Lumentum's Component Business Accelerates: More Upside Ahead?

Lumentum Holdings’ LITE component business is accelerating rapidly, positioning the company for continued revenue growth as AI-driven demand for optical networking solutions remains robust. In the third quarter of fiscal 2026, Lumentum's Components segment generated a record $533.3 million, accounting for 66% of total revenues, while revenues climbed 20.2% sequentially and 77.3% year over year, underscoring that components have become the primary engine of its business expansion.

The strong performance was driven by record shipments of electro-absorption modulated laser (EML) chips, more than 120% year-over-year growth in narrow-linewidth laser assemblies and 80% growth in pump lasers, fueled by rising demand from hyperscale AI data centers. Management also noted that several high-growth component categories remain effectively sold out, while its Japan wafer fabrication capacity is fully allocated, indicating sustained customer demand and strong revenue visibility.

Lumentum is also laying the groundwork for its next phase of growth through ultra-high-power laser chips and co-packaged optics (CPO), which management expects to become meaningful revenue contributors later in 2026. The richer mix of premium AI components helped lift non-GAAP operating margin to 32.2% in the reported quarter, demonstrating that the company is not only growing revenue but also improving profitability.

Lumentum's recent updates underscore that optical components are becoming indispensable to next-generation AI infrastructure, with co-packaged optics emerging as another meaningful growth driver. As hyperscale cloud providers accelerate investments in AI networking, the company's expanding portfolio of advanced optical components is well positioned to capture this demand. Its increased fourth-quarter fiscal 2026 revenue guidance of $960 million-$1.01 billion further suggests that management expects the strong momentum in the Components segment to continue, strengthening LITE's long-term growth outlook.

Lumentum Faces Stiff Competition

Lumentum faces stiff competition from Coherent Corp.COHR and Applied OptoelectronicsAAOI as AI-driven demand for optical components, photonics and data center networking continues to accelerate.

Coherent challenges Lumentum through broad photonics capabilities, 800G/1.6T transceivers, optical circuit switches and co-packaged optics. Coherent strengthens its edge with 6-inch indium phosphide production, long-term supply agreements and aggressive capacity expansion. The company also benefits from robust AI networking demand, expanding backlog and differentiated manufacturing scale.

Applied Optoelectronics competes with Lumentum by scaling 800G and 1.6T transceivers, expanding U.S. manufacturing and leveraging in-house laser production. Applied Optoelectronics emphasizes automation, production flexibility and capacity growth to address accelerating AI infrastructure demand. It also targets co-packaged optics and hyperscale customers, reinforcing its long-term growth strategy.

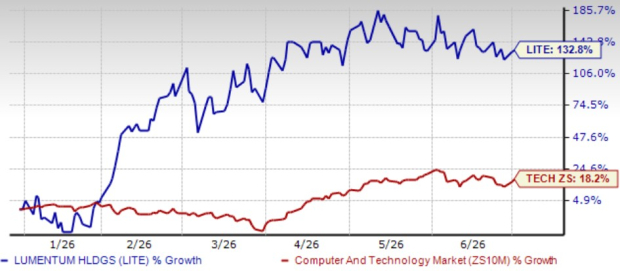

LITE’s Share Price Performance, Valuation & Estimates

Shares of LITE have surged 132.8% year to date compared with the Computer and Technology sector’s growth of 18.2%.

LITE’s YTD Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, LITE trades at a forward price-to-sales ratio of 22.26X, significantly higher than the sector’s average of 6.62X. LITE carries a Value Score of F.

LITE’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for LITE’s fiscal 2027 earnings implies year-over-year growth of 118.77%. The consensus estimate for fiscal 2027 has been revised upward in the past 30 days.

Image Source: Zacks Investment Research

Lumentum stock carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).