Should DNN Stock be in Your Portfolio Before Q1 Earnings?

Denison Mine Corp. DNN is expected to report a year-over-year decline in revenues and a loss when it reports first-quarter 2026 results next week.

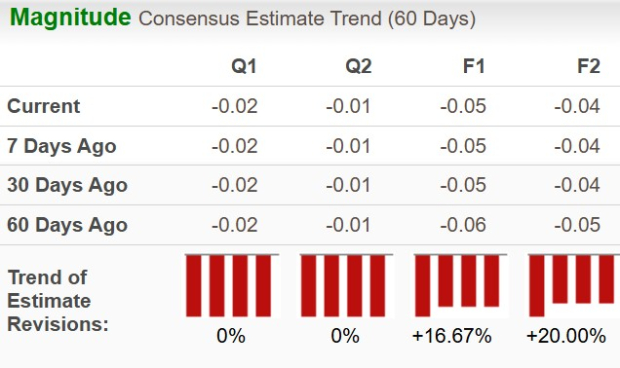

The Zacks Consensus Estimate for Denison Mine’s revenues for the quarter is currently pegged at $0.81 million, suggesting a 15.6% year-over-year decline. The consensus estimate for first-quarter earnings has remained unchanged at a loss of two cents per share in the past 60 days. It, however, suggests an improvement from the loss of three cents per share reported in the prior-year quarter.

Image Source: Zacks Investment Research

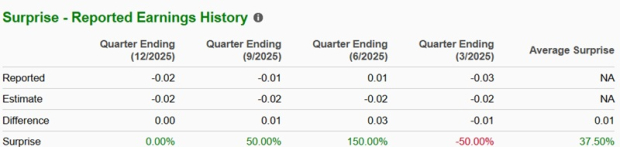

Denison Mine’s Earnings Surprise History

In the trailing four quarters, DNN’s earnings have outpaced the Zacks Consensus Estimate in two quarters, missed in one quarter and came in line in the remaining quarter. The company has delivered an average earnings surprise of 37.50% for the period.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

What the Zacks Model Unveils for DNN Stock

Our proven model does not conclusively predict an earnings beat for Denison Mine this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here.

Earnings ESP: The Earnings ESP for DNN is +0.00%. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Zacks Rank: Denison Mine currently sports a Zacks Rank of 1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Likely to Have Shaped Denison Mine’s Q1 Performance

Denison Mine is a uranium exploration and development company focused on the Athabasca Basin region of northern Saskatchewan, Canada. It has a 95% interest in its flagship Wheeler River Uranium Project, which is the largest undeveloped uranium project in the infrastructure-rich eastern portion of the Athabasca Basin.

In February 2026, Denison Mine announced that its board of directors approved the construction of the Phoenix In-Situ Recovery (ISR) uranium mine at Wheeler River. Site preparation and construction activities were scheduled to begin in March 2026.

Denison Mine also owns a 22.5% interest in the McClean Lake Joint Venture (MLJV), and the McClean Lake uranium mill, which processes ore from the Cigar Lake mine under a toll milling agreement. The company’s toll milling revenues fluctuate depending on the timing and volume of uranium processed at the mill, as well as changes in the estimated mineral resources at Cigar Lake.

In 2025, the mill processed 19.1 million pounds of uranium, up from 16.9 million pounds in 2024. Denison Mine recorded toll milling revenues of CAD 4.9 million ($3.52 million) for the year, reflecting a 22% year-over-year increase attributed to higher production.

However, operators of the Cigar Lake mine now expect production of approximately 17.5-18.0 million pounds (100% basis) in 2026 compared with 19.1 million pounds in 2025. Given the projected decline in annual production, first-quarter throughput at the McClean Lake mill is also likely to have been lower year over year, which is expected to have negatively impacted Denison Mine’s toll milling revenues.

Denison Mine also stated that it plans to sell uranium production received from the McClean Lake SABRE mine, which commenced operation in 2025. Around 300,000 pounds of uranium are projected to be sold in 2026 for net proceeds (after selling costs) of approximately CAD29 million.

On the expense side, evaluation costs are likely to have remained elevated as Denison Mine progressed toward a final investment decision (FID) for the Phoenix project and continued advancing other development activities. Increased staffing to support project advancement is also likely to have added to costs. In addition, exploration expenses are typically higher during the first and third quarters due to the timing of winter and summer exploration programs in northern Saskatchewan. This, along with higher operating expenses and costs related to the Phoenix project, is expected to have led to a loss in the quarter.

In 2025, DNN sold 500,000 pounds of uranium from its physical uranium investments at a weighted average selling price of CAD108.50 (US$78.63) per pound, representing a realized gain of CAD36.0 million ($24.6 million). The company has also entered into sales commitments with market-linked pricing terms for 550,000 pounds of uranium scheduled for delivery in 2026.

Uranium prices averaged around $88 per pound during the first quarter of 2026, up 41% year over year. Given the strong pricing environment, Denison Mine is likely to have monetized additional uranium holdings during the quarter, potentially generating realized gains on uranium sales. This is expected to have set off some of the loss in the quarter.

DNN’s Price Performance & Valuation

Denison Mine has gained 155.7% over the past year, well ahead of the industry’s 60.5% growth. The Basic Materials Sector and S&P 500 have gained 46.6% and 36.3%, respectively, over the same period. Peers NexGen EnergyNXE and Ur-Energy Inc. URG have gained 130.7% and 166.1%, respectively.

Image Source: Zacks Investment Research

DNN is trading at a price/book multiple of 13.23X, a significant premium to the industry’s 2.08X. NexGen Energy and Ur-Energy Inc. are cheaper options at 6.49X and 9.49X, respectively.

Image Source: Zacks Investment Research

Investment Thesis on DNN

Denison Mine’s long-term investment case is anchored in its portfolio of four prospective, low-cost uranium development assets: Phoenix, Gryphon, Midwest and THT/Waterbury. Demand for nuclear energy is expected to accelerate as countries increasingly shift toward low-carbon energy sources, while years of underinvestment have constrained new uranium supply.

Against this backdrop, DNN’s strategy of advancing a diversified pipeline of mining, development and exploration assets places it in a strong position to benefit from favorable long-term market dynamics. Backed by high-quality resources, a solid balance sheet and a clearly defined path to production, the company’s growth story remains intact.

Should You Buy DNN Stock Now?

Denison Mine’s premium valuation appears justified given its high-quality asset base, cost-efficient ISR mining approach and robust project economics. Although earnings are expected to remain under pressure in the near term due to ongoing development spending, this is typical for a company transitioning from development to production. No matter how the upcoming quarterly results play out, the stock remains an attractive play on the long-term uranium theme and continues to stand out as a solid investment choice.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).