Affirm Stock Falls 33% YTD: Should Investors Buy the Dip Now?

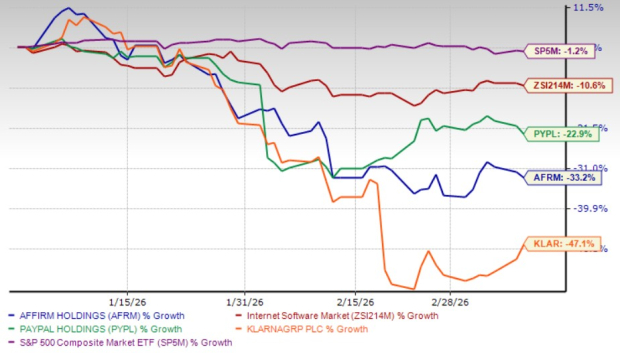

Shares of Affirm Holdings, Inc.AFRM have plunged 33.2% in the year-to-date period, underperforming the S&P 500’s 1.2% drop and the industry’s 10.6% decline. Even major buy now, pay later (BNPL) providers PayPal Holdings, Inc.PYPL and Klarna Group plcKLAR have lost 22.9% and 47.1%, respectively, during this time.

Price Performance – AFRM, PYPL, KLAR, Industry & S&P 500

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

What’s Behind the Drop?

Persistent inflation concerns, driven by geopolitical turmoil and rising worries about consumers’ ability to repay debt have weighed on sentiment across the fintech sector. At the same time, intensifying competition in the BNPL market, particularly from Klarna and other fintech players, continues to pressure the space. Investors are also mindful that merchant partnerships can shift quickly, highlighted by Walmart’s decision last year to replace Affirm with Klarna as its exclusive BNPL provider. Additionally, Affirm’s relatively high debt levels have raised balance-sheet concerns.

Together, these factors have pushed the stock lower despite the structurally strong demand for digital payments and installment lending. As a result, Affirm now trades roughly 50.2% below its 52-week high of $100. However, the sharp pullback may be setting the stage for a potential rebound.

AFRM’s Bright Long-Term Picture

Affirm continues to build a foundation for long-term growth through partnerships, product expansion and a growing user base. Its partnership with Shopify is expected to expand into Europe, with launches planned in France, Germany and the Netherlands. This geographic push should broaden Affirm’s addressable market while helping diversify its revenue base. It ended 2025 with 25.8 million active consumers, up 23% year over year, underscoring steady adoption both in the United States and abroad.

The company is also becoming more embedded in everyday spending categories such as groceries, fuel, travel and subscriptions, increasing how frequently consumers interact with its products. It witnessed a 44% jump in transactions to 54.9 million in the last reported quarter, with repeat activity accounting for roughly 96% of the total, a sign of strong customer retention. Merchant adoption remains strong as well, with active merchants climbing 42% year over year to 478,000 by the end of 2025.

Another key growth driver is the Affirm Card. Management is working to scale the card across its user base and position it as a primary access point to the company’s services. Active cardholders surged 121% in the fiscal second quarter, supported by a cash-flow underwriting model that evaluates real-time spending and deposit patterns instead of relying solely on traditional credit scores. Meanwhile, Gross Merchandise Volume rose 36% year over year to $13.8 billion in the fiscal second quarter.

Favorable Earnings Estimates for AFRM

The Zacks Consensus Estimate for fiscal 2026 earnings indicates a 640% year-over-year surge, while the estimate for fiscal 2027 earnings implies growth of 58.2%. Moreover, the consensus mark for fiscal 2026 and 2027 revenues suggests 28.5% and 24.9% year-over-year growth, respectively.

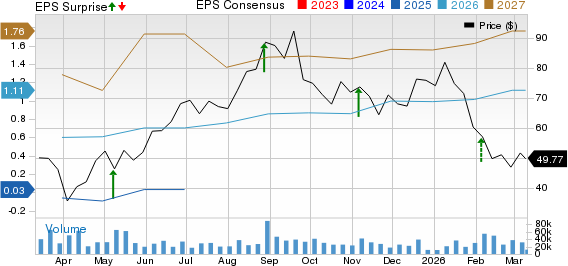

It has delivered solid financial results lately, beating earnings estimates in each of the trailing four quarters, the average surprise being 83.5%.

Affirm Holdings, Inc. Price, Consensus and EPS Surprise

Affirm Holdings, Inc. price-consensus-eps-surprise-chart | Affirm Holdings, Inc. Quote

AFRM’s Valuation

In terms of valuation, the company is cheaply priced compared with the industry average. Currently, AFRM is trading at 3.41X forward 12-month sales, below its five-year median of 4.57X and the industry’s average of 3.98X. So, there is more room to grow.

In comparison, PayPal and Klarna are trading at forward P/S of 1.20X and 2.37X, respectively.

Conclusion

Affirm’s sharp year-to-date decline reflects broader pressure on the fintech and BNPL space, driven by inflation concerns, credit risk worries and rising competition. The loss of the Walmart partnership and balance-sheet concerns also weigh on investor sentiment. However, the company’s long-term growth drivers remain intact. Expanding merchant relationships, rising consumer adoption and increasing use cases across everyday spending categories continue to support transaction growth.

International expansion through its partnership with Shopify, along with momentum in products like the Affirm Card, should further strengthen its ecosystem and help drive higher Gross Merchandise Volume over time. With strong earnings growth expectations and a valuation that remains below historical levels, the stock could regain momentum if execution remains solid. Still, macroeconomic uncertainty and competitive pressures warrant some caution. Affirm currently carries a Zacks Rank #3 (Hold), suggesting investors may want to stay on the sidelines while monitoring the company’s growth trajectory and profitability progress. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PayPal Holdings, Inc. (PYPL): Free Stock Analysis Report

Affirm Holdings, Inc. (AFRM): Free Stock Analysis Report

Klarna Group plc (KLAR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).