CAH's Pharma Segment Gains 19% in Q2'26: Is the Growth Sustainable?

Cardinal HealthCAH once again delivered a robust performance in the fiscal second quarter of 2026, led by the continued strength of its core Pharmaceutical and Specialty Solutions segment. Segment revenues increased 19% year over year to $61 billion, while profit climbed 29% to $687 million, reinforcing the segment’s position as the company’s primary earnings driver.

The growth was fueled by strong pharmaceutical demand, specialty drug momentum and improved operational efficiency across the distribution network. Cardinal Health also benefited from new customer onboarding and steady performance in its generics sourcing program with Red Oak. GLP-1 medications contributed roughly 6 percentage points of revenue growth during the quarter, reflecting strong demand for these therapies.

With the company posting broad-based growth and raising its fiscal 2026 outlook, investors are now asking a key question: how sustainable is this growth trajectory?

Key Growth Drivers for Fiscal 2026

Specialty Drug Demand Remains a Major Catalyst: Cardinal Health’s focus on specialty pharmaceuticals continues to pay off. The company is aggressively expanding in this higher-growth, higher-margin category through physician networks and MSO platforms, such as Specialty Alliance. Management expects specialty revenues to exceed $50 billion in fiscal 2026, underscoring the segment’s growing importance.

Specialty therapies, particularly in oncology, immunology and chronic disease treatments, are becoming an increasingly large portion of pharmaceutical spending. Cardinal Health’s distribution scale and service infrastructure position it well to capture this demand.

Strength in the Red Oak Generics Program: Another important contributor to growth is Cardinal Health’s generics sourcing partnership through the Red Oak program. The company reported healthy generic unit growth that exceeded long-term expectations, providing a stable source of margin expansion.

Generics typically yield higher profitability for distributors than branded drugs. Continued momentum in this program supports the company’s earnings growth even as drug pricing environments evolve.

Customer Wins and Operational Efficiency: Cardinal Health’s pharmaceutical distribution platform continues to benefit from new customer onboarding and strong demand from existing clients.

At the same time, the company is leveraging technology and infrastructure investments to improve operational efficiency across its distribution network. Initiatives like the Vantus HQ e-commerce platform are helping streamline ordering and supply-chain processes, supporting margins while improving customer experience.

These efficiency gains, combined with disciplined cost management, contributed to the company’s strong operating leverage during the quarter.

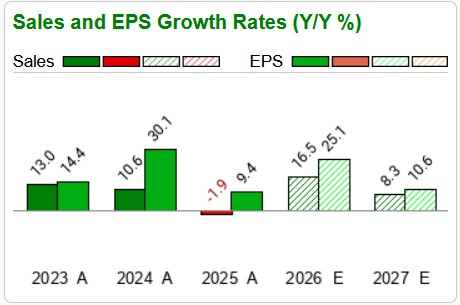

Estimate Revision Trend for CAH

Estimates for Cardinal Health’s fiscal 2026 earnings have moved up 25.1% to $10.31 per share over the past year, while the same for fiscal 2027 earnings has improved 10.6% to $11.40. The positive estimate revision depicts bullish sentiments for the stock.

Image Source: Zacks Investment Research

Competitive Landscape: MCK and COR

Cardinal Health operates in a highly concentrated pharmaceutical distribution industry alongside McKesson MCK and Cencora COR.

McKesson continues to deliver strong results, driven by growth in oncology services, biopharma solutions and North American distribution. The company recently reported double-digit revenue and earnings growth, reflecting strong momentum in its community oncology network and specialty distribution services.

Similarly, Cencora is strengthening its specialty platform through acquisitions, such as OneOncology and Retina Consultants of America, thereby expanding its reach in community oncology and physician services. These initiatives have helped drive operating income growth and continued expansion in its U.S. Healthcare Solutions segment.

Despite intense competition, Cardinal Health maintains a strong position due to its scale, supply-chain expertise and diversified services across pharmaceutical distribution, specialty platforms and logistics.

Price Performance and Valuation Outlook

Cardinal Health’s improving fundamentals have translated into stronger earnings visibility and guidance. The company recently raised its fiscal 2026 EPS outlook to $10.15-$10.35, implying growth of roughly 23-26% year over year.

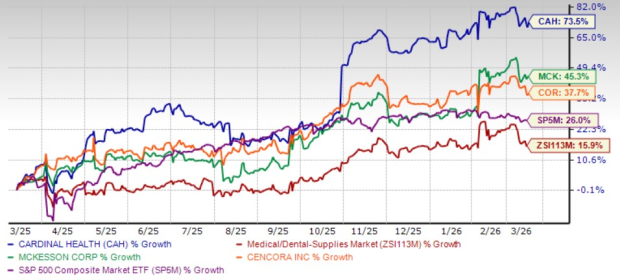

Such strong earnings momentum supports the stock’s price performance and suggests that Cardinal Health remains attractively positioned relative to its historical growth profile. The company’s shares have surged 73.5% in the past year compared with the industry’s growth of 15.9% and the S&P 500 Index’s increase of 26%. CAH also outperformed its peers McKesson and Cencora, which have gained 45.3% and 37.7%, respectively, in the same time period.

One-Year Price Performance

Image Source: Zacks Investment Research

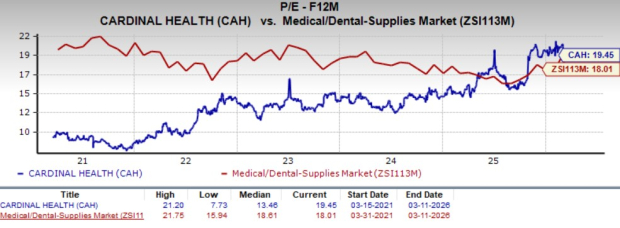

Continued profit expansion from the pharmaceutical segment and contributions from growth businesses such as Nuclear and Precision Health Solutions and OptiFreight Logistics could further support valuation upside. CAH’s shares currently trade at a forward 12-month price-to-earnings (P/E) of 19.45X, higher than the industry average of 18.01X.

Image Source: Zacks Investment Research

Risks and Potential Challenges

While Cardinal Health’s growth outlook appears solid, several factors could influence sustainability. Part of the recent growth was driven by GLP-1 demand and new customer wins, which may moderate over time as comparisons become tougher.

Additionally, some revenue tailwinds, such as distributor restocking or customer onboarding, may normalize in the forthcoming quarters. The company also faces industry-wide pressures, including pricing dynamics, regulatory changes and competitive intensity, from major peers like McKesson and Cencora.

Conclusion

Cardinal Health’s Pharmaceutical and Specialty Solutions segment remains the primary growth engine, delivering robust revenue and profit expansion in fiscal 2026. Strong specialty drug demand, generics program strength and improved operational efficiency are supporting the company’s earnings momentum.

Although some growth drivers, such as GLP-1 demand and recent customer additions, may normalize over time, CAH’s strategic focus on specialty distribution and physician services provides a durable long-term opportunity.

Given the strong earnings trajectory, improving operational performance and favorable industry trends, Cardinal Health appears well positioned for continued growth. For investors seeking exposure to the resilient pharmaceutical distribution sector, CAH currently looks like a compelling bet.

Cardinal Health presently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

McKesson Corporation (MCK): Free Stock Analysis Report

Cencora, Inc. (COR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).