Key Points

The Nasdaq Composite index briefly entered correction territory during the past month as investors rotated away from artificial intelligence (AI) stocks.

The selling activity indiscriminately eroded the valuations of otherwise robust, profitable technology businesses.

Microsoft, Amazon, and Alphabet trade at attractive levels now, considering their long-term AI-driven trajectories.

Throughout 2026, there has been a pronounced shift on Wall Street away from technology stocks. The combination of waning enthusiasm for the artificial intelligence (AI) narrative and big tech's accelerating capital spending on infrastructure build-outs has paved the way for the "Great Rotation" -- a broad shift in investor preference away from AI stocks and toward value stocks and companies that produce tangible, physical goods.

The sell-offs that this transition induced have left Microsoft(NASDAQ: MSFT), Amazon(NASDAQ: AMZN), and Alphabet(NASDAQ: GOOGL)(NASDAQ: GOOG) trading at discounts.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Far more than cloud infrastructure providers, each of these companies is weaving AI into durable, multiproduct ecosystems spanning enterprise software, consumer experiences, logistics, advertising, and even orbital infrastructure. These trillion-dollar giants aren't just renting AI compute. They are quietly designing and owning the entire AI flywheel.

Microsoft brings native intelligence to the workspace

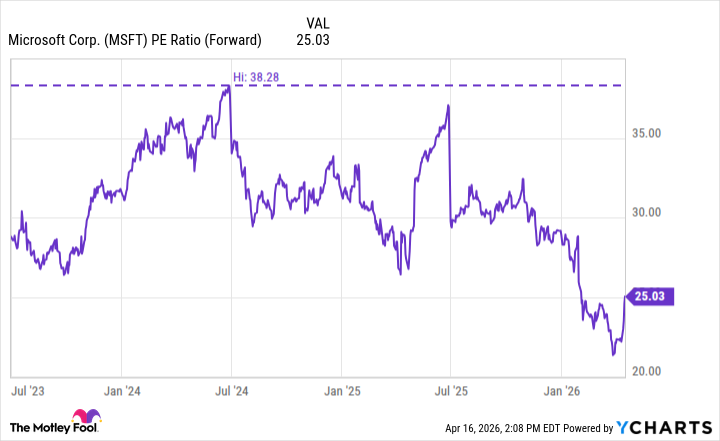

Microsoft's valuation tells quite the bargain story. Its forward price-to-earnings (P/E) ratio of 21 is a 45% discount to its 2024 peak multiple, even as revenues from its Azure cloud services segment have been growing by nearly 40% year over year in recent quarters. The market is pricing Microsoft like a mature technology dinosaur and ignoring the AI software that's driving the company's various revenue streams.

MSFT PE Ratio (Forward) data by YCharts.

Beyond Azure, Microsoft has built an end-to-end enterprise AI operating system thanks to its multibillion-dollar partnership with OpenAI. OpenAI's models are embedded directly into Microsoft Copilot for Microsoft 365. This transition brought much-needed innovation to legacy product lines like Excel, PowerPoint, Teams meetings, and Outlook -- each of which now features AI-native functionality.

At the enterprise level, GitHub Copilot is being used to write new code at Fortune 500 companies, while Dynamics 365 Copilot is helping automate critical applications like sales pipelines and supply chain forecasting in real time. On the consumer side, the company's Surface devices now ship with dedicated neural processing units. Meanwhile, Microsoft's custom Maia accelerator chips are being deployed across its data centers in an effort to slash inference costs relative to fully relying on off-the-shelf GPUs.

This vertical integration -- from silicon to software -- is meant to create a competitive moat for its offerings. Even amid a stock market rotation that has punished pure-play AI hype, Microsoft's diversified cash flows from cloud infrastructure, personal computing, gaming, LinkedIn, and security are acting as foundations while its AI ecosystem quietly compounds.

Image source: Getty Images.

Amazon is moving from the warehouse to the final frontier

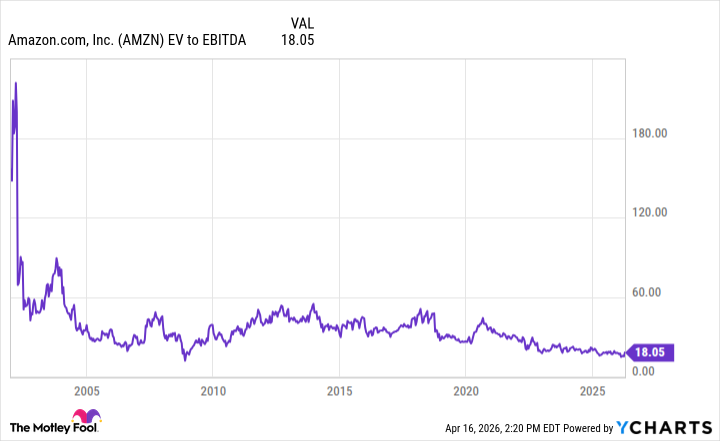

Amazon's ratio of enterprise value to earnings before interest, taxes, depreciation, and amortization (EBITDA) is roughly 18 -- the lowest it has ever been.

AMZN EV to EBITDA data by YCharts.

The company's cloud segment, Amazon Web Services (AWS), remains the foundation supporting the overall business. New AI-powered products like Bedrock, which are designed in partnership with Anthropic, now serve as central marketplaces for enterprise customers to access foundational models.

Another differentiator is how Amazon is bringing AI to the physical world. Its custom Proteus autonomous mobile robots and Sparrow robotic arms can pick, stow, and sort packages faster than human workers.

Furthermore, Amazon's recent acquisition of Globalstar expands Project Kuiper -- giving the company direct control over latency for AWS edge computing. This was a savvy form of capital allocation, as efficiencies from this deal should drive improvements for next-generation services featuring real-time robotics and drone delivery.

On top of all of this, Amazon's conversational AI assistant, Rufus, is helping personalize product recommendations for customers across the company's roughly $500 billion retail marketplace.

Alphabet is much more than an advertising empire

On the surface, Alphabet stock looks expensive within this trio. The company's forward price-to-earnings ratio of 29 is only nominally discounted to the highs it touched in late 2025 and well above the company's two-year average of roughly 21. Alphabet's valuation expansion over the last year has contributed to this premium.

That said, there are more nuanced ways to analyze the company -- specifically, by looking at its trailing-12-month PEG ratio, which is 0.91. Any positive figure for that metric below 1.0 is generally viewed as signaling that a stock is undervalued, so that ratio suggests that Alphabet is trading at a reasonable price relative to its earnings growth momentum.

While some still view Alphabet as an advertising company with a cloud computing side hustle, these investors are missing the tailwinds of Alphabet's AI stack and optionality.

Alphabet is powering much of its expanding data center infrastructure with the custom TPU chips it designed in partnership with Broadcom. Accessing TPUs has become a lucrative value proposition for other hyperscalers, which is why they're renting capacity from Alphabet.

Meanwhile, another hidden catalyst is Alphabet's long-held stake in SpaceX. As SpaceX moves toward an initial public offering, Alphabet could be positioned to realize nearly $140 billion in profit while simultaneously gaining first-mover access to a major low-latency satellite network.

This relationship could become the backbone for global AI inference at the edge, especially for Waymo's autonomous fleet as well as Google Cloud's sovereign regions. It appears that Alphabet is poised to turn what was once a widely overlooked financial stake in a privately held space business into front-of-the-line access to strategic orbital infrastructure that most other competitors will have to lease at increasing market rates.

Big tech stocks are dirt cheap and make for compelling buy-and-hold positions

The Great Rotation has created a rare window that only smart investors are seeing through. Prolonged and indiscriminate panic-driven selling has left Microsoft, Amazon, and Alphabet shares cheap. While their respective valuation profiles reflect investors' skepticism about how long it will take for their massive investments in AI to pay off, each company has already proven product-market fit across software, logistics, search, advertising, and physical infrastructure.

History suggests that the current rotation will eventually reverse again. When it does, it will be the companies that have developed AI ecosystems that are not just durable, but defensible for the next decade, that generate robust long-term returns.

Should you buy stock in Microsoft right now?

Before you buy stock in Microsoft, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Microsoft wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $511,411!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,238,736!*

Now, it’s worth noting Stock Advisor’s total average return is 986% — a market-crushing outperformance compared to 199% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of April 21, 2026.

Adam Spatacco has positions in Alphabet, Amazon, and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Broadcom, and Microsoft. The Motley Fool has a disclosure policy.