MRVL Appreciates 29% YTD: Time to Buy, Sell or Hold the Stock?

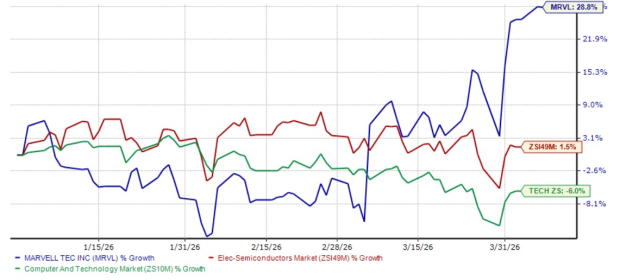

Marvell TechnologyMRVL shares have gained 28.8% year to date, outperforming the Zacks Electronics - Semiconductors industry and the Zacks Computer and Technology sector. While the industry has returned 1.5%, the broader sector has declined 6% in the same time frame.

MRVL YTD Performance Chart

Image Source: Zacks Investment Research

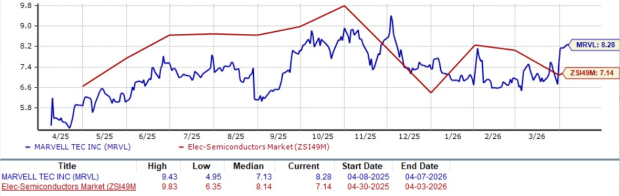

The outperformance has led to MRVL stock’s forward 12-month P/S multiple trading at 8.28X compared with the industry’s multiple of 7.14X, implying that the stock is trading at a premium. The overvaluation of MRVL stock is further substantiated by Zacks Value Score of D. Given the outperformance and overvaluation, investors are wondering if this is the right time to invest in MRVL stock.

MRVL Forward 12-Month (P/S) Valuation Chart

Image Source: Zacks Investment Research

Let’s examine the fundamentals of Marvell Technology to assess what investors’ next move should be.

Strong Demand for AI Products Drives MRVL Stock

Marvell Technology is seeing robust strength for its products as the global AI infrastructure spending rises. MRVL’s data center business alone grew 46% year over year in fiscal 2026 and crossed $6 billion as hyperscalers, AI data centers, AI fabs and high performance computing clients increased their investment, pushing the demand for MRVL’s networking, optical interconnect and custom silicon solutions.

Marvell Technology is also capitalizing on the rising demand for high-speed connectivity, such as 800G and 1.6T optical interconnects. These solutions are gaining traction as AI workloads require faster communication between GPUs and data centers. Based on the current growth trend, MRVL predicts that its interconnect business will grow more than 50% in fiscal 2027.

MRVL’s custom silicon segment reached $1.5 billion in fiscal 2026 and is expected to further increase on the back of the rising demand from hyperscalers. New opportunities, such as XPU attach, CXL memory expansion and scale-up networking, are opening additional revenue streams. These are further amplified by the latest capabilities in AI networking and PCIe/CXL switching from the acquisitions of Celestial AI and XConn Technologies.

MRVL has expanded its partnership with NVIDIA to strengthen its long-term growth outlook by embedding it deeper into the fast-growing AI infrastructure ecosystem. Marvell Technology will integrate into NVIDIA’s AI ecosystem like NVLink Fusion and AI-RAN, enabling customers to build custom AI XPU systems that remain fully compatible with NVIDIA platforms.

By integrating with NVIDIA’s NVLink Fusion platform, Marvell Technology gains direct access to customers building next-generation AI factories, where demand for high-speed connectivity and custom silicon is rising sharply. However, MRVL also experiences some challenges.

MRVL Grapples With Macroeconomic and Competitive Challenges

Macroeconomic and geopolitical uncertainties remain a meaningful overhang on Marvell Technology’s near-term performance. Global trade tensions, evolving U.S. chip export restrictions and tariffs create operational and demand-side risks, particularly given Marvell’s reliance on hyperscalers and global supply chains.

Marvell Technology’s rapid growth in AI-driven custom silicon is heavily tied to hyperscalers, creating concentration risk. In the third quarter of fiscal 2026, 74% of total revenues came from data centers, with more than 90% of that tied to AI and cloud hyperscaler demand. The company faces stiff competition in the networking and custom silicon space from Broadcom AVGO, Astera LabsALAB and Advanced Micro Devices AMD.

Broadcom is a leader in the domain of custom silicon solutions for data centers. Broadcom’s advanced 3.5D XDSiP packaging platform is critical to ensure the performance and efficiency of custom AI XPUs. Advanced Micro Devices is another established player in the custom silicon solutions and AI accelerator market.

Advanced Micro Devices offers semi-custom SoCs and Instinct Accelerators to power data centers. Astera Labs’ Leo CXL smart memory controllers are built for memory expansion up to two terabytes and improve interoperability to accelerate AI performance and cloud computing.

These existing headwinds, along with MRVL’s continuous bottom-line growth rate decline, have become a concern for investors. The company’s bottom-line growth rate has been on a declining trend for the past three quarters. The Zacks Consensus Estimate for MRVL’s first quarter of fiscal 2027 earnings implies growth of 29%, suggesting a further decline in growth rate. The estimate has been revised upward in the past 30 days.

Image Source: Zacks Investment Research

Conclusion: Hold MRVL Stock for Now

Marvell Technology’s strong AI-driven growth, fueled by rising data center demand, expanding custom silicon opportunities and deeper integration with NVIDIA, positions it well for sustained momentum. However, execution risks and competitive pressures remain key watchpoints. Considering these factors, we suggest that investors should retain this Zacks Rank #3 (Hold) stock at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).