BJ's (BJ): Buy, Sell, or Hold Post Q1 Earnings?

Since January 2026, BJ's has been in a holding pattern, posting a small loss of 4.7% while floating around $88.75. The stock also fell short of the S&P 500’s 8.4% gain during that period.

Is now the time to buy BJ's, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is BJ's Not Exciting?

We’re swiping left on BJ's for now. Here are three reasons you should be careful with BJ, plus one stock we’d rather own.

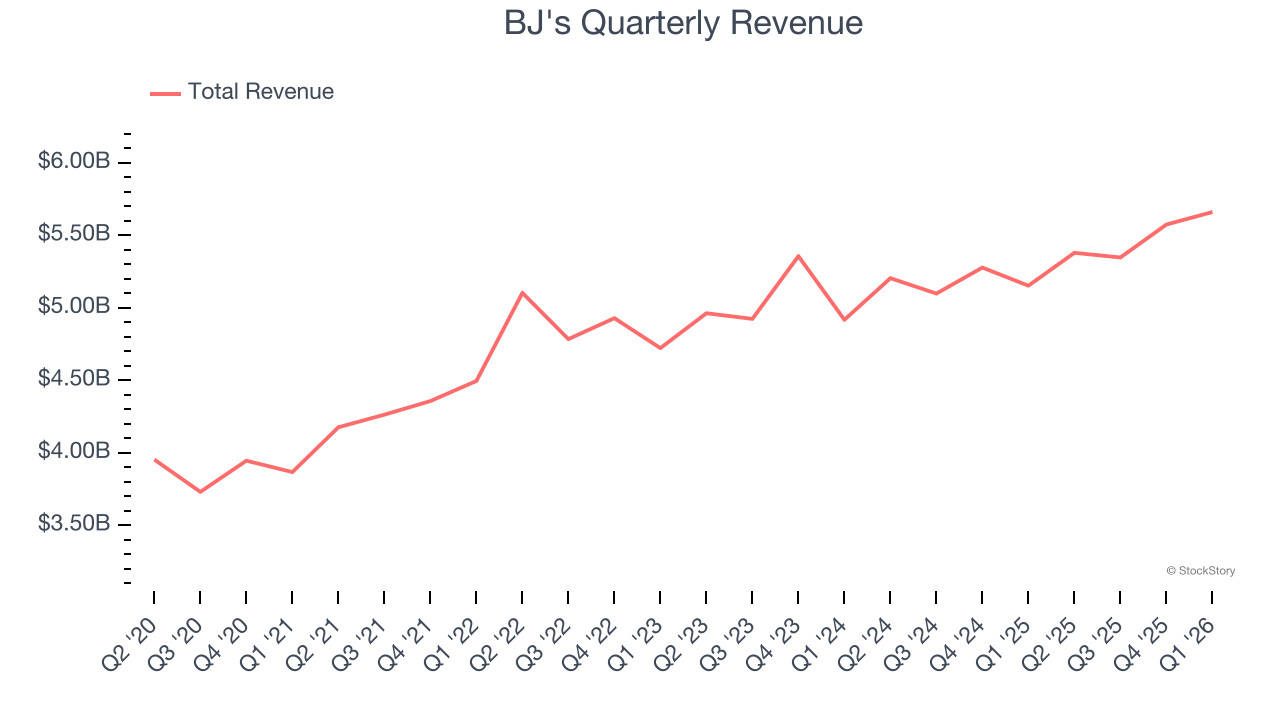

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, BJ’s sales grew at a sluggish 4% compounded annual growth rate over the last three years. This was below our standard for the consumer retail sector.

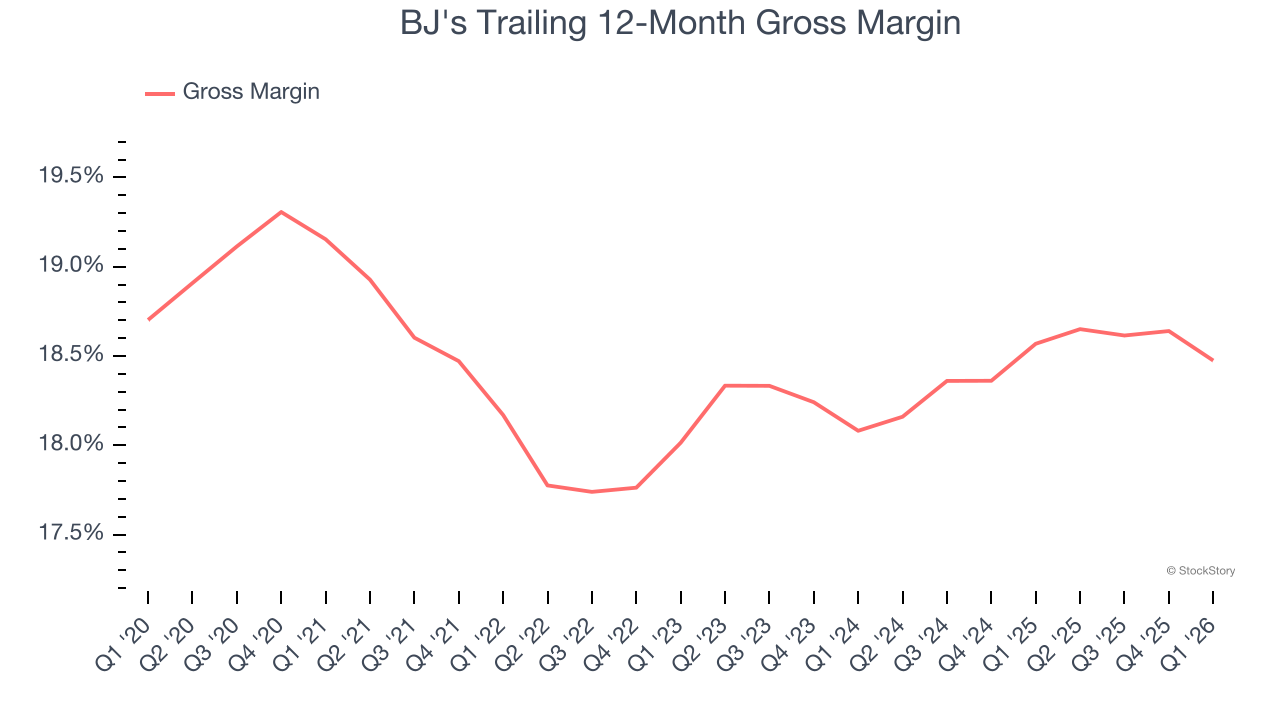

2. Low Gross Margin Reveals Weak Structural Profitability

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

BJ's has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 18.5% gross margin over the last two years. That means BJ's paid its suppliers a lot of money ($81.48 for every $100 in revenue) to run its business.

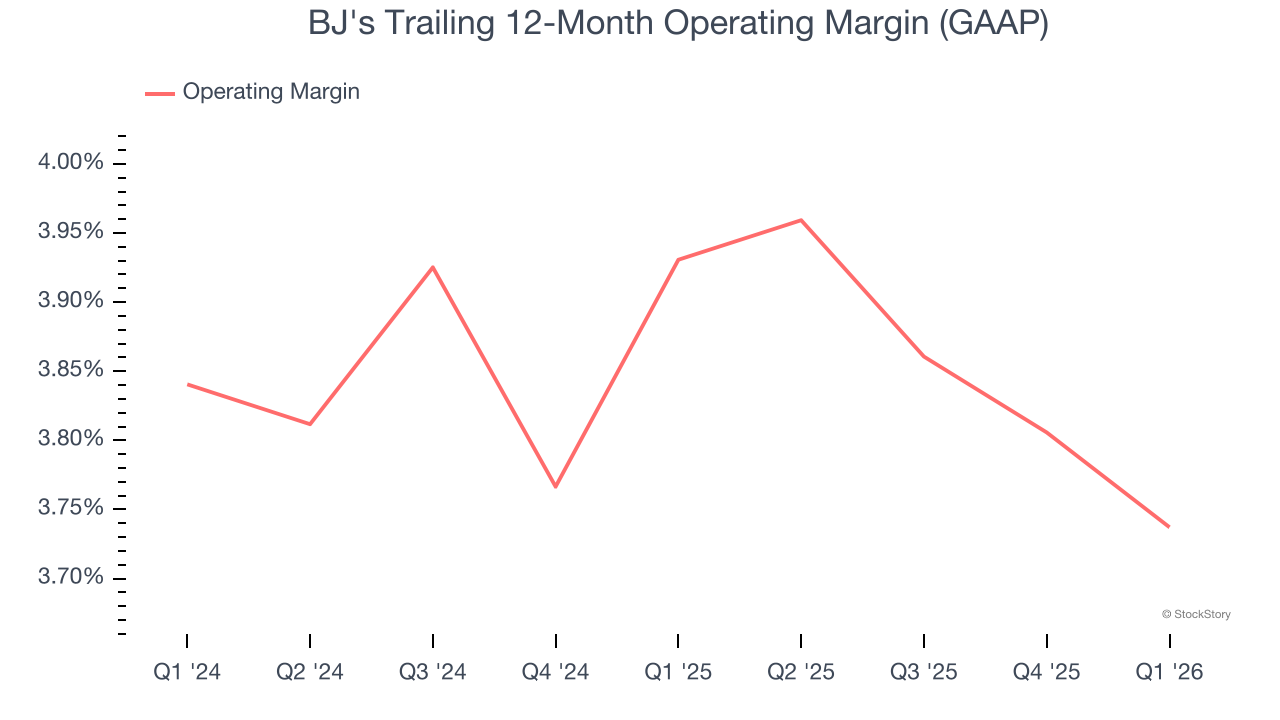

3. Weak Operating Margin Could Cause Trouble

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

BJ’s operating margin has more or less stayed the same over the last 12 months , averaging 3.8% over the last two years. This profitability was lousy for a consumer retail business and caused by its suboptimal cost structureand low gross margin.

Final Judgment

BJ's isn’t a terrible business, but it isn’t one of our picks. With its shares underperforming the market lately, the stock trades at 18.7× forward P/E (or $88.75 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We’re fairly confident there are better investments elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Like More Than BJ's

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.