DELL Stock Jumps 17% in a Month: Here Are 3 Reasons Why It Is a Buy

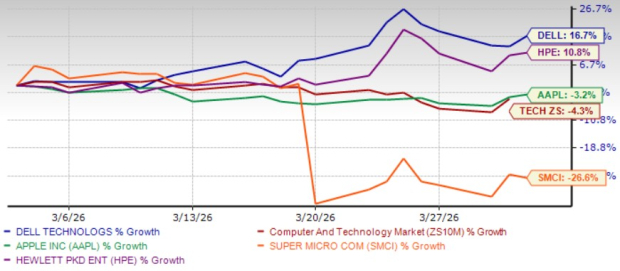

Dell TechnologiesDELL shares have jumped 16.7% in a month, outperforming the broader Zacks Computer and Technology sector’s fall of 4.3%, as well as peers such as AppleAAPL, Super Micro ComputerSMCI and Hewlett Packard EnterpriseHPE. Over the same time frame, shares of Apple and Super Micro Computer have dropped 3.2% and 26.6%, respectively, while Hewlett Packard shares have returned 10.8%. DELL is benefiting from strong AI infrastructure demand that is driving its top-line growth. The company not only boasts strong liquidity but is also trading cheaper, as suggested by a Value Score of B. Let us dig deep to discuss these factors, which make the DELL stock a buy.

DELL Stock’s Price Performance

Image Source: Zacks Investment Research

DELL’s Strong AI Growth Boosts Competitive Prowess

Dell Technologies is benefiting from accelerating AI infrastructure demand. In fiscal 2026, the company recorded more than $64 billion in AI-optimized server orders and shipped above $25 billion worth of AI infrastructure, ending the year with a record backlog of $43 billion. DELL’s AI infrastructure solutions are gaining traction among enterprises, sovereign entities and next-generation cloud providers, with the company serving more than 4,000 AI customers globally.

DELL’s ability to optimize AI systems for performance, deliver rapid deployment at scale and provide lifecycle services has strengthened its competitive position. The company’s integrated rack-scale systems and data center solutions allow customers to deploy AI clusters efficiently, while managing the total cost of ownership. These capabilities are helping Dell Technologies capture opportunities as organizations scale AI workloads across industries. This is expected to drive top-line growth with AI server revenues to reach $50 billion in fiscal 2027, representing more than 100% year-over-year growth.

For fiscal 2027, revenues are expected between $138 billion and $142 billion, indicating 23% year-over-year growth at the mid-point. The Zacks Consensus Estimate for revenues is pegged at $141.03 billion, suggesting 24.2% growth from the figure reported in fiscal 2026.

For the first quarter of fiscal 2027, revenues are expected between $34.7 billion and $35.7 billion, with the mid-point of $35.2 billion suggesting 51% year-over-year growth. Dell Technologies anticipates a 53% year-over-year rise at the mid-point for the combined Infrastructure Solutions Group (“ISG”) and Client Solution Group (“CSG”), with ISG expected to grow more than 100%, supported by $13 billion of AI server revenues, and CSG is expected to inch up 2%. The Zacks Consensus Estimate for revenues is pegged at $35.28 billion, suggesting 50.89% growth from the figure reported in the year-ago quarter.

Dell Technologies Inc. Price and Consensus

Dell Technologies Inc. price-consensus-chart | Dell Technologies Inc. Quote

Strong top-line growth is expected to boost profits. Dell Technologies now expects first-quarter fiscal 2027 non-GAAP earnings of $2.90 per share (+/- 10 cents) at the mid-point, indicating 87% year-over-year growth. For fiscal 2027, non-GAAP earnings are expected to be $12.90 per share (+/- 25 cents) at the mid-point, implying a 25% year-over-year rally. The Zacks Consensus Estimate for first-quarter fiscal 2027 earnings is pegged at $3.17 per share, up 12% over the past 30 days, indicating a 104.52% surge from the figure reported in the year-ago quarter. The consensus mark for fiscal 2027 earnings is currently pegged at $12.77 per share, up 3.5% over the past 30 days, indicating 23.98% from the fiscal 2026 reported figure.

DELL’s Strong Liquidity Aids Prospects

Dell Technologies’ prospects benefit from strong liquidity. In fiscal 2026, the company generated more than $11 billion in operating cash flow and ended fiscal 2026 with $13.3 billion in cash and investments. This healthy cash position allows Dell Technologies to continue investing in strategic areas like AI infrastructure and data center modernization.

Apart from supporting business expansion, Dell Technologies’ strong cash generation enables consistent shareholder returns. In fiscal 2026, the company returned $7.5 billion to shareholders through dividends and share repurchases, including $2.2 billion in the fiscal fourth quarter. DELL also raised its dividend 20% and increased its share repurchase authorization by $10 billion, reflecting confidence in its long-term growth prospects.

DELL Shares Are Trading Cheap

In terms of the forward 12-month price/earnings (P/E), DELL is trading at 12.99X, lower than the broader sector’s 22.17X. Dell Technologies is also trading at a discount against Apple shares, which are currently trading at 28.93X. Shares of Super Micro Computer and Hewlett Packard are trading at 8.19X and 9.43X, respectively.

DELL Stock’s Valuation

Image Source: Zacks Investment Research

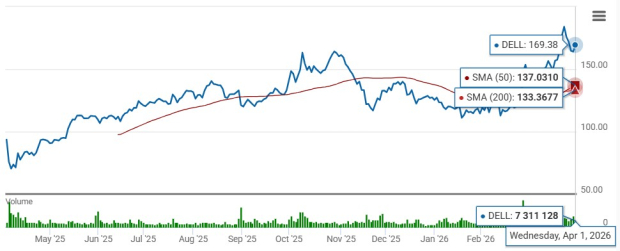

Technically, Dell Technologies is trading above the 50- day and 200-day moving averages, indicating a bullish trend.

DELL Stock Trades Above 50-Day & 200-Day SMAs

Image Source: Zacks Investment Research

Conclusion

Dell Technologies’ prospects ride on strong AI infrastructure demand, impressive liquidity position and cheap valuation. An expanding clientele across neoclouds, sovereigns and enterprise customers bodes well for the company’s top-line growth. The company’s disciplined approach toward capital spending is a key catalyst.

DELL currently has a Zacks Rank #2 (Buy) and a Growth Score of B, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeThis article originally published on Zacks Investment Research (zacks.com).