Salesforce vs. Adobe: Which AI-Driven Software Stock Has an Edge?

Salesforce, Inc.CRM and Adobe Inc.ADBE sit at the center of the enterprise software landscape, both riding on strong tailwinds from digital transformation and the rapid rise of artificial intelligence (AI). Salesforce dominates customer relationship management, while Adobe leads in creative and document software.

As AI becomes the defining battleground, both companies are aggressively embedding it into their platforms to unlock new growth. But which stock offers the stronger investment case right now? Let’s break it down.

The Case for Salesforce Stock

Salesforce remains the global leader in customer relationship management, a position it has consistently held, according to Gartner. However, the company is no longer just a CRM provider. Rather, it is evolving into a full-scale enterprise platform.

Salesforce is building a broader enterprise ecosystem centered on AI, data and collaboration. Acquisitions like Slack and Informatica highlight this ambition, while smaller AI-focused deals such as Doti AI and Spindle AI show management’s urgency in staying ahead of the curve.

AI is now central to Salesforce’s growth story. Since the 2023 rollout of Einstein GPT, Salesforce has been embedding generative AI across its offerings to help companies automate processes, improve decision-making and strengthen customer relationships.

Its latest innovation, Agentforce, is gaining momentum. Combined with Data Cloud, these AI-driven offerings brought in $2.9 billion in recurring revenues in the fourth quarter of fiscal 2026, representing more than 200% year-over-year increase. Agentforce alone generated $800 million in recurring revenues, up 169% year over year. More than 60% of Agentforce deals came from existing clients, showing Salesforce’s success in cross-selling AI features to its user base.

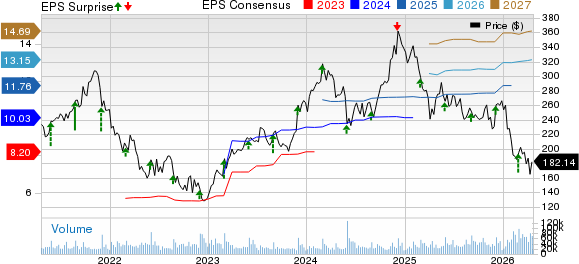

Financially, Salesforce continues to deliver steady performance. In the fourth quarter of fiscal 2026, revenues and non-GAAP earnings per share (EPS) rose 12% and 37% year over year, respectively. Both top and bottom lines surpassed the Zacks Consensus Estimate by 0.32% and 25.69%, respectively.

Salesforce, Inc. Price, Consensus and EPS Surprise

Salesforce, Inc. price-consensus-eps-surprise-chart | Salesforce, Inc. Quote

The Case for Adobe Stock

Adobe is witnessing solid momentum across its AI-powered tools, such as Creative Cloud Pro and Acrobat. Its AI-first offerings, such as Firefly and Acrobat AI Assistant, are also gaining traction. By adding conversational and agentic interfaces to Adobe Reader, Acrobat and Express, the company is making its products more useful for consumers. These integrations also improve productivity for creative professionals, which supports higher adoption.

Firefly is becoming a key growth driver within Adobe’s creative ecosystem. Firefly models and applications like Photoshop, Illustrator and Premiere, which integrate third-party models, are gaining traction among Creators and Creative professionals. New solutions like Premiere mobile with YouTube integration and Photoshop mobile are helping creators develop content anywhere.

Adobe’s growing partner ecosystem further strengthens its AI strategy. The company has integrated with major AI platforms, including Amazon Web Services, Microsoft Azure, Google Gemini, Microsoft Copilot and OpenAI. Firefly also supports models from several well-known AI startups, giving users a broad set of generative options. In the first quarter of fiscal 2026, Firefly’s generative credit consumption grew 45% sequentially, while its subscription annual recurring revenues soared 75%.

Financially, Adobe is doing well. In the first quarter of fiscal 2026, the company’s top and bottom lines soared 12% and 19.3%, respectively, year over year. Revenues and EPS surpassed the respective Zacks Consensus Estimate by 1.86% and 3.06%, respectively.

Adobe Inc. Price, Consensus and EPS Surprise

Adobe Inc. price-consensus-eps-surprise-chart | Adobe Inc. Quote

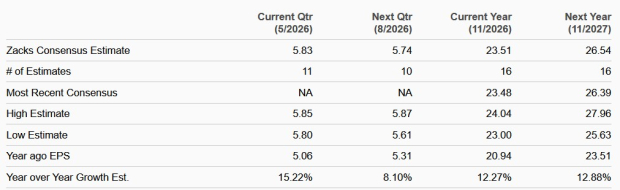

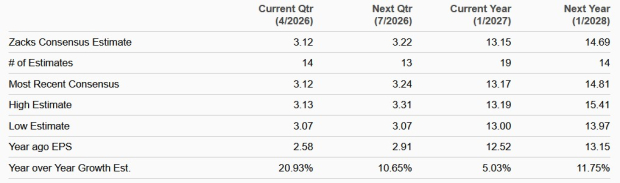

Salesforce vs. Adobe: EPS Growth Outlook

Both companies are riding on the AI wave, but near-term EPS growth looks slightly stronger for Adobe. The consensus estimates for Adobe’s fiscal 2026 and 2027 EPS point to a year-over-year increase of 12.3% and 12.9%, respectively. Estimates for Salesforce’s fiscal 2027 and 2028 EPS call for growth of 5% and 11.8%, respectively.

Adobe Earnings Estimates

Image Source: Zacks Investment Research

Salesforce Earnings Estimates

Image Source: Zacks Investment Research

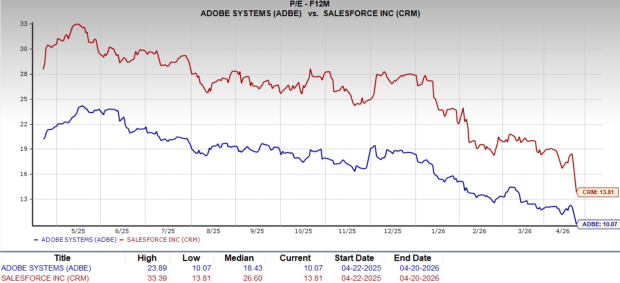

CRM vs. ADBE: Price Performance and Valuation

Year to date, both stocks have declined, but Adobe has held up slightly better. CRM has plunged 29.6%, while ADBE has dropped 28.9%.

Image Source: Zacks Investment Research

Adobe looks attractive on the valuation front as well. Adobe trades at 10.07 times forward 12-month earnings, while Salesforce trades at 13.81 times.

Image Source: Zacks Investment Research

Conclusion: ADBE Has an Edge Over CRM

Both Salesforce and Adobe are well-positioned to benefit from the AI wave. Salesforce is building a broad AI-driven platform, which offers long-term potential. Adobe, through its innovative product portfolio, is also translating AI into tangible results. However, a stronger earnings growth outlook and low valuation give ADBE an edge over CRM from an investment point of view.

Salesforce and Adobe each carry a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).