Credo Technology Stock Outlook Hinges on AI and Optical Scale

Credo Technology Group Holding Ltd CRDO is moving through a new phase of its AI connectivity story. The question is whether rapid demand can broaden beyond one product family while profitability holds.

The setup now spans active electrical cables (AECs), optical digital signal processors, PCIe connectivity and silicon photonics. That wider portfolio gives investors more to track and raises the bar for execution.

CRDO Growth Now Reaches Beyond AECs

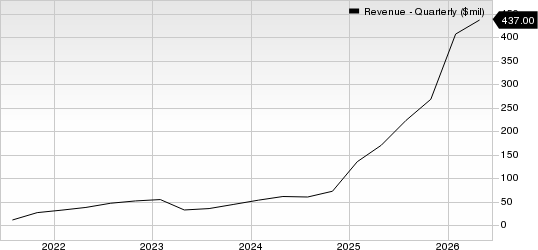

Credo’s growth is no longer just an AEC story. Fiscal 2026 revenues reached $1.3 billion, up 206% year over year, as AI infrastructure ramps lifted demand across the product base.

Credo Technology Group Holding Ltd. Revenue (Quarterly)

Credo Technology Group Holding Ltd. revenue-quarterly | Credo Technology Group Holding Ltd. Quote

AECs remain a key engine for in-rack and multi-rack AI connectivity. Yet management is also pointing to optical products, retimers and digital signal processors as larger contributors, helping frame Credo as an AI connectivity platform.

Lattice Semiconductor CorporationLSCC, a peer in the semiconductor space, offers low-power field-programmable gate arrays used in communications, computing, industrial and other applications. It gives investors another infrastructure-linked chip name to compare against CRDO’s connectivity focus.

Credo Is Building a Bigger Optical Engine

Optics has become the clearest next pillar. Credo completed the DustPhotonics acquisition in May 2026, adding silicon photonics PIC capabilities and strengthening its high-speed optical portfolio.

That deal fits with ZeroFlap optical transceivers and optical digital signal processors. Management expects optical revenues to exceed $600 million in fiscal 2027, with ZeroFlap optics, silicon photonics photonic integrated circuits and optical digital signal processors each contributing more than $100 million.

The optical opportunity also gives Credo more exposure to 800-gigabit and 1.6-terabit connectivity needs. FormFactor, Inc.FORM, which provides advanced semiconductor test and measurement solutions, sits in a different part of the semiconductor ecosystem but remains relevant to data-infrastructure demand.

CRDO Execution Still Depends on Big Customers

Customer concentration remains the main counterweight to the growth story. In the fourth quarter of fiscal 2026, four hyperscale customers each accounted for at least 10% of revenues.

The top three represented 34%, 27% and 16% of revenues. That concentration can magnify upside during deployment ramps because one large program can move revenues quickly.

Credo Technology Group Holding Ltd. Price, Consensus and EPS Surprise

Credo Technology Group Holding Ltd. price-consensus-eps-surprise-chart | Credo Technology Group Holding Ltd. Quote

The same structure can create volatility. If a major customer pauses a deployment, changes timing or adds suppliers, quarterly revenues can shift faster than the long-term opportunity would suggest.

Credo is working to diversify across hyperscalers, neo clouds and other customers. Still, management expects three to four customers to remain above 10% of revenues in the coming quarters.

Credo Margins Show Scale but Face Transitions

Credo’s profitability shows the leverage in the model. Fourth-quarter fiscal 2026 non-GAAP gross margin was 68.3%, while non-GAAP operating income reached $216.7 million.

Free cash flow was $177.5 million in the quarter. The company ended fiscal 2026 with $1.4 billion in cash, cash equivalents and short-term investments.

Margins may not move in a straight line. Non-GAAP operating expenses were $81.7 million in the fiscal fourth quarter and are expected to rise to $86-$90 million in the current quarter.

The mix shift toward newer optical products can also affect earnings cadence. Management expects fiscal 2027 non-GAAP gross margin to be broadly consistent with fiscal 2026, but higher spending and product transitions can make quarterly results less linear.

How CRDO Signals Fit the Setup

The bottom line is that Credo has a larger platform story, but investors still need confidence in customer ramps, optical execution and expense discipline. The stock’s growth profile depends on those factors holding together.

CRDO currently carries a Zacks Rank #1 (Strong Buy). That rank is consistent with a stock benefiting from favorable earnings estimate revision trends, which are central to the Zacks Rank framework.

The Style Scores add a more mixed layer. CRDO has a Momentum Score of A, Growth Score of B and VGM Score of C, pointing to favorable price action and growth characteristics but a less complete profile across all styles.

The weaker Value Score of F keeps the investment case rooted more in execution and growth confidence than in cheap valuation. For investors, CRDO remains a stock where the outlook hinges on whether optical scale and broader AI connectivity demand can offset concentration and transition risks.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).