Delta Air Lines (DAL) Stock Near Highs Ahead of Q2 Earnings: Buy, Hold, or Sell?

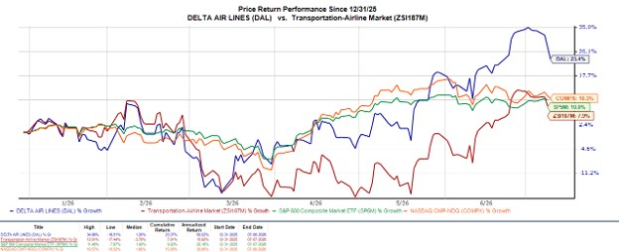

Delta Air Lines DAL) has been one of the airline industry's standout performers in 2026, with its stock climbing more than 20% YTD as investors have grown more optimistic about premium travel demand, improving industry pricing, and easing fuel cost concerns.

With Delta scheduled to report Q2 results before the market opens on Friday, July 10, investors will be looking to see whether the carrier can justify its strong rally and provide an encouraging outlook for the remainder of the busy summer travel season.

Image Source: Zacks Investment Research

Delta's Q2 Expectations

Wall Street expects another quarter of healthy revenue growth, driven by resilient demand for international routes, premium cabin bookings, and Delta’s expanding loyalty ecosystem.

Current consensus estimates call for Q2 revenue of $17.74 billion, representing more than 6% year over year growth. Quarterly EPS is expected at $1.50, down from last year's Q2 profit of $2.10 per share as higher labor expenses and elevated fuel costs weigh on margins.

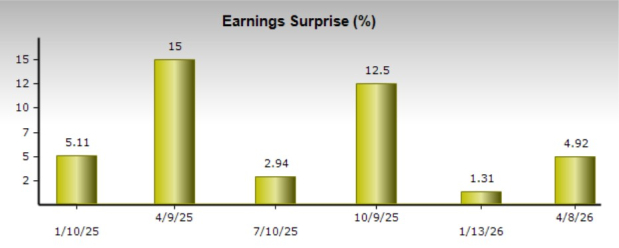

Although earnings are expected to decline from last year's exceptionally strong comparison, Delta has developed an impressive track record of execution, exceeding EPS expectations for six consecutive quarters.

Image Source: Zacks Investment Research

Premium Demand Remains Delta's Biggest Strength

Unlike many airlines that remain heavily dependent on price-sensitive domestic leisure travelers, Delta has increasingly differentiated itself through premium offerings and corporate travel.

Management has emphasized:

- Premium seating demand

- International travel strength

- Corporate travel recovery

- American Express AXP) loyalty partnership growth

These higher-margin revenue streams have helped Delta generate more stable profitability than many of its airline peers, even as industry conditions fluctuate. Analysts also expect premium travel demand to remain healthy throughout the summer travel season.

Fuel Costs and Guidance Will Be the Biggest Story

While investors will naturally focus on quarterly earnings, management's outlook may ultimately matter more than the reported numbers.

Earlier this year, Delta warned that fuel expenses would remain elevated during the June quarter, although declining oil prices in recent weeks have improved the industry's outlook heading into the second half of 2026.

Investors will want to monitor Delta's commentary on:

- Third-quarter demand trends

- Corporate booking activity

- International travel demand

- Fuel expense expectations

- Capacity growth

- Full-year earnings outlook

If management strikes a confident tone, investors may become increasingly optimistic about airline profitability heading into the remainder of 2026.

Is Delta Stock Still Reasonably Valued?

Despite Delta’s impressive YTD rally, DAL remains relatively attractive compared to many large-cap companies.

Airline stocks generally trade at modest earnings multiples due to the cyclical nature of the business. However, Delta has earned a premium valuation thanks to its industry-leading operational performance, strong balance sheet improvements, premium customer mix, and growing loyalty revenue.

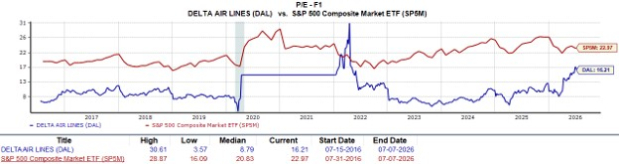

At around $86 a share, DAL currently trades at 16X forward earnings, with the Zacks Transportation-Airline Industry average at 11X. Notably, domestic competitors United Airlines UAL) and American Airlines AAL) are trading at forward earnings multiples of 12X and 37X, respectively.

Given its moderate P/E valuation, the market may continue to reward Delta if management demonstrates that earnings growth can remain durable despite macroeconomic uncertainty.

Image Source: Zacks Investment Research

Bottom Line

Delta enters its Q2 report with considerable momentum as travel demand has remained resilient and industry fundamentals continue to improve. Investors will be looking for confirmation that premium travel, international demand, and loyalty revenues are offsetting cost pressures in hopes that management provides constructive guidance for the remainder of 2026.

That said, much of the recent optimism may already be reflected in the share price following the stock's strong advance this year. While Delta remains one of the highest-quality names in the airline industry, investors may want to await management's latest outlook before becoming more aggressive with DAL landing a Zacks Rank #3 (Hold) at the moment.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).