Should You Add Intel Stock to Your Portfolio Ahead of Q1 Earnings?

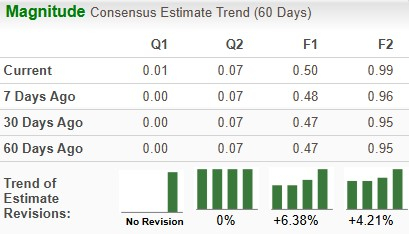

Intel CorporationINTC is scheduled to report first-quarter 2026 earnings after the closing bell on April 23. The Zacks Consensus Estimate for sales and earnings is pegged at $12.38 billion and a penny per share, respectively. Over the past 60 days, estimates for INTC have increased 6.38% to 50 cents per share for 2026, while it has increased 4.21% to 99 cents for 2027.

INTC Estimate Trend

Image Source: Zacks Investment Research

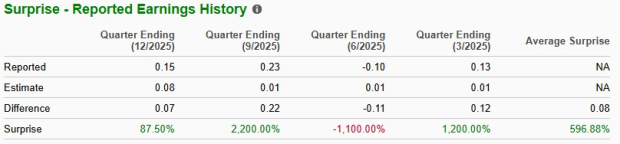

Earnings Surprise History

The leading semiconductor manufacturer delivered a stellar four-quarter earnings surprise of 596.88%, on average, beating estimates thrice. In the last reported quarter, the company’s earnings surprise was 87.5%.

Image Source: Zacks Investment Research

Earnings Whispers

Our proven model predicts a likely earnings beat for Intel for the first quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is exactly the case here. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Intel currently has an ESP of +425.00% with a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping the Quarterly Performance

During the quarter, Intel introduced the leading-edge Intel Core Ultra Series 3 processors. These are the first processors built on Intel 18A. This is a 1.8-nanometer-class chip manufacturing process engineered to deliver significantly higher performance and efficiency for AI and next-generation computing requirements. The company also rolled out its next-generation workstation CPUs, the Xeon 600 series. The leading-edge processor is purpose-built for professional environments where extreme computation requirements are present, and systems run heavy workloads for long durations. Such innovative product launches are expected to have a favorable impact on the first-quarter results.

In the quarter under review, Intel announced a multi-year strategic collaboration with SambaNova, a leading AI inference platform and hardware provider. The partnership is set to focus on delivering high-performance, cost-efficient AI inference solutions built around Intel Xeon-based infrastructure.

NVIDIA CorporationNVDA has opted to utilize Intel Xeon 6 processors for its NVIDIA DGX Rubin NVL8 systems, a high-performance, liquid-cooled AI server designed specifically for large-scale agentic AI and reasoning models. Intel also formed a collaboration with CrowdStrike, a leading AI-native cybersecurity company, to secure AI adoption across AI PCs. Such strategic collaboration with industry leaders will likely boost commercial prospects.

However, despite Intel’s growing prowess in the AI PC and AI inference domains. The company faces competition from other major players, including Advanced Micro DevicesAMD, Qualcomm and NVIDIA. The NVIDIA Blackwell, H200, L40S and NVIDIA RTX offer remarkable speed and efficiency in AI inference across cloud, workstations and data centers. AMD and Qualcomm are steadily expanding into the AI PC domain. This could impact Intel’s growth prospects.

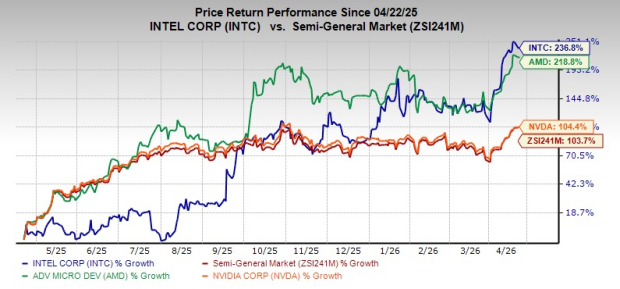

Price Performance

Over the past year, Intel has surged 236.8% compared with the industry’s growth of 103.7%, outperforming its peers, NVIDIA and AMD. While NVIDIA has gained 104.4%, AMD has soared 218.8% over this period.

Image Source: Zacks Investment Research

Key Valuation Metric

From a valuation standpoint, Intel appears to be relatively cheaper than the industry but above its mean. Going by the price/sales ratio, the company’s shares currently trade at 5.97 forward sales, lower than 11.24 for the industry but higher than the stock’s mean of 3.19.

Image Source: Zacks Investment Research

Investment Consideration

AI clusters require massive interconnect bandwidth. Consistent networking requirements in the AI buildouts are driving growth in Intel’s custom Application-Specific Integrated Circuit (ASIC) business. Intel’s Client Computing Group is benefiting from healthy traction in the AI pc market. Intel AI chips are now powering more than 200 notebook designs. The AI PC market is expected to grow substantially in the upcoming quarters, backed by rapid digital transformation initiatives across sectors. Intel’s leading-edge Core Ultra Series 3 processors are expected to gain from this.

Innovative product launches and AI integration are expanding Intel's customer base. Super Micro Computer, a global leader in high-performance, energy-efficient IT solutions, has opted to deploy Intel’s Xeon 6 Processors. Intel has also revealed that several industry leaders across industries, including AT&T, Verizon, Samsung, and Ericsson, are leveraging Xeon 6 for network transformation and AI acceleration.

However, weakness in Intel’s Foundry business remained a drag on the top-line growth. Intel’s 18A ramp costs worsen the segment’s operating margin. China accounts for the lion’s share of Intel’s total revenues. China's purported move to replace U.S.-made chips with domestic alternatives significantly affected its revenue prospects. Intel’s high debt levels might limit sufficient cash flow generation.

End Note

Strength in the AI PC market and the AI data center market are major growth drivers for Intel. Strategic collaboration with major industry leaders such as NVIDIA and Crowdstrike to expand portfolio offerings and accelerate innovation is a positive. A growing client base is a tailwind. Upward estimate revision shows growing investors’ confidence. However, stiff competition in the commercial PC market is hindering growth. High debt levels are a concern. With a Zacks Rank #3, Intel appears to be treading in the middle of the road, and new investors could be better off if they trade with caution.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).