Microsoft's AI Data Center Push: Growth Engine or Capex Trap?

Microsoft MSFT continues to double down on AI infrastructure, most recently announcing its intent to purchase approximately 3,200 acres of land in Cheyenne, Wyoming, to develop a new data center campus. The move signals that the company's capital deployment is accelerating well into fiscal 2026, further expanding an already formidable infrastructure footprint.

The scale of that commitment was on full display in the company's second-quarter fiscal 2026 results. Capital expenditures reached $37.5 billion for the quarter, with roughly two-thirds directed toward short-lived assets, primarily GPUs and CPUs. That brought the first-half fiscal 2026 total to $72.4 billion — a pace that puts the full-year figure on track to exceed $100 billion. The investment isn't without results: Microsoft Cloud revenues crossed $51.5 billion in the quarter, up 26%, while Intelligent Cloud revenues grew 29% to $32.9 billion, and Azure expanded 39% in constant currency.

The central investor tension is whether this spending pace will yield proportional returns. Management acknowledged that customer demand continues to exceed available supply, and that capacity constraints are expected to persist through at least the end of fiscal 2026. Crucially, the supply gap isn't a demand problem — it reflects infrastructure delivery timelines. Microsoft added nearly one gigawatt of capacity in the quarter alone, while its commercial remaining performance obligation reached $625 billion, up 110% year over year.

The structural case for the spending holds. Cash flow from operations came in at $35.8 billion in the fiscal second quarter, up 60%, driven by strong cloud billings and collections — evidence that the business is generating the liquidity to sustain its infrastructure cycle. Looking ahead, management guided for fiscal third-quarter capex to decrease on a sequential basis, with the mix of short-lived assets remaining similar, suggesting a more calibrated build rather than an open-ended spending surge. For MSFT, the data center push looks less like a trap and more like a deliberate bet on a demand curve that is only beginning to steepen.

Competitive Landscape

Microsoft's AI infrastructure push places it squarely alongside rivals AmazonAMZN and AlibabaBABA in a global capex arms race. Amazon has committed to $200 billion in capital expenditures for 2026, with the majority directed toward Amazon Web Services data centers — a figure that positions Amazon as the highest spender in the group. Alibaba, meanwhile, is considering raising its three-year AI infrastructure commitment to approximately $69 billion, up from a previously pledged $52.4 billion, with Alibaba Cloud prioritizing both domestic and international data center expansion. While Amazon and Alibaba each face their own supply-demand dynamics and regulatory environments, all three companies share the same foundational challenge: converting rising capital intensity into durable cloud revenue growth.

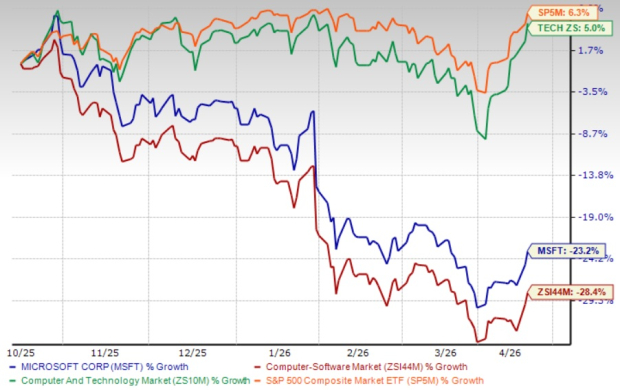

MSFT’s Share Price Performance, Valuation & Estimates

MSFT shares have lost 23.2% in the past six-month period, underperforming the Zacks Computer – Software industry’s decline of 28.4% and the Zacks Computer and Technology sector's return of 5%.

MSFT’s 6-Month Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, MSFT stock is currently trading at a forward 12-month Price/Sales ratio of 8.01X compared with the industry’s 6.69X. MSFT has a Value Score of D.

MSFT’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for MSFT’s fiscal 2026 earnings is pegged at $17.10 per share. The estimate indicates 25.37% year-over-year growth.

Microsoft Corporation Price and Consensus

Microsoft Corporation price-consensus-chart | Microsoft Corporation Quote

Microsoft currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>This article originally published on Zacks Investment Research (zacks.com).