Seagate's Massive 616% Run in a Year: Time to Buy, Sell, or Stay Put?

Seagate Technology Holdings plc’s STX stock has delivered solid gains, climbing 616.2% in the past year, exceeding the Zacks Computer-Integrated Systems industry’s, the Zacks Computer & Technology sector and the S&P 500’s growth of 154.1%, 61.9% and 39.2%, respectively.

Image Source: Zacks Investment Research

The company has also surpassed its industry peers like International Business Machines Corporation IBM and Advanced Micro Devices AMD, which have risen 5.3% and 218.7%, respectively, over the past year. At the same time, its primary competitor in the HDD space, Western Digital Corporation WDC, has surged 919.9%.

Western Digital is a diversified storage company offering a broad portfolio of HDD and NAND-based SSD solutions used across desktop PCs, servers, NAS devices, gaming consoles, DVRs and other consumer electronics. AMD delivers industry-leading total cost of ownership, efficiency and advanced AI capabilities, enabling high performance, reliability and scalability across data centers, the edge and end-user environments. IBM has gradually evolved into a provider of cloud and data platforms, offering advanced information technology solutions, computer systems, quantum computing and supercomputing solutions, enterprise software, storage systems and microelectronics.

A key driver behind Seagate’s surge is the AI infrastructure boom. As companies build massive data centers to train and run AI models, data creation is exploding, pushing cloud providers to seek cost-efficient storage at scale. Despite the hype around SSDs, high-capacity HDDs remain essential for large-scale storage, and Seagate, one of the dominant players in nearline HDDs, is well-positioned to benefit from this demand.

STX has a 52-week high of $553.57. After such a meteoric rise, the key question is whether Seagate still offers meaningful upside or if most of the gains are already reflected in its valuation. To answer that, it is important to look at the company’s recent performance, key growth drivers, potential risks and overall valuation to assess if the stock still merits a spot in investors’ portfolios.

AI Boom Fuels Rise in STX’s Data Storage Demand

At the center of Seagate’s surge is the AI infrastructure boom. As enterprises and hyperscalers race to build and scale AI models, data creation is growing at an unprecedented pace. Training large language models, running inference workloads and storing vast datasets all require enormous storage capacity. Seagate is a dominant player in nearline HDDs, the category specifically designed for cloud-scale data centers. As cloud providers prioritize cost per terabyte, Seagate’s high-capacity drives are seeing strong demand, making the company a key beneficiary of the AI-driven data explosion.

Seagate continues to benefit from a very strong demand environment, especially in data center markets. The shift to higher-capacity HAMR drives is expected to improve margins and cost efficiency, boosting its long-term value proposition. Its build-to-order pipeline also indicates that this strong demand momentum is likely to continue. Nearline capacity is fully allocated through calendar 2026, with orders for early 2027 expected to open shortly. Long-term agreements with major cloud customers provide increasing demand visibility through 2027, with early discussions already underway for 2028.

Seagate’s strength in areal density continues to be a key driver of its long-term growth and cost advantage over competing storage technologies. Its HAMR-based Mozaic platform enables higher-capacity drives, positioning it well to meet increasing AI-driven data storage demands. The company has experienced strong momentum in HAMR adoption, with more than 1.5 million units shipped and growing interest among major cloud service providers. Mozaic 3 is now certified with leading U.S. CSPs and is moving toward global adoption, while next-generation Mozaic 4 is advancing toward broader rollout. These developments support Seagate’s roadmap to significantly increase storage capacity per disk in the coming years.

Additionally, Seagate generates robust cash flow, allowing investments in innovation, acquisitions and growth, while continuing to reward shareholders through dividends and buybacks. In fiscal 2025, it reduced debt by $684 million, reflecting a balanced capital allocation strategy. For the second quarter of fiscal 2026, it returned $154 million via dividends and retired $500 million in debt. With expectations of higher free cash flow driven by strong demand, efficiency and disciplined spending, Seagate remains well-positioned to support its HAMR transition, sustain dividends and improve profitability.

Image Source: Zacks Investment Research

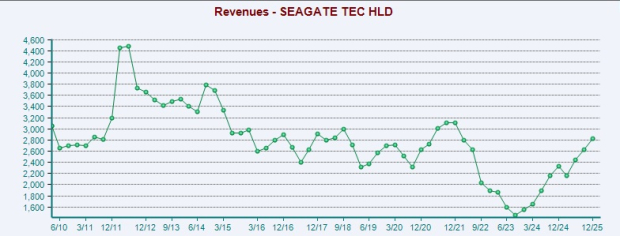

Demand remains strong, especially from global cloud customers, and is expected to more than offset the typical March-quarter seasonality in the edge IoT markets. For the fiscal third quarter, it expects revenues of $2.9 billion (+/- $100 million). At the midpoint, this indicates a 34% year-over-year improvement. It expects free cash flow to increase further in the March quarter, driven by strong demand, operational efficiency and disciplined capital spending, supporting sustainable long-term cash generation. STX will maintain capital discipline while continuing the transition and ramp-up of HAMR technology, with fiscal 2026 capital spending expected to remain within its target range of 4–6% of revenue.

STX’s Emerging Risks That Investors Should Be Wary Of

Seagate’s elevated debt levels remain a key risk for investors. As of Jan. 2, 2026, the company held about $1.05 billion in cash against roughly $4.5 billion in long-term debt, resulting in a debt-to-total capital ratio of 90.7%, well above the industry average of 36.8%. This leverage largely reflects its strategy of funding growth through acquisitions, partnerships and investments. While such spending supports expansion, heavy reliance on debt increases financial risk, especially if returns take time to materialize.

Despite strong cash flow generation, the high debt burden could limit Seagate’s flexibility in maintaining dividends, executing share buybacks, or pursuing future acquisitions.

A large portion of Seagate’s revenue comes from international markets, exposing it to currency fluctuations. Adverse movements in currencies such as the euro and pound against the U.S. dollar can weigh on its financial performance and slightly limit growth prospects. The company also operates in a highly competitive data storage market, facing pressure from both HDD and SSD manufacturers, as well as firms offering storage subsystems like electronic manufacturing services providers. Ongoing global macroeconomic uncertainty and supply chain volatility add further challenges to the competitive landscape.

Estimate Revision Trend for STX

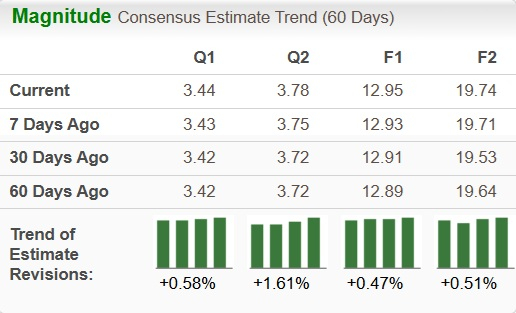

STX is currently witnessing an uptrend in estimate revisions. Earnings estimates for fiscal 2026 have increased 0.47% to $12.95 over the past 60 days, while the same for fiscal 2027 has gone up 0.51% to $19.74.

Image Source: Zacks Investment Research

STX’s Valuation: The Critical Piece

Going by the price/earnings ratio, the company’s shares currently trade at 30.43 forward earnings compared with 10.77 for the industry.

Image Source: Zacks Investment Research

In comparison, the forward 12-month price/earnings multiple for IBM, AMD and WDC are 20.07X, 40.55X and 29.27X, respectively.

Final Verdict

Seagate’s surge reflects a transformation driven by AI and data infrastructure demand. The company is well-positioned in a critical segment of the data infrastructure stack, and its role in enabling large-scale storage remains highly relevant.

The key issue now is not whether Seagate is a strong company but whether the current price already reflects most of its future growth. For investors, this is less about chasing momentum and more about carefully weighing long-term potential against near-term expectations. A hold stance appears to be the most balanced approach at this stage. Seagate’s fundamentals remain solid and industry tailwinds, particularly from AI-driven storage demand, are still intact. However, the stock’s sharp rally has stretched its valuation, which could limit near-term upside. Holding the stock lets investors stay positioned for potential long-term gains without making aggressive purchases at elevated levels.

STX currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).