Why Membership Trends Make BJ's Wholesale a Retail Stock to Watch

BJ's Wholesale Club Holdings, Inc.BJ is solidifying its position as a compelling retail stock to watch, supported by record-breaking membership metrics. The company generated $132.4 million in membership fee income in the first quarter of fiscal 2026, up 9.9% from the prior year, as total members reached an all-time high. Management attributed the gain to acquisition, retention and higher-tier membership penetration across both new and existing clubs.

The membership base is expanding and becoming more valuable. Management said higher-tier members are more engaged, shop more often and deliver greater lifetime value. The company maintained a 90% tenured membership renewal rate and reported more than 8 million members, with 42% higher-tier penetration.

This strong membership foundation also underpins steady customer traffic and ongoing market share gains. This was evident as BJ’s expanded operations in Texas, its 22nd state. In May 2026, BJ indicated that membership acquisition across the four new Texas clubs was running an impressive 33% ahead of plan, amassing approximately 100,000 members in the Dallas-Fort Worth region alone.

BJ's noted that membership fee income has grown every year for more than 25 years. The metric has expanded at an 8% CAGR from fiscal 1997 through fiscal 2025. That kind of consistency gives the latest quarter more weight, especially in a retail environment where consumer spending remains uneven. Management did caution that membership fee income growth should moderate as the company laps last year's fee increase. However, the underlying health of this engine remains exceptionally strong.

The committed shoppers provide BJ’s with a recurring membership-fee stream. The reliable, high-margin revenues generated by these loyal members give the warehouse club operator a distinct competitive advantage and substantial financial durability during dynamic economic periods.

Walmart & Costco: Membership Momentum Remains Strong

Walmart Inc.WMT continues to deepen engagement through Walmart+, with membership fee revenues rising 17.4% globally in the first quarter of fiscal 2027 and Walmart+ recording a record level of net additions. Management noted that membership has become an increasingly important profit stream, with members spending significantly more than non-members and utilizing benefits such as fuel savings and faster delivery.

Costco Wholesale Corporation’s COST membership model appears to be gaining strength not simply through member additions, but through deeper engagement. Costco’s membership fee income increased 10.7% year over year to $1,373 million during the third quarter of fiscal 2026. Executive members reached 41.2 million at quarter-end, up 9.6% from the prior year, far outpacing overall paid membership growth of 4.1%. With executive members representing 75% of sales and early adoption strong in China, Costco continues to benefit from loyalty and higher-tier penetration.

What the Latest Metrics Say About BJ's Wholesale

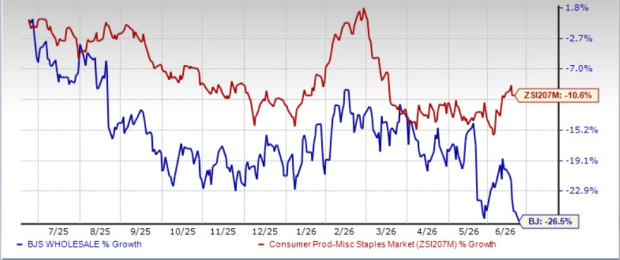

BJ's Wholesale has seen its shares tumble 26.5% over the past year compared with the industry’s decline of 10.6%.

Image Source: Zacks Investment Research

From a valuation standpoint, BJ's forward 12-month price-to-earnings ratio stands at 17.99, lower than the industry’s ratio of 18.13 and the median level of 20.57. BJ carries a Value Score of B.

Image Source: Zacks Investment Research

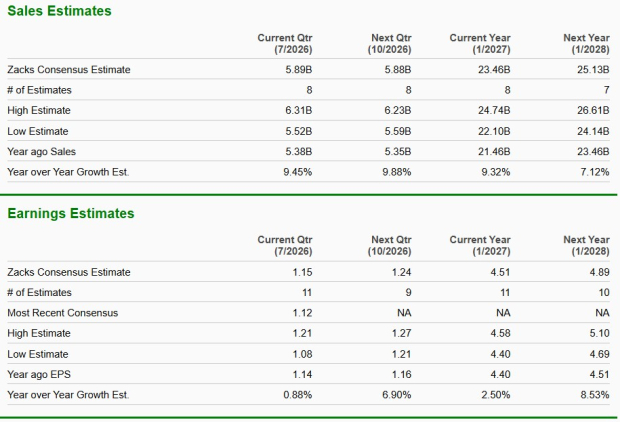

The Zacks Consensus Estimate for BJ’s current financial-year sales and earnings per share implies year-over-year growth of 9.3% and 2.5%, respectively. For the next fiscal year, the consensus estimate indicates a 7.1% rise in sales and 8.5% growth in earnings.

Image Source: Zacks Investment Research

BJ currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).