Bear of the Day: Autohome (ATHM)

Finding stocks to avoid can be just as important as identifying the next big winner. While many investors focus exclusively on companies with strong momentum and improving fundamentals, it can be equally valuable to recognize businesses facing structural challenges. Companies with declining revenue trends, falling earnings estimates, and persistent share price weakness often struggle to attract investor capital for extended periods.

One stock that currently fits this profile is Autohome (ATHM). The company has seen its fundamentals deteriorate in recent years, and the combination of slowing growth, falling analyst estimates, and a steep decline in the stock price suggests investors may want to remain cautious.

Image Source: Zacks Investment Research

Autohome’s Business Model

Autohome operates one of China’s largest online platforms for automotive consumers. The company provides digital content, research tools, dealer listings, and advertising services that connect car buyers with automakers and dealerships. Historically, the platform generated strong growth by monetizing advertising and marketing services from automotive manufacturers and dealers seeking access to its large user base.

However, the company’s fortunes are closely tied to trends within China’s automotive market. As competition among online auto marketplaces intensified and growth across the Chinese auto sector slowed, Autohome’s revenue trajectory has weakened considerably.

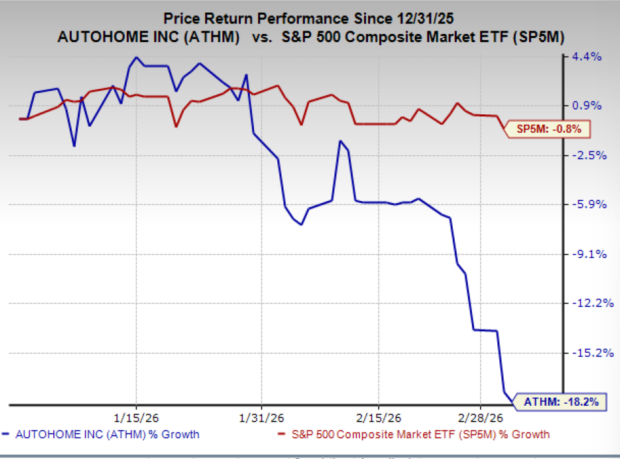

ATHM Stock Falls Along Sales Growth and Earnings Estimates

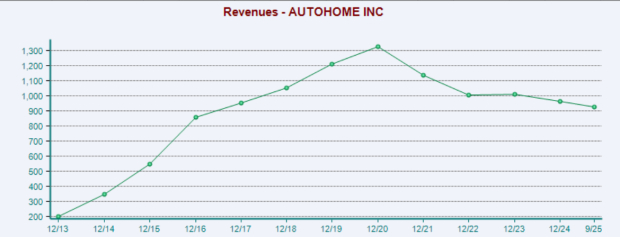

Autohome’s financial performance has steadily deteriorated over the past several years. After reaching a peak in 2020, annual revenue has trended lower, with total sales declining roughly 30% from their peak. The slowdown reflects weaker demand from automakers and dealers, as well as increased competition from other online platforms.

Analysts have also been lowering their earnings expectations. Over the past several months, consensus earnings estimates have been revised downward, a negative signal that often precedes further stock price weakness. As a result, the stock currently carries a Zacks Rank #5 (Strong Sell) rating.

The market has already reacted to these challenges. Shares of ATHM have fallen more than 80% from their 2021 highs, reflecting investor concerns about the company’s long-term growth prospects.

Image Source: Zacks Investment Research

Should Investors Avoid ATHM Stock?

Autohome currently appears to be a company facing structural headwinds rather than a temporary slowdown. Declining revenue, negative earnings revisions, and persistent share price weakness all point to a business that is struggling to regain momentum.

While turnarounds are always possible, there is currently little evidence that Autohome’s growth trajectory is improving. Until the company demonstrates a clear stabilization in revenue and earnings expectations, investors may be better served focusing on companies with stronger fundamental momentum.

For now, Autohomelooks like a stock investors may want to avoid.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power, you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Autohome Inc. (ATHM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).