APLD's Customer Concentration Remains Elevated: Is Growth at Risk?

Applied Digital's APLD customer concentration remains elevated despite continued efforts to diversify its hyperscale customer base. APLD has expanded its development pipeline and is actively pursuing additional leasing opportunities, but contracted revenue remains heavily concentrated among a limited number of customers, creating an ongoing risk to long-term revenue visibility.

The concentration remains significant. Of the company's approximately $36 billion in total contracted lease revenues, $11 billion is attributable to CoreWeave, while a separate hyperscaler anchors Delta Forge 1, Polaris Forge 3 and Delta Forge 2 and accounts for $20 billion. The remaining $5 billion is tied to a third hyperscaler at Polaris Forge 2. Together, just two customers represent close to 90% of total contracted revenues, leaving long-term growth tightly bound to the demand and credit trajectory of a narrow set of counterparties.

The risk becomes more pronounced as Applied Digital expands its AI data center platform. Initial operations at Delta Forge 1, Polaris Forge 3 and Delta Forge 2 are not expected until 2027 and 2028, meaning future growth will depend heavily on the successful execution and continued expansion of existing customer relationships. While the company continues to market additional development sites and broaden its hyperscaler pipeline, customer diversification has not kept pace with the growth in contracted capacity.

Hence, any slowdown in deployment plans, capital spending or credit quality among Applied Digital's largest customers could have an outsized impact on future revenue growth. Until the company adds customers capable of contributing significantly to the revenue, concentration risk is likely to remain a key overhang.

APLD Faces Stiff Competition

Applied Digital's customer concentration remains significantly higher than that of its peers, Equinix EQIX and Digital Realty Trust DLR. Equinix benefits from a highly diversified customer base spanning enterprises, cloud providers and network operators, while Digital Realty Trust generates revenue from a broad mix of hyperscale and colocation customers. In contrast, Applied Digital derives the majority of its contracted lease revenues from a handful of hyperscale customers.

Unlike Equinix and Digital Realty Trust, which are less dependent on any single tenant, Applied Digital remains exposed to customer-specific spending decisions and counterparty risks.

APLD’s Share Price Performance, Valuation & Estimates

Applied Digital’s shares have returned 88.7% year to date, while the broader Zacks Finance sector has declined 3.7% and the Zacks Financial-Miscellaneous Services industry has plunged 6%.

APLD Stock’s Performance

Image Source: Zacks Investment Research

Applied Digital stock is trading at a forward 12-month price/sales of 16.87X compared with the broader sector’s 8.82X. APLD has a Value Score of F.

APLD’s Valuation

Image Source: Zacks Investment Research

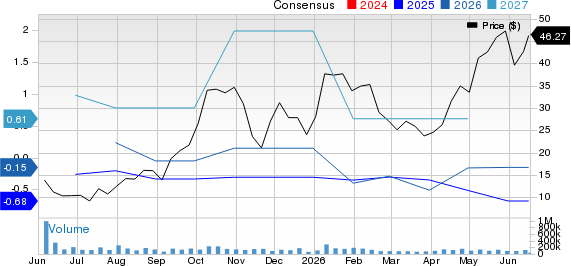

The Zacks Consensus Estimate for fiscal 2026 loss is pegged at 68 cents per share. Applied Digital reported a loss of 80 cents per share in the previous year.

Applied Digital Corporation Price and Consensus

Applied Digital Corporation price-consensus-chart | Applied Digital Corporation Quote

APLD currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).