source: Apollo Global Management

Really? You don’t have to be a troll to notice that the word “assuming” is doing an awful lot of work in that last sentence. Yes, assuming everything turns out perfectly, SpaceX could one day make a profit and justify its current share price. For now, though, it remains a money-losing company with a hodgepodge of speculative bets that may or may not work out.

What Wall Street’s gushing support for SpaceX really demonstrates is the anything-goes mentality that has become standard in a market driven mad by excitement over artificial intelligence (AI). Euphoria is everywhere. Valuations are stretched.

This is not a secret. In May, the Bank of Canada pointed out that several measures of market ebullience are hovering near historic highs. Last month, the Bank for International Settlements, a key adviser to the world’s central banks, warned that the “current AI exuberance” runs the risk of turning into “a protracted investment bust.” The latest Financial Stability Report from the Bank of England, published this week, contains a helpful chart showing that the benchmark S&P 500 index is now more expensive relative to long-run fundamentals than at any time since the dot-com bubble of more than two decades ago.

So why aren’t markets faltering? The short answer is that corporate earnings are still going through the roof. In fact, profits for companies in the benchmark S&P 500 index are expected to be 23 per cent higher this quarter than a year ago, according to the analysts at FactSet.

A profit boom of this magnitude would ordinarily be cause for celebration. What should limit the celebration, though, is how dependent those profits are on the spending boom around AI.

Goldman Sachs estimates that U.S. companies are on track to invest a staggering US$7.6-trillion into AI-related capital expenditures between now and 2031. Technology investment now accounts for nearly 5 per cent of economic output – “a share higher than at the peak of the dot-com bubble,” according to Ryan Cummings of the Stanford Institute for Economic Policy Research.

Expectations for companies related to AI are now so elevated, and nerves so tight, that anything short of perfection can capsize a stock. Consider the rather absurd case of Samsung Electronics Co. SSNLF, the South Korean tech giant, which this week reported a 19-fold increase in its operating profit – then watched its stock price slide because investors had hoped for even better results.

The broader challenge for the market as a whole is sustainability. So far, there is little sign that AI is generating the level of profits that would provide a reasonable payback on the torrent of money going into the sector. Just the opposite: Low-cost Chinese competitors are gobbling up an increasing share of the AI market. Free cash flow at big tech companies is dwindling rapidly.

This is setting up an interesting contest between the high hopes around AI and the financial reality of providing it. If the optimists are right, AI pioneers such as OpenAI and Anthropic, as well as “hyperscalers” such as Microsoft Corp. MSFT-Q – and, yes, SpaceX, too – will soon wallow in huge new streams of AI profits.

But success isn’t guaranteed. If those profits don’t start to materialize soon – say, within the year or so – the market’s mood could change. The same companies that are now spending so lavishly could cut back their capital expenditures and today’s boom could turn to bust.

“The bottom line is that AI has been the one thing holding up both the economy and markets,” Torsten Slok, chief economist at Apollo Global Management, wrote this week. “With so much riding on so few names, a slower payoff wouldn’t just be a sector problem, it would risk tipping the economy into recession and the S&P 500 into a correction.” Let’s keep our fingers crossed.