Key Points

High-speed networking is crucial to AI data centers, which explains why Ciena has seen impressive growth.

The networking component provider continues to see strong order backlog and potential new order inflows.

Investors looking for a growth stock may wish to consider buying this stock now as it may soar higher.

Artificial intelligence (AI) infrastructure stocks have been on a roll over the past few years, driven by massive investments in data centers that have supercharged the growth of several companies in this sector.

From chip designers to foundries to power companies to server manufacturers, the huge AI data center spending has been a tailwind across multiple verticals. Networking component manufacturers have also benefited from investments in AI infrastructure. That's not surprising, as AI data centers require fast networking and high bandwidths to transport large datasets quickly. This ensures that slow transmission speeds don't hamstring model training and inference applications.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

This explains why shares of Ciena(NYSE: CIEN), a provider of high-speed optical networking components and data center interconnect (DCI) products, shot up 176% in 2025. But will this AI stock be able to sustain its momentum in 2026, or should investors consider booking profits and look elsewhere to capitalize on the AI infrastructure market's momentum?

Let's find out.

Image source: Getty Images.

Ciena has gotten off to a solid start in 2026

The good news for Ciena investors is that the stock's rally has continued in 2026. Its shares are up by 47% as of this writing. There is a chance that it can sustain its terrific momentum on the back of a bump in AI data center spending this year. Gartner estimates a 32% jump in spending on data center systems in 2026 to $653 billion, paving the way for Ciena to clock stronger growth this year.

In fact, Ciena expects its growth rate to accelerate in fiscal 2026 (which started in November 2025) to 24% at the midpoint of its $5.7 billion to $6.1 billion guidance range. That'll be an improvement over the 19% revenue growth it clocked in the previous fiscal year. Importantly, Ciena has entered the new fiscal year with a record backlog of $5 billion, which it says is enough to support the acceleration of its growth this year.

It's worth noting that Ciena received $7.8 billion in orders for its optical networking, routing, and switching components last year, exceeding the company's annual revenue of $4.8 billion. A similar scenario can be expected in 2026 as well. Management pointed out on the December 2025 earnings call that "we see indications of strong demand continuing into '27 and beyond, giving us exceptional visibility and confidence in our outlook and medium-term expectations."

Even better, Ciena is seeing an improvement in its margin profile driven by stronger revenue growth and an improving product mix. The company expects this trend to continue in fiscal 2026. It expects "year-over-year gross margin improvements with second half margins being higher than first half margins."

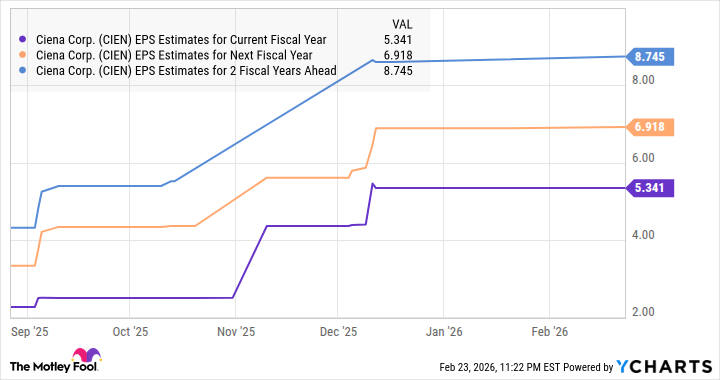

The company's non-GAAP earnings increased by 45% last year to $2.64 per share. The forecast of a stronger revenue increase, along with further margin improvements, should pave the way for another big jump in its bottom line this year. This is precisely what analysts expect in fiscal 2026, followed by robust increases over the next couple of years.

CIEN EPS Estimates for Current Fiscal Year data by YCharts.

Is more upside in the cards this year?

Ciena's impressive gains last year and a solid start to 2026 have made the stock expensive. It's now trading at 40 times forward earnings, well above the tech-laden Nasdaq-100 index's forward earnings multiple of 25.

However, Ciena can justify its valuation. After all, its bottom line is poised to double this year, well above the 14% average earnings growth of companies in the S&P 500 index. Additionally, Ciena's earnings growth may exceed consensus estimates this year on the back of a sizable increase in AI infrastructure spending, its robust backlog, and the possibility of more orders to support the build-out of AI data centers.

So, investors looking for a growth stock to capitalize on the massive AI infrastructure spending can consider buying Ciena, as it has the potential to justify its expensive valuation. In contrast, those worried about its valuation can consider another high-flying name, which is trading at a really attractive valuation.

Should you buy stock in Ciena right now?

Before you buy stock in Ciena, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ciena wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $456,188!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,133,413!*

Now, it’s worth noting Stock Advisor’s total average return is 916% — a market-crushing outperformance compared to 194% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 27, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Ciena. The Motley Fool recommends Gartner. The Motley Fool has a disclosure policy.