Can Flotek's ProFrac Deal Power a High-Margin Growth Engine?

Flotek IndustriesFTK is making a big move to expand its Data Analytics Services (DAS) segment — and its latest acquisition is key to that plan. In April 2025, FTK purchased 30 mobile gas monitoring and dual-fuel optimization units from ProFrac Holding Corp.ACDC for $105 million.

Flotek’s Strategic Bet

More than buying equipment, the transaction is seen as a strategic bet on building recurring, high-margin revenues from real-time gas analytics and remote power solutions. These units help generate electricity on-site, especially in remote areas, by optimizing fuel quality and reducing emissions. Twenty-two of the acquired assets are already deployed under a six-year lease with ProFrac, projected to generate $14 million in EBITDA in 2025. Once all 30 units are up and running, FTK estimates that annual lease revenues could reach $27.4 million in 2026 — almost double the DAS segment’s revenues in 2024. Importantly, the deal was structured to preserve cash by using a combination of equity, promissory notes, and shortfall penalty offsets.

Flotek’s latest move strengthens its partnership with ProFrac and positions the company to tap into the growing off-grid energy market. It also marks a step forward in making Flotek a serious contender in gas analytics and on-site power management — key areas as industries push to cut flaring and boost fuel efficiency.

Peer Check: How Does Flotek Stack Up?

While larger rival ChampionXCHX has expanded its digital offerings through production optimization tools, it is yet to adopt a lease-based model for its analytics technology. ChampionX’s digital revenues remain modest, and its greater reliance on short-cycle markets adds volatility.

In contrast to ChampionX, Flotek’s hybrid approach — pairing its own hardware with built-in analytics and long-term leases — sets it apart in a space where many still depend on one-time sales. It’s unclear if this advantage will lead to steady profits, but the company now has a clear strategy in place.

FTK’s Price Performance, Valuation and Estimates

Shares of Flotek Industries have gained around 54% year to date.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

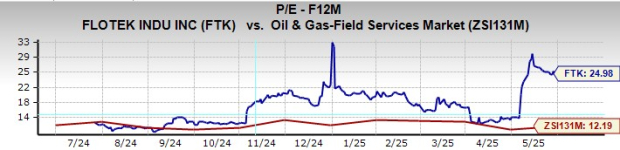

From a valuation standpoint, FTK trades at a forward price-to-earnings ratio of 24.98, compared to the subindustry’s 12.19. Flotek carries a Value Score of D.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

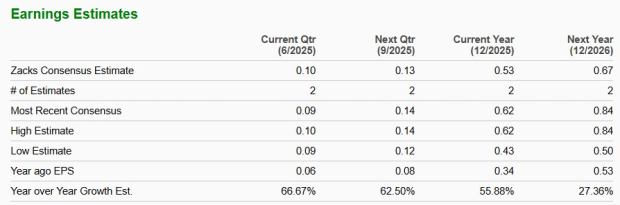

The Zacks Consensus Estimate for Flotek Industries’ 2025 earnings implies a 56% improvement year over year.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #1 (Strong Buy).

You can see the complete list of today’s Zacks #1 Rank stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Flotek Industries, Inc. (FTK): Free Stock Analysis Report

ChampionX Corporation (CHX): Free Stock Analysis Report

ProFrac Holding Corp. (ACDC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).