After a 41% Rally, Is ConocoPhillips Stock Still Worth Buying?

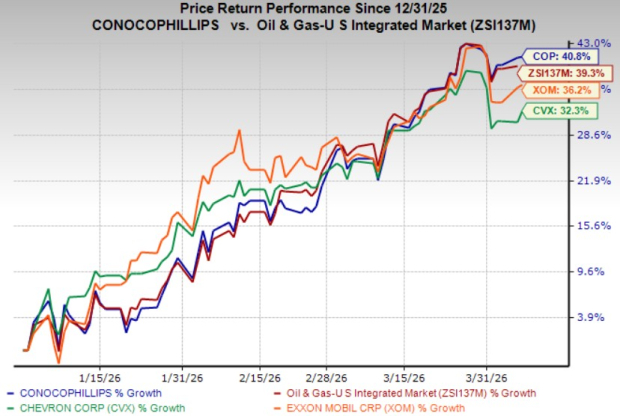

ConocoPhillips COP has jumped 40.8% year to date (YTD), outpacing the 39.3% growth of the industry’s composite stocks, and 36.2% and 32.3% improvements of Exxon Mobil CorporationXOM and Chevron CorporationCVX, respectively.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The outperformance might reflect strong market confidence in COP’s prospects, especially when the pricing scenario of oil is extremely favorable. However, for investment conclusions, one should do a thorough assessment of the company’s fundamentals, growth potential and prevailing market conditions.

High Oil Price & COP’s Key Upstream Assets

The price of West Texas Intermediate (WTI) crude is trading at more than $90 per barrel, according to data from oilprice.com, owing to the ongoing tensions in the Middle East. With COP generating a significant proportion of revenues from crude oil, the high price of the commodity is extremely favorable for the leading oil and gas exploration and production company, much like other energy giants such as XOM and CVX.

The upstream energy giant also has low-cost drilling opportunities across Permian, Eagle Ford and Bakken, that could be successfully developed over two decades. Thus, the outlook for ConocoPhillips’ upstream operations looks highly profitable.

COP’s Low Debt & Cost Reduction Initiatives

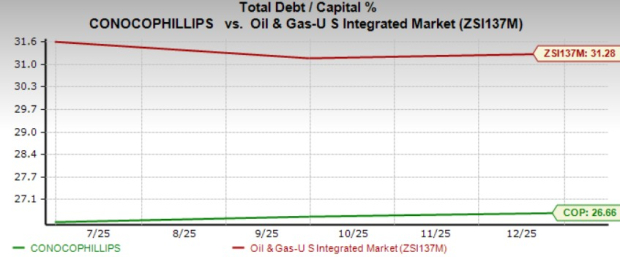

The company has a low exposure to debt capital and hence can rely on its balance sheet to sail through all the business cycles efficiently. Compared to composite stocks in the industry, COP has lower debt exposure, reflected in debt to capitalization of 26.66% compared with the industry’s 31.28%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

ConocoPhillips also has a strong initiative to reduce costs while leaving production unaffected. On its fourth-quarter 2025 earnings call, the upstream major stated its intention of lowering a combined of $1 billion across operating costs and capital expenditure this year while increasing volumes.

Bet on the Stock Right Away?

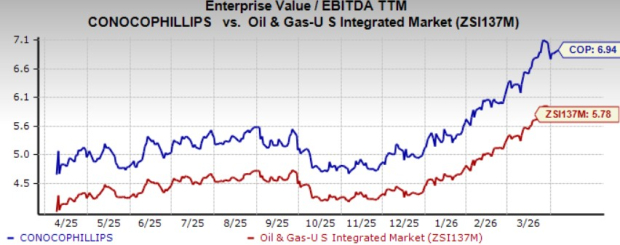

Despite all the positive developments, investors shouldn’t bet on the stock right away as it is currently overvalued. On a relative basis, the stock is trading at a 6.94x trailing 12-month Enterprise Value to Earnings Before Interest, Taxes, Depreciation and Amortization (EV/EBITDA), which is a premium compared with the broader industry average of 5.78x. COP, however, appears cheaper compared to integrated giants such as XOM and CVX, which are currently trading at 10.42x and 10.36x trailing 12-month EV/EBITDA, respectively.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

However, those who have already invested may hold the stock, which currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).