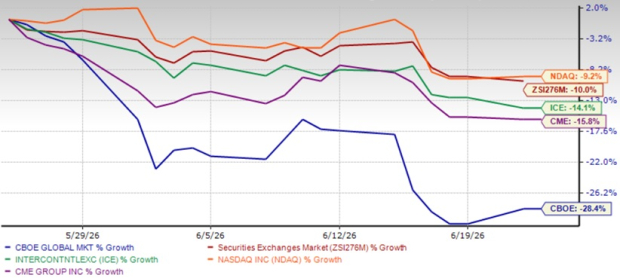

CBOE Stock Plunges 28.4% in a Month: Time to Buy the Dip?

Cboe Global Markets, Inc.CBOE shares have lost 28.4% over the past month compared with the industry's decline of 10%.

The stock has been weighed down by concerns over its valuation compression, competitive threats, and selling pressure after a strong rally that reached a 52-week high in May. Investor sentiment has also been affected by market-share erosion and expectations of lower market volatility that could reduce trading activity. However, the solid earnings growth, record trading volumes, a profitable derivatives and market-data business, and prudent capital deployment position the company well for long-term growth.

Shares of some of its peers, including Intercontinental Exchange Inc.ICE, CME Group Inc.CME, and Nasdaq, Inc.NDAQ, have lost 14.1%, 15.8% and 9.2%, respectively, in the past month.

1-Month Price Performance: CBOE, ICE, CME, NDAQ & Industry

Image Source: Zacks Investment Research

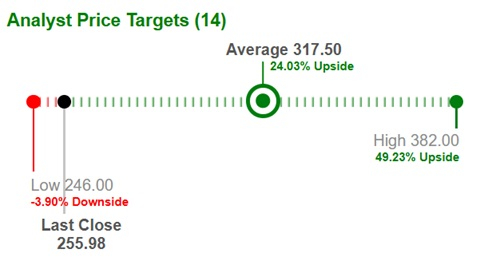

CBOE’s Average Target Price Suggests Upside

Based on short-term price targets offered by 14 analysts, the Zacks average price target is $317.50 per share. The average suggests a potential 24% upside from the last closing price.

Image Source: Zacks Investment Research

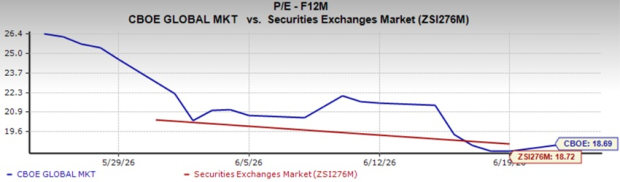

CBOE Valuation

Shares of Cboe Global are currently trading at a discount. Its forward price-to-earnings (P/E) ratio is 18.69X, which is below the industry average of 18.72X.

Image Source: Zacks Investment Research

Shares of Intercontinental Exchange are trading at a discount, while CME and Nasdaq are trading above the industry average.

CBOE’s Growth Projection Encourages

The Zacks Consensus Estimate for Cboe Global’s 2026 earnings per share (EPS) indicates a year-over-year increase of 25%. The consensus estimate for revenues is pegged at $2.75 billion, implying a year-over-year improvement of 13.1%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 5.5% and 2.9%, respectively, from the corresponding 2026 estimates.

Earnings have grown 14.7% in the past five years, better than the industry average of 10.6%. The expected long-term earnings growth rate is 16.8%, %, better than the industry average of 12.2%. It also has a Growth Score of A.

Optimist Analyst Sentiment on CBOE

10 analysts covering the stock have raised estimates for 2026 and 2027 over the past 60 days, with no downward revisions. Thus, the Zacks Consensus Estimate for 2026 and 2027 earnings has moved up 8.8% and 9.1%, respectively, over the same period.

CBOE’s Favorable Return on Capital

Return on equity for the trailing-12 months was 24.9%, which compared favorably with the industry’s average of 16%. This reflects its efficiency in utilizing shareholders’ funds.

Return on invested capital in the trailing-12 months was 14.6%, better than the industry average of 6.7%, reflecting CBOE’s efficiency in utilizing funds to generate income.

What Drives CBOE’s Growth?

Cboe Global’s organic strength lies in a diversified business mix that ensures uninterrupted revenue generation and recurring non-transaction revenues. The company is sharpening its focus on core derivatives, data, clearing and off-exchange businesses through portfolio optimization, including the planned sale of its Canada and Australia operations. At the same time, CBOE is investing in high-growth opportunities such as prediction markets, tokenized products and expanded clearing services.

Trading activity across Cboe’s derivatives complex continues to be the primary organic growth engine. Net revenue rose 29% year over year to $728.9 million, with derivatives net revenue up 32% in the first quarter of 2026. Proprietary SPX options set another quarterly record with average daily volume up 34% year over year to 4.9 million contracts, supported by both shorter-dated and longer-dated demand as market conditions shifted. Management raised its 2026 organic total net revenue growth target to low double-digit to mid-teens.

Growing demand for market data, connectivity services and analytics solutions is driving solid growth in the Data Vantage segment. In the first quarter of 2026, Data Vantage revenue increased to $181.3 million from $152.5 million a year ago, supported primarily by new customer additions and increased product adoption. Management lifted its 2026 Data Vantage organic net revenue growth target to low double-digit.

The multi-quarter realignment is now paired with additional actions aimed at reducing complexity and improving execution. Management expects these initiatives to reduce its workforce by approximately 20% and be substantially completed by the end of 2026. Management also lowered 2026 expense guidance and expects meaningful savings from restructuring initiatives.

CBOE’s strategic investments are well supported by solid capital management. The company has been strengthening its balance sheet with a strong cash position supporting continued investment in technology, sales and product initiatives as well as capital returns, while lowering its debt balance. As of March 31, 2026, it had $569.4 million remaining under existing share repurchase authorizations.

Conclusion

Cboe Global’s growth strategy of expanding its product line across asset classes, broadening geographic reach, diversifying the business mix with recurring revenues, and leveraging technology reflects its operational expertise. A VGM Score of B instils optimism.

Coupled with cheap valuation, optimistic analyst sentiment, favorable ROE and favorable growth estimates, the time appears right for potential investors to bet on this Zacks Rank #1 (Strong Buy) insurer. You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).