Should Investors Buy Credo Technology Stock Post Q3 Earnings?

Credo Technology Group Holding LtdCRDO reported strong third-quarter fiscal 2026 results earlier this week.

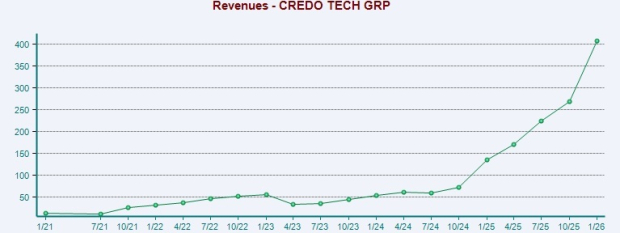

Revenues for the fiscal third quarter jumped 51.9% sequentially and 201.5% year over year to $407 million. This performance highlights the strong demand for the company’s high-speed connectivity solutions.

Image Source: Zacks Investment Research

Revenues more than doubled from fiscal 2024 to fiscal 2025, and the company expects the metric to triple from fiscal 2025 to fiscal 2026. This implies that Credo will have achieved more than six times the revenue growth within two years. For fiscal 2027, management expects more than 50% year-over-year revenue growth, indicating a strong demand environment.

Non-GAAP gross margin was 68.6% compared with 63.8% a year ago. Non-GAAP net income hit $208.8 million, representing a 51.3% net margin. Free cash flow totaled $139.7 million in the fiscal third quarter and the company had $1.3 billion in cash and equivalents.

Post the announcement on March 3, the stock fell sharply 14.8% and closed trading at $97.30. However, the stock is up 17.9% since March 3 and closed yesterday’s trading session at $114.74.

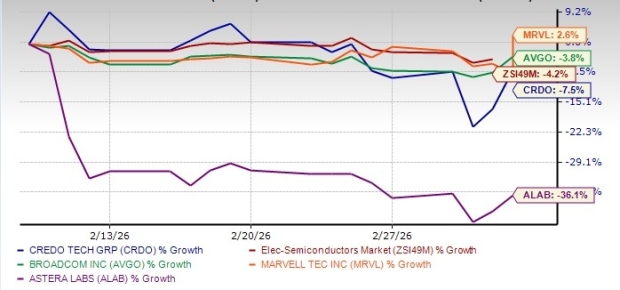

Price Performance

Image Source: Zacks Investment Research

Over the past month, CRDO has lost 7.5%, igniting investor concern regarding volatility in AI-driven semiconductor plays. Overall, the Electronic-Semiconductors industry is down 4.2% over the same time frame.

This slide is bound to raise the obvious question: Is this the beginning of a deeper structural problem, or simply a pause in an otherwise compelling long-term growth story?

Let’s dig deeper and assess if this pullback represents a buying opportunity.

AI Proliferation Driving Long-Term Connectivity Demand

CRDO’s focus on high-performance, energy-efficient connectivity solutions gives it strategic relevance as hyperscalers and cloud service providers overhaul their network architectures.

Management highlighted that the industry is transitioning from 100-gigabit-per-lane connectivity to 200-gigabit-per-lane solutions, with 400-gigabit-per-lane technologies expected in the future. As AI clusters scale into the hundreds of thousands of GPUs and push toward million-GPU configurations, reliability, signal integrity, latency and power efficiency, total cost of ownership have become “mission-critical”. Credo’s architecture (purpose-built SerDes technology, sound IC design and a system-level development approach) is tailored to meet these demands.

CRDO’s AECs and IC Portfolio Witnessing Heavy Demand

CRDO’s Active Electrical Cables (AECs) business sits at the core of its growth narrative, playing an increasingly critical role in AI-driven networking deployments. According to Credo, adoption of zero-flap AECs is accelerating because they deliver up to 1,000x higher reliability while consuming roughly 50% less power compared with optical alternatives. These advantages are particularly valuable in large XPU clusters, where network failures can disrupt operations and lead to high costs.

Credo’s hyperscaler traction sits at the center of its AEC strength. The company reported “substantial year-over-year growth” across four domestic hyperscalers. Three hyperscalers each contributed more than 10% of total revenues, reflecting strong adoption of Credo’s high-reliability AEC solutions. Credo has also secured a fifth hyperscaler customer, further strengthening its position within the global cloud ecosystem.

Management added that the industry was still in the early stages of AEC adoption, implying a long runway for growth as AI infrastructure deployments accelerate. Beyond traditional hyperscalers, Credo is also seeing increasing demand from Neocloud providers.

Beyond AECs, Credo is focusing on its IC portfolio, which includes retimers and optical DSPs. Credo’s PCIe retimer program remains on track for design wins in fiscal 2026 and revenue contributions in the next fiscal year.

With the recent launch of the Blue Heron 224G AI scale-up retimer, it is eyeing the lucrative scale-up networking market. The Blue Heron retimer is purpose-built to support multiple protocols, including UALink, ESUN and Ethernet and enables full recovery of a 40+dB 224G link. Blue Heron enables rack-scale cable backplanes and flexible placement of switch ICs and GPUs for AI scale-up applications.

Image Source: Zacks Investment Research

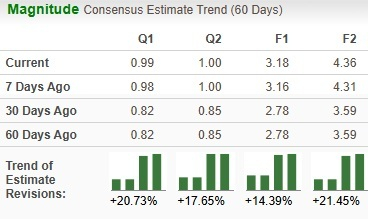

Analysts have revised their earnings estimates upwards over the past 60 days.

Expanding Product Portfolio Unlocks New Opportunities

Apart from the AECs and IC portfolio, CRDO is also expanding its long-term growth potential by introducing three new product families that broaden the total addressable market. These include Zero-Flap optics, Active Linear Cables (ALCs) and OmniConnect gearboxes.

ZF optics is a laser-based connectivity solution delivering AEC-level reliability through a custom optical DSP tightly integrated with Credo’s software stack. The company has commenced production shipments to its first Neocloud customer, TensorWay, and is currently in qualification with three additional customers, including hyperscalers. Management expects a considerable production ramp beginning in the first quarter of fiscal 2027.

ALCs utilize micro-LEDs, delivering AEC-level reliability and power efficiency and support up to 30-meter connections for row-scale data center networks. Management expects to sample and qualify ALC products in fiscal 2027, with a production ramp anticipated in fiscal 2028.

OmniConnect gearboxes are designed to optimize XPU connectivity. The first OmniConnect product, called Weaver, allows up to a tenfold improvement in memory I/O density. Management expects the initial production ramp for OmniConnect gearbox in fiscal 2028, with additional products planned in the future.

Financial Firepower to Cushion Expansion

Credo’s $1.3 billion strong cash position enables it to pursue strategic M&A while continuing investments in product innovation. As AI infrastructure rapidly scales, the company’s combination of organic execution and targeted inorganic expansion could help deepen its technology moat and broaden the addressable market amid increasing competitive pressure.

The company recently acquired high-speed connectivity IP innovator CoMira Solutions. The acquisition strengthens Credo’s existing scale-out products, such as ZF, AECs, ZF Optics and ALCs, as well as OmniConnect solutions through innovative connectivity products like link layer, error correction (“ECC”) and security semiconductor IP. The CoMira acquisition builds on Credo’s earlier Hyperlume acquisition, announced in October 2025.

However, macroeconomic uncertainties, rising expenses and exposure to the AI investment cycle amid increasing market competition from the likes of BroadcomAVGO, Marvell TechnologyMRVL and Astera LabsALAB may impact CRDO’s growth trajectory.

Non-GAAP operating expenses are expected to be between $76 million and $80 million in the fiscal fourth quarter. This could pressure margins if revenue growth falters.

CRDO’s Premium Valuation Justified?

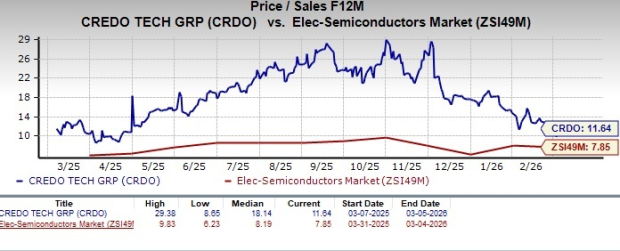

In terms of the forward 12-month price/sales ratio, CRDO is trading at 11.64, higher than the Electronic-Semiconductors sector’s multiple of 7.85.

Image Source: Zacks Investment Research

However, the premium appears justified given the company’s explosive revenue growth, strong profitability and expanding hyperscaler relationships and growing exposure to the rapidly scaling AI data center market.

In comparison, Broadcom trades at a forward 12-month P/S multiple of 14.58, while Astera Labs and Marvell are trading at a multiple of 14.47 and 6.42, respectively.

ALAB and AVGO have registered declines of 36.1% and 3.8%, respectively, while MRVL is up 2.6% in the past month.

Why Is CRDO Still a Buy?

CRDO currently sports a Zacks Rank #1 (Strong Buy).

The company remains well-positioned to benefit from AI-driven demand for networking, supported by expanding profitability, a strong balance sheet and a broadening product pipeline. While risks around competition, customer concentration and valuation persist, the long-term growth story seems compelling.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Marvell Technology, Inc. (MRVL): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

Credo Technology Group Holding Ltd. (CRDO): Free Stock Analysis Report

Astera Labs, Inc. (ALAB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).