Premium Valuation: Should Investors Still Consider Blackstone Stock?

On the basis of valuation, shares of Blackstone Inc. BX appear to be trading at a premium relative to the industry. The company’s forward 12-month price/earnings (P/E) ratio of 16.48 is above the industry average of 9.87.

Even if we compare BX’s current valuation with two of its closest peers, Apollo Global Management, Inc.APO and The Carlyle Group Inc.CG, the stock appears overvalued. Apollo Global has a P/E (F12M) ratio of 11.31 and Carlyle Group has a forward 12-month P/E ratio of 10.12.

P/E (F12M) Ratio

Image Source: Zacks Investment Research

Despite being the largest alternative asset manager, the relatively stretched valuation of Blackstone may discourage investors from buying the stock. This is because premium-valued stocks are more vulnerable to valuation multiple compression if industry conditions deteriorate. In such a scenario, a reversion toward the mean valuation level could lead to a sharp correction in the stock price.

However, investors should not completely avoid Blackstone solely due to its premium valuation. Before making an investment decision, it is important to assess the company’s underlying fundamentals and growth prospects to determine whether the higher valuation is justified.

Blackstone’s Fundamental Strength

Robust Assets Under Management (AUM) Balance: Blackstone has a solid AUM balance. Its total AUM and fee-earning AUM have recorded compound annual growth rates (CAGR) of 15.6% and 14.4%, respectively, over the last five years (2020-2025). At the end of 2025, the total AUM balance reached a record $1.27 trillion.

Blackstone’s AUM growth has been driven by continued solid capital inflows, the company’s strategic investments in high-growth infrastructure and technology sectors, and a broad fundraising momentum.

The company’s investments in secular growth areas like digital infrastructure, artificial intelligence infrastructure, energy transition and life sciences are major tailwinds.

While Blackstone’s expansion into private wealth channels and insurance platforms has helped in diversifying its revenue sources, new products like perpetual vehicles allow tapping demand from different kinds of investors.

The company’s diversified product base, solid revenue mix and superior position in the alternative investments space are expected to continue supporting AUM growth.

Strong Fundraising Ability: Despite a challenging fundraising environment for asset managers, Blackstone has been raising money. Fundraising for the global private equity and real estate funds resulted in Blackstone’s ‘dry powder’ or the available capital of $198.3 billion as of Dec. 31, 2025.

In 2024 and 2025, the company deployed $133.9 billion and $138.2 billion of capital, respectively. With substantial investable capital, Blackstone is well-positioned to take advantage of market dislocations. Accelerating growth in India and Japan offers attractive opportunities, supporting a strategic deployment of capital.

In April 2025, Wellington, Vanguard and Blackstone announced the formation of an alliance to develop simplified multi-asset investment solutions combining public and private markets. Aiming to broaden investor access to institutional-quality portfolios, the collaboration leverages each firm’s strengths to address long-term diversification and return challenges in wealth and asset management.

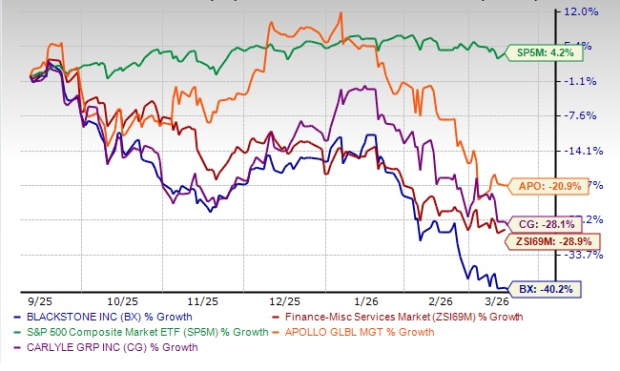

Analyzing BX’s Price Performance

In the past six months, BX shares have lost 40.2% compared with the industry’s decline of 28.9%. During this period, the S&P 500 Index has returned 4.2%.

BX has underperformed both APO and CG in the past six months. Carlyle Group shares have lost 28.1% and the Apollo Global stock has declined 20.9%.

6-Month Price Performance

Image Source: Zacks Investment Research

How to Approach Blackstone Stock Now?

As Blackstone manages assets across private equity, real estate, credit, infrastructure and hedge fund solutions, the diversification enables it to generate multiple revenue streams, including management and performance fees. Moreover, its strong brand and deep relationships with institutional investors are expected to continue to drive steady fund inflows, supporting growth in AUM and fee-related earnings in the long run.

However, a premium valuation compared with the industry does make us apprehensive about the company’s prospects. Tighter credit markets of late, relatively high interest rates, slower deal activity in private equity and real estate, reduced realizations and concerns about exit opportunities are expected to hamper Blackstone’s near-term prospects.

Rather than immediate credit losses, the near-term concerns in the private credit market could weigh modestly on Blackstone, mainly through investor sentiment, potential redemptions and slower fundraising. Caution among retail and wealth-channel investors toward semi-liquid credit vehicles, particularly funds like the Blackstone Private Credit Fund, could lead to temporary outflows or slower inflows, which may slightly pressure AUM and fee-related earnings.

If we look at Blackstone’s estimate revisions, it is clear that analysts are not optimistic regarding the company’s earnings growth prospects. While the company’s earnings estimates for 2026 and 2027 indicate year-over-year growth rates of 14% and 26.8%, respectively, estimates for both years have been revised lower over the past 30 days.

Earnings Estimate Revision

Image Source: Zacks Investment Research

Thus, valuation-aware and more conservative investors should stay away from the BX stock at present and should look for any signs of slowing growth before making any investment decision. However, those who already own the stock can hold onto it as the company is less likely to disappoint in the long run.

Currently, Blackstone carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Blackstone Inc. (BX): Free Stock Analysis Report

Apollo Global Management Inc. (APO): Free Stock Analysis Report

Carlyle Group Inc. (CG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).