Buy 2 AI Memory Giants at Lucrative Valuations Amid Solid Price Upside

The astonishing bull run of Wall Street over the last three years faced hurdles in March. Concerns about the continuation of artificial intelligence (AI) trade and the breakout of war in the Middle East significantly dented market participants’ confidence in risky assets like equities. Investors booked profits on AI-driven technology stocks for which valuations were already overstretched.

Despite these headwinds, we have selected two AI chip behemoths with a favorable Zacks Rank that are currently trading at lucrative intervals. These stocks have seen double-digit price declines in the past month. However, their strong business outlook has made them highly attractive at current valuations.

These stocks are: Micron Technology Inc. MU and Analog Devices Inc.ADI. At their current valuations, these stocks offer huge short-term price upside. Each of our picks currently carries either a Zacks Rank #1 (Strong Buy) or 2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

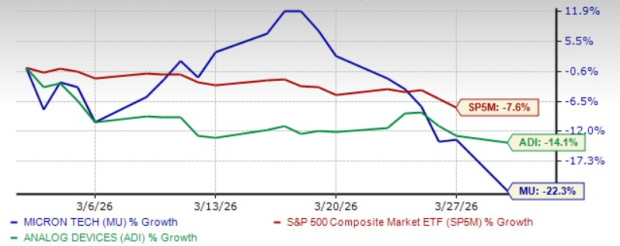

The chart below shows the price performance of our two picks in the past month.

Image Source: Zacks Investment Research

Micron Technology Inc.

Zacks Rank #1 Micron Technology is benefiting from the rapidly expanding AI-driven memory and storage markets. The positive impacts of inventory improvement across multiple end markets are driving top-line growth.

MU has become a leader in the AI infrastructure boom due to strong demand for its high-bandwidth memory (HBM) solutions. Record sales in the data center end market and accelerating HBM adoption have been driving MU’s Dynamic Access Random Memory (DRAM) revenues higher.

The growing adoption of AI servers is reshaping the DRAM market as these systems require significantly more memory than traditional servers. This is boosting demand for both high-capacity DIMMs (Dual In-line Memory Module) and low-power server DRAM.

MU is capitalizing on this trend with its leadership in DRAM technology and a strong product roadmap that includes HBM4, slated for volume production in 2026. MU’s investments in next-generation DRAM and 3D NAND ensure that it remains competitive in delivering the performance needed for modern computing.

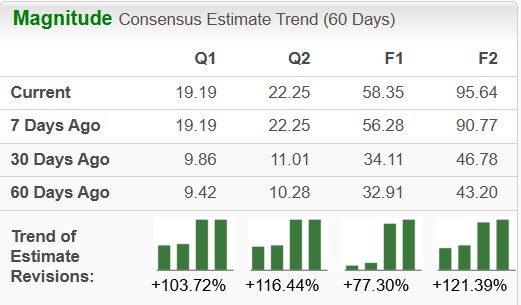

Strong Estimate Revisions

Micron Technology has an expected revenue and earnings growth rate of more than 100% each, respectively, for the current year (ending August 2026). The Zacks Consensus Estimate for the current year’s earnings has improved 3.7% over the past seven days.

For the next year (ending August 2027), the company has an expected revenue and earnings growth rate of 56.1% and 63.9%, respectively. The Zacks Consensus Estimate for the next year’s earnings has improved 5.4% over the past seven days.

Image Source: Zacks Investment Research

Massive Price Upside Potential

Micro Technology is currently trading at an attractive valuation compared to its peers. The stock has a forward price/earnings (P/E) ratio of 6.12X, well below the industry’s P/E of 19.03X and the S&P 500’s P/E of 17.91X.

The short-term average price target of brokerage firms for the stock represents an increase of 52% from the last closing price of $321.80. The brokerage target price is currently in the range of $140-$750. This indicates a maximum upside of 133.1% and a downside of 56.5%. The risk/reward ratio is 1:2.4.

Analog Devices Inc.

Zacks Rank #2 Analog Devices’ latest quarterly results demonstrate broad-based recovery, margin resilience and strong free cash flow generation. Secular growth drivers in automation, AI infrastructure and automotive electrification provide multi-year tailwinds.

ADI’s robust top-line performance was primarily driven by strong growth in its industrial, aerospace and defense businesses, fueled by demand for AI chip infrastructure buildout, automated test equipment, and a rebound in automation and healthcare markets.

Strong momentum across the electric vehicle space on ADI’s robust Battery Management System solutions remains a tailwind. ADI’s strong investments in technology and business innovation are contributing well.

ADI’s hybrid manufacturing strategy provides a significant competitive advantage by balancing internal production capacity with external partnerships. This approach enhances supply-chain flexibility and reduces geopolitical risk, ensuring consistent product availability for customers.

By the end of 2026 or early 2027, 95% of ADI’s products will have at least dual sourcing, reducing reliance on any single geography. Key partnerships and internal fab investments position ADI for sustainable growth. ADI’s strong cash flow generation capability and aggressive shareholder return policies are other positives.

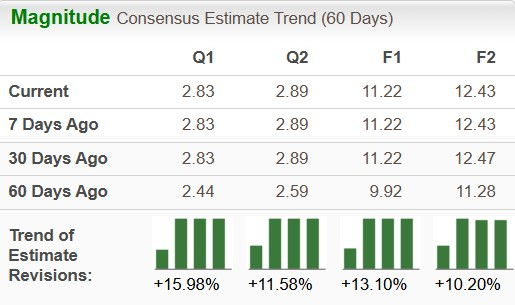

Strong Estimate Revisions

Analog Devices has an expected revenue and earnings growth rate of 25.15 and 44%, respectively, for the current year (ending October 2026). The Zacks Consensus Estimate for the current year’s earnings has improved 13.1% over the past 60 days.

For the next year (ending October 2027), the company has an expected revenue and earnings growth rate of 8.4% and 10.8%, respectively. The Zacks Consensus Estimate for the next year’s earnings has improved 10.2% over the past 60 days.

Image Source: Zacks Investment Research

Impressive Price Upside Potential

Analog Devices has a forward price/earnings (P/E) ratio of 27.41X, compared with the industry’s P/E of 32.97X and the S&P 500’s P/E of 17.91X. The short-term average price target of brokerage firms for the stock represents an increase of 27.9% from the last closing price of $303.10. The brokerage target price is currently in the range of $280-$430. This indicates a maximum upside of 41.9% and a downside of 7.6%. The risk/reward ratio is 1:5.5.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Micron Technology, Inc. (MU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).