TXN's Manufacturing Expansion Continues: Can It Strengthen Margins?

Texas Instruments Incorporated’s TXN long-term manufacturing expansion strategy is beginning to show meaningful benefits, raising the question of whether it can drive stronger profit margins in the years ahead. Unlike many semiconductor companies that rely heavily on third-party foundries, Texas Instruments has invested aggressively in its manufacturing network, particularly 300-millimeter wafer fabrication facilities.

The company has spent billions of dollars expanding capacity across sites in Texas and Utah over the past several years. While these investments initially pressured profitability through higher depreciation and operating costs, they are designed to lower production costs over time. Larger 300-millimeter wafers produce significantly more chips per manufacturing run than traditional 200-millimeter wafers, improving efficiency and reducing cost per chip.

The benefits are already becoming visible. In the first quarter of 2026, Texas Instruments reported a gross margin of 58%, an improvement of 120 basis points (bps) from the year-ago quarter. Revenues rose 19% year over year to $4.83 billion, while operating profit climbed 37% to $1.81 billion. The operating margin was 37.5%, which expanded by 490 bps from the prior-year quarter’s number. Stronger factory utilization, combined with growing demand in industrial and data center markets, helped improve profitability.

The company’s internal manufacturing push gives it a competitive advantage during periods of industry tightness. Texas Instruments can support customers with stable lead times while competitors face supply constraints. This capability may also create opportunities to gain market share.

Although depreciation expenses are expected to remain elevated in 2026, capital expenditures are projected to decline to $2-$3 billion from more than $4 billion over the past 12 months. As revenues continue to recover and factory utilization improves, Texas Instruments’ manufacturing investments could become an increasingly important driver of margin expansion.

How TXN’s Rivals Are Improving Manufacturing Efficiency

Analog Devices, Inc.ADI is a major competitor in the analog semiconductor market and continues to focus on manufacturing efficiency to protect margins. The company operates a mix of internal production facilities and outsourced manufacturing partners.

Analog Devices has historically delivered gross margins above 60%, benefiting from its high-value industrial and automotive products. The company is also integrating manufacturing assets acquired through past acquisitions to improve scale and cost efficiency. In the second quarter of fiscal 2026, Analog Devices’ adjusted gross margin expanded 360 bps year over year to 73%, while adjusted operating margin improved 780 bps to 49%.

NXP Semiconductors N.V.NXPI is another key rival investing to strengthen profitability. The company has expanded its internal manufacturing capabilities while maintaining relationships with external foundries.

NXP Semiconductors generates a gross margin in the mid-to-high 50% range and has benefited from strong demand in automotive and industrial markets. Its manufacturing strategy focuses on balancing flexibility with cost control. In the first quarter of 2026, NXP Semiconductors’ non-GAAP gross margin expanded 100 bps year over year to 57.1%, while non-GAAP operating margin improved 120 bps to 33.1%.

TXN’s Price Performance, Valuation and Estimates

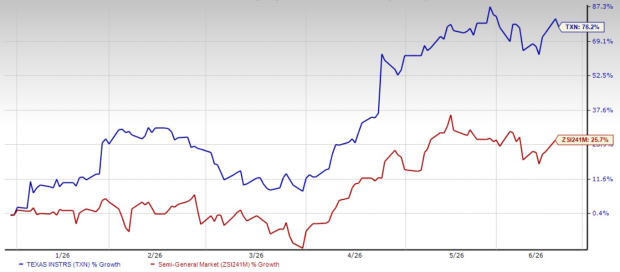

Shares of Texas Instruments have soared 76.2% year to date compared with the Zacks Semiconductor - General industry’s 25.7% gain.

Texas Instruments YTD Price Return Performance

Image Source: Zacks Investment Research

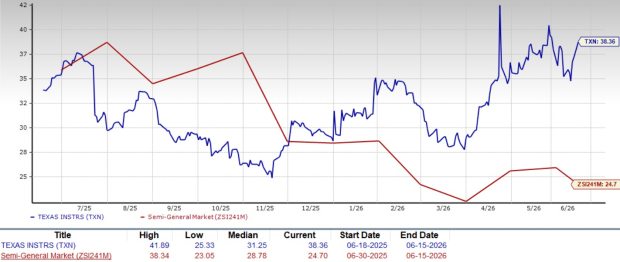

From a valuation standpoint, TXN trades at a forward price-to-earnings ratio of 38.36, significantly higher than the industry’s average of 24.70.

Texas Instruments Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Texas Instruments’ 2026 and 2027 earnings implies a year-over-year increase of 40.6% and 14.4%, respectively. Estimates for 2026 and 2027 have been revised upward in the past 60 days.

Image Source: Zacks Investment Research

Texas Instruments currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).