Credo Climbs 165% in a Year: Is the Stock Still Worth Buying?

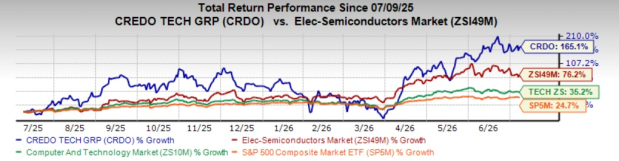

Credo Technology Group Holding Ltd’s CRDO shares have appreciated 165.1% over the past year, outperforming the Zacks Electronics – Semiconductors industry’s growth of 76.2%. The Zacks Computer and Technology sector and the S&P 500 composite have registered growth of 35.2% and 24.7%, respectively, over the same time frame.

The stock has outperformed Broadcom AVGO, which gained 42.1% during the same period. However, Marvell TechnologyMRVL and Astera Labs ALAB have outperformed CRDO, with their shares appreciating 216.7% and 305.3%, respectively, over the past year.

Image Source: Zacks Investment Research

Let us take a closer look at CRDO’s fundamentals, key growth drivers, competitive strengths and potential risks to determine whether the stock remains an attractive investment.

Factors to Consider

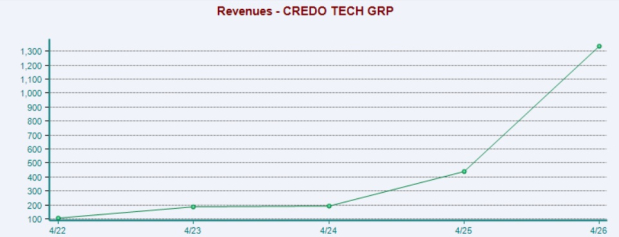

Credo is benefiting from the rapid expansion of AI infrastructure, which continues to drive strong demand for its high-speed connectivity solutions. Fiscal 2026 was another transformative year for the company, with revenue surpassing $1.3 billion, more than tripling year over year. Non-GAAP net income increased more than fivefold to $662 million, reflecting strong execution, product leadership and healthy margins. In the fiscal fourth quarter, revenue reached a record $437 million, exceeding the company's entire fiscal 2025 revenue, while non-GAAP gross margin remained strong at 68.3%. Management attributed this performance to Credo's ability to capitalize on the increasing importance of reliable, power-efficient connectivity as AI clusters continue to expand.

The company continues to strengthen its competitive position through a comprehensive connectivity portfolio designed for AI infrastructure. Its strategy spans die-to-die, chip-to-chip, multi-rack copper and facility-wide optical interconnect solutions, enabling it to address connectivity needs across the entire AI data center. Management stated that hyperscalers and Neo cloud providers increasingly seek partners capable of delivering multiple generations of connectivity products with deep system-level integration. Credo believes its vertically integrated approach, covering SerDes technology, silicon, firmware, telemetry software and system-level solutions, differentiates it from competitors and positions it as a long-term network architecture partner.

Credo's Active Electrical Cable (AEC) business remains a major growth driver. As AI clusters become larger and more complex, customers are increasingly prioritizing network reliability and power efficiency. Management noted that its ZeroFlap AECs provide significantly higher reliability than conventional laser-based optical modules while consuming less power, making them well-suited for in-rack and multi-rack deployments. The company continues to experience strong adoption among hyperscale and Neo cloud customers for both 100-gig and emerging 200-gig-per-lane deployments. It also remains on track with its PCIe Gen 6 AEC family, where customer engagement and design activity continue to expand.

The optical business is expected to become another significant growth engine. Management believes fiscal 2027 will represent an inflection point as demand increases for optical DSPs, silicon photonics and ZeroFlap optics. The recently completed acquisition of Dust Photonics expands Credo's capabilities with silicon photonics technology, strengthening its portfolio across 800G and 1.6T solutions while providing a roadmap to higher-speed products. The company expects its optical DSPs, silicon photonics PICs and ZeroFlap optics to each generate more than $100 million in fiscal 2027 revenue, with the combined optical portfolio expected to contribute more than $600 million. Management believes this portfolio will support sustained long-term growth.

Beyond its core businesses, Credo continues to advance several emerging growth opportunities. The company is developing Active Light Cable (ALC) solutions that extend the reliability and power advantages of AECs into longer-distance optical connectivity using MicroLED technology. It is also expanding its OmniConnect portfolio, including its Weaver gearbox solution, to address increasing memory bandwidth and density requirements for next-generation AI inference architectures. Customer engagement remains strong, and management expects production ramps for both ALC and OmniConnect solutions to begin in fiscal 2028, adding new long-term growth drivers.

Image Source: Zacks Investment Research

The company's financial outlook remains bright, supported by continued AI-driven demand. For fiscal 2027, Credo expects revenue growth of more than 80% year over year, with the second half benefiting from the ramp of its optical portfolio. Management anticipates non-GAAP gross margin to remain broadly consistent with fiscal 2026 levels while maintaining a non-GAAP net margin near 50%. The company also generated record operating cash flow and free cash flow during the fiscal fourth quarter, ending the year with approximately $1.4 billion in cash and cash equivalents, providing ample financial flexibility to invest in future growth opportunities.

However, Credo continues to face customer concentration and supply chain-related risks. During the fourth quarter of 2026, four customers each accounted for more than 10% of revenue, with the largest customer contributing 34%, highlighting continued dependence on a limited number of large customers despite ongoing diversification efforts. Management also acknowledged that the supply chain remains tight across the industry and noted that current fiscal 2027 guidance is based on the existing tariff environment, which remains subject to change.

A Look at CRDO’s Valuation

The stock trades at a forward 12-month price-to-sales (P/S) ratio of 18.84, above the industry’s average of 9.04. AVGO, MRVL and ALAB trade at a forward 12-month P/S of 12.25X, 14.73X and 36.42X, respectively.

Image Source: Zacks Investment Research

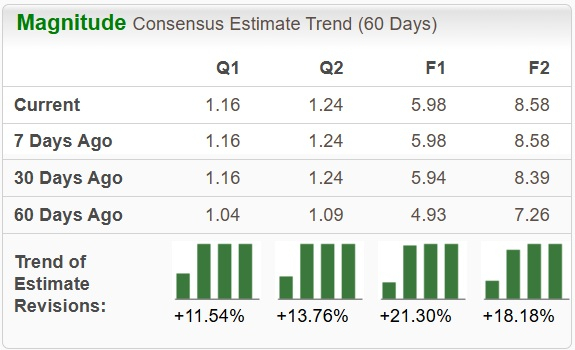

CRDO’s Upward Estimates

The Zacks Consensus Estimate for CRDO’s earnings for fiscal 2026 has been significantly revised upward over the past 60 days.

Image Source: Zacks Investment Research

What Should You Do With CRDO Stock Now?

Sporting a Zacks Rank #1 (Strong Buy), Credo appears to be a compelling investment opportunity at the moment.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).