PRM Stock Outlook as New Fire Contracts Improve Earnings Visibility

Perimeter Solutions, Inc.PRM is entering a phase in which contract structure matters as much as wildfire activity. Multi-year agreements, annual price escalators and a larger services base are making the Fire Safety business less dependent on any single fire season.

The company still faces weather-driven quarterly swings. Yet its recent contract wins and broader segment mix point to a more durable earnings profile.

Why PRM’s Contract Model Matters More Now

Perimeter’s new five-year agreement with the United States Defense Logistics Agency covers fire suppression foam and services, with a maximum contract value of $500 million. The company expects the financial impact to begin late in 2026, ramp in 2027 and reach a steadier run rate from 2028 onward.

The CAL FIRE renewal adds another five-year anchor. Pricing under that contract rose to align California with other large retardant customers, while annual escalators reinforce revenue durability. Existing federal coverage is also expected to carry forward into the U.S. Wildland Fire Service, supporting planning visibility across agencies.

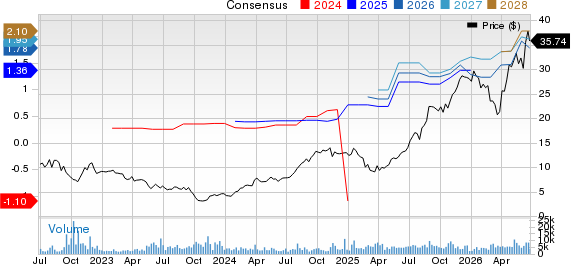

Perimeter Solutions, SA Price and Consensus

Perimeter Solutions, SA price-consensus-chart | Perimeter Solutions, SA Quote

How Perimeter Is Reducing Fire Season Swings

Management believes Perimeter can keep adjusted EBITDA more resilient across normal and milder fire seasons. The company has said variability between a normalized season and a relatively mild one should be roughly in the mid-teens percentage range.

That confidence rests on the full-service air base model and more proactive use of retardants. Federal agencies used an aggressive initial-attack strategy in 2025, and management expects that approach to continue in 2026, which could support demand even when reported acres burned are not especially high.

Perimeter’s Services Base Is Becoming a Shock Absorber

Service revenues in Fire Safety have moved from roughly $30 million a few years ago to $108.3 million in 2025. That represented about 17% of total sales and is largely recognized over time.

This mix matters because most of the service base is fixed each year. It can cushion product-volume volatility when wildfire timing is unfavorable, while also monetizing the air base infrastructure that supports Perimeter’s customer relationships.

Why PRM’s Business Mix Is Broadening

Specialty Products gives Perimeter a second growth engine beyond wildfire-driven demand. The segment includes PDI, Intelligent Manufacturing Solutions and Medical Manufacturing Technologies, which was acquired in January 2026.

In the first quarter of 2026, Specialty Products revenues rose 128% year over year to $79.6 million, while adjusted EBITDA increased 181% to $22.5 million. That contribution helped diversify consolidated results.

Bridger Aerospace Group Holdings, Inc.BAER, which provides aerial wildfire surveillance and suppression services, offers another public-market reference point for wildfire response exposure. The Chemours CompanyCC gives investors a broader specialty-chemicals comparison, although its end-market mix differs from PRM’s fire-safety focus.

What PRM’s Rating Signals Add to the Story

The bottom line is that PRM’s story is becoming less about guessing fire-season severity and more about contracted revenues, services mix and segment diversification. Those elements do not remove wildfire risk, but they improve the visibility of the earnings base.

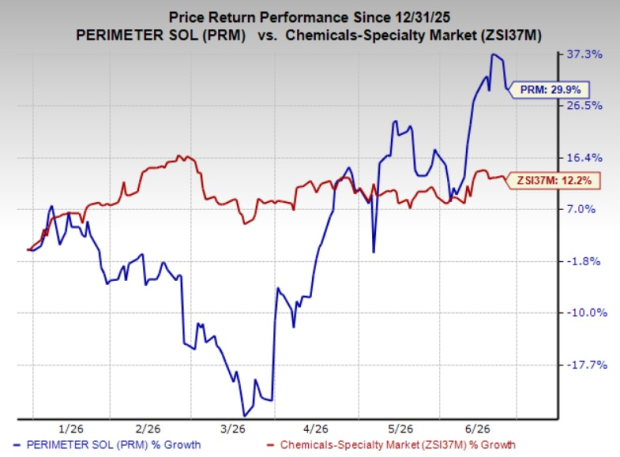

Shares of PRM have gained 29.9% so far this year against the industry’s 12.2% rise.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #1 (Strong Buy). That rank points to favorable estimate-driven support over the next one to three months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Style Scores offer a more mixed signal. PRM has a VGM Score of F, Value Score of F, Momentum Score of F and Growth Score of C. That means the stock has strong Zacks Rank support, but it does not currently screen cheaply or favorably across traditional value and momentum factors.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).