Key Points

ASML is benefiting from the growing investments in artificial intelligence (AI).

Its order volumes support years of accelerated demand.

ASML's stock isn't cheap by any means.

The S&P 500(SNPINDEX: ^GSPC) fell by 4.6% in the first three months of 2026, and had dipped by more than 9% from its peak late in that period. Yet a little over two weeks into April, the S&P 500 hasn't just made up those losses, it's setting new all-time highs again.

Here's why semiconductor equipment manufacturer ASML(NASDAQ: ASML) is a top growth stock to buy now.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

ASML continues to lead the pack

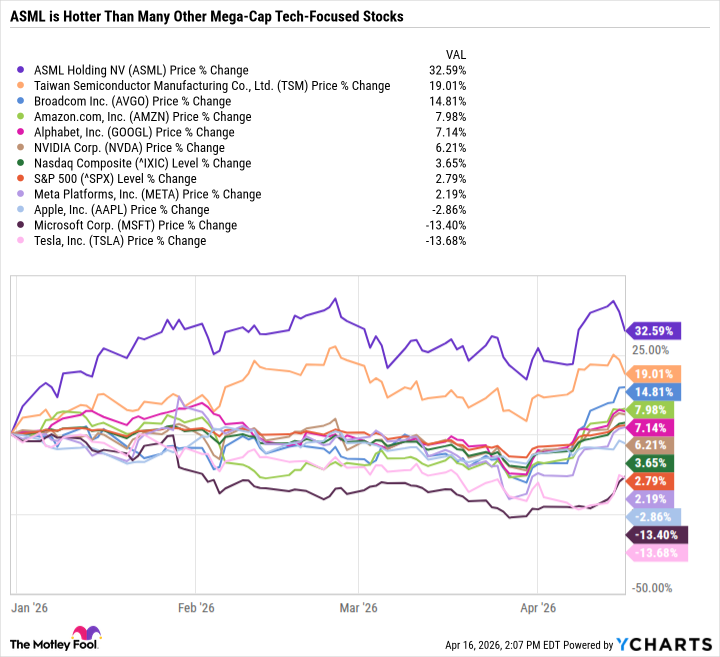

ASML crushed both the S&P 500 and the tech sector in 2025. So far this year, it has followed up that incredible performance with a 32.6% gain, outpacing semiconductor manufacturing giant Taiwan Semiconductor Manufacturing, Broadcom, every "Magnificent Seven" stock, and the major indexes.

ASML and the broader semiconductor industry are on the rise because demand for artificial intelligence (AI) chips continues to outpace what fabrication plants can currently produce -- creating multiyear backlogs.

Investors are becoming increasingly convinced that the spike in AI chip demand won't be a short-lived phenomenon, but rather a trend with staying power. A permanent increase in demand, even with ebbs and flows driven by spending cycles, would be incredible news for ASML given its unique role in the value chain.

The bedrock of AI evolution

ASML is a catch-all way to invest in AI because it benefits from data center spending regardless of which hyperscaler is operating the data center, what AI chips and networking infrastructure go into the data center, who is powering it, or what specialized machinery is in it.

This is because ASML has a virtual monopoly on high-end semiconductor lithography equipment. These massive and expensive machines are basically highly advanced printers that print tiny transistors and wires into computer chips. The most advanced ones bounce light off multilayered mirrors inside a vacuum chamber, enabling interconnected layering on microchips. ASML spent many years and billions of euros figuring out how to do this at higher resolutions and transistor densities than any rival has yet been able to achieve. Put simply, today's most advanced chips depend on a highly advanced manufacturing process that wouldn't be possible without ASML's systems.

ASML's ideal operating environment

It is music to ASML's ears that companies are racing to design and build their own custom chips to reduce their dependence on Nvidia's graphics processing units. ASML loves it when Advanced Micro Devices and Broadcom challenge Nvidia's market leadership. Tesla entered a partnership with Intel to build a fab in Texas for advanced AI chips for data centers, robotics, and vehicles. The U.S. build-out of chip fabs will be yet another long-term catalyst for ASML, as it could reduce the equipment maker's reliance on customers such as Taiwan Semiconductor and Samsung Electronics.

In sum, ASML benefits from innovation and competition in the chip space. Shifts in market share dynamics create greater scarcity for its most advanced lithography machines, which support its pricing power and extend its backlog.

A stock that's worth its premium price tag

ASML trades at 39.5 times forward earnings, and there are plenty of tech stocks changing hands at less expensive valuations. But the investment thesis for the company is stronger than ever, and its multiyear backlog should support sustained high-margin growth.

To justify that elevated valuation, it will need to continue growing its earnings at a pace that matches investors' ambitious expectations. The stock fell after ASML reported its first-quarter results on April 15. The results were incredible, and management even raised its guidance. But investors' hopes had been even higher.

Although ASML is red-hot, it could be volatile depending on shifts in investor sentiment. So the stock is best suited for investors with a high risk tolerance and who believe that the AI infrastructure investment trend is here to stay.

Should you buy stock in ASML right now?

Before you buy stock in ASML, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ASML wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $524,786!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,236,406!*

Now, it’s worth noting Stock Advisor’s total average return is 994% — a market-crushing outperformance compared to 199% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of April 21, 2026.

Daniel Foelber has positions in ASML and Nvidia. The Motley Fool has positions in and recommends ASML, Advanced Micro Devices, Alphabet, Amazon, Apple, Broadcom, Intel, Meta Platforms, Microsoft, Nvidia, Taiwan Semiconductor Manufacturing, and Tesla and is short shares of Apple. The Motley Fool has a disclosure policy.