Is Arm Holdings Stock a Buy After Its Record Q4 Earnings?

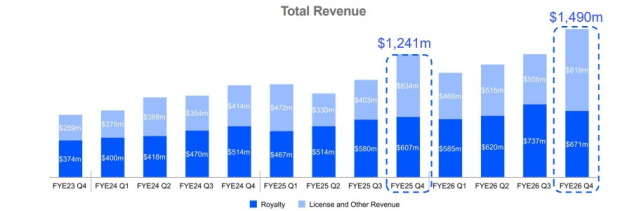

Arm Holdings plc ARM reported fourth-quarter fiscal 2026 revenues of $1.49 billion, up 20% year over year and above expectations. Adjusted earnings per share came in at 60 cents, beating the Zacks Consensus Estimate by 2 cents. The company also delivered its highest quarterly revenue in history, underscoring the accelerating adoption of Arm-based architectures across cloud, AI and edge computing workloads.

Image Source: ARM

Image Source: ARM

For the full fiscal year, revenues climbed 23% year over year to a record $4.92 billion. Licensing revenues increased 25% to $2.31 billion, while royalty revenues rose 21% to $2.61 billion. Non-GAAP EPS reached a record $1.77.

A major contributor was continued strength in cloud AI deployments. Management noted that data-center royalty revenues more than doubled year over year, fueled by hyperscaler adoption of Arm-based server CPUs, networking chips, DPUs and SmartNICs. ARM also highlighted that it now commands nearly 50% share among top hyperscaler cloud compute deployments.

Licensing Business Remains Exceptionally Strong

Licensing revenues rose 29% year over year during the quarter to $819 million, reflecting strong customer demand for next-generation compute architectures and ARM’s Compute Subsystems (CSS). Annualized contract value, a key indicator of underlying licensing momentum, grew 22% year over year.

Management signed two additional next-generation CSS agreements during the quarter, including one tied to smartphone chips and another for data-center networking silicon. The company also expanded strategic partnerships globally, including an AI technology collaboration with the Indonesian government.

Importantly, Arm Holdings’ licensing momentum suggests customers are increasing long-term commitments around AI infrastructure, custom silicon and edge AI deployments.

ARM AGI CPU Could Become a Massive Growth Driver

The biggest strategic development this quarter was the growing traction surrounding the Arm AGI CPU platform. Management revealed customer demand across fiscal 2027 and 2028 now exceeds $2 billion, more than double the level discussed during the company’s March Arm Everywhere event.

The AGI CPU platform is designed specifically for agentic AI workloads, where CPUs increasingly coordinate tasks, move data, manage memory, enforce security and orchestrate AI accelerators. Management believes data centers may eventually require more than four times the current CPU capacity as agentic AI scales globally.

Arm Holdings expects the AGI CPU business alone to generate $15 billion in annual revenue by fiscal 2031. Combined with its projected $10 billion IP business opportunity, management sees a path toward $25 billion in long-term revenue potential.

The platform is already attracting major ecosystem support. Partnerships and deployments now include hyperscalers and AI leaders such as Meta Platforms, Google Cloud, Amazon Web Services, NVIDIA, Microsoft Azure, Cloudflare and SAP

Management emphasized that Arm-based CPUs are rapidly becoming central to AI infrastructure economics because of superior performance-per-watt efficiency. Google recently replaced x86 host processors with custom Arm-based Axion CPUs in TPU deployments, improving performance while lowering power consumption substantially.

Margin Expansion and Profitability Remain Impressive

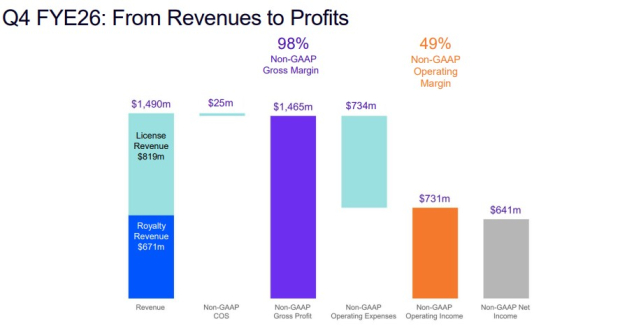

Arm continued demonstrating strong operating leverage despite elevated AI investments. Non-GAAP operating income reached $731 million during the quarter, representing an operating margin near 49%.

Image Source: ARM

Image Source: ARM

Although operating expenses increased 30% year over year due to higher R&D spending, revenue growth comfortably outpaced incremental investments. Management also indicated that operating expenses should grow more slowly than revenues by the end of fiscal 2027, supporting continued margin expansion.

Importantly, the AGI CPU business itself may become profitable relatively quickly. Management suggested incremental operating costs tied to the silicon initiative remain modest because much of the core compute design work already overlaps with Arm’s IP ecosystem.

Guidance Reinforces Confidence in Sustained AI Demand

For the first quarter of fiscal 2027, Arm guided for revenue of approximately $1.26 billion at the midpoint, representing around 20% year-over-year growth. Management also expects both licensing revenues and royalty revenues to grow roughly 20%.

Adjusted EPS guidance of approximately 40 cents also reflects continued investment while preserving strong profitability.

Perhaps more importantly, management repeatedly emphasized that AI infrastructure demand continues to accelerate rather than slow. Executives highlighted growing adoption across hyperscalers, networking infrastructure, edge AI, autonomous systems and physical AI applications.

The company also stated that cloud AI royalty growth should continue at elevated levels throughout fiscal 2027.

Risks Still Exist Despite the Strong Narrative

Even with the exceptional results, some risks remain. ARM’s AI opportunity is attracting enormous investor expectations, which raises valuation sensitivity. Any slowdown in hyperscaler AI spending, cloud deployments, or AGI CPU adoption could pressure sentiment.

Supply-chain constraints also remain a factor. Management acknowledged it is actively securing wafer, packaging, memory, and testing capacity to support rising AGI CPU demand.

Competition in AI infrastructure remains intense as well. Although Arm appears to be gaining architectural share from competitors, rivals continue investing aggressively across CPUs, GPUs and AI accelerators.

Additionally, Arm’s expansion into silicon products introduces execution complexity beyond its historically high-margin licensing model.

Hold Verdict After Earnings

Arm delivered one of its strongest quarters since becoming a public company again, with record revenue, accelerating AI-driven royalty growth, expanding margins and rapidly increasing demand for its AGI CPU platform. The company is clearly evolving into a broader AI infrastructure player with growing exposure to cloud computing, agentic AI, and custom silicon. However, the stock also reflects very high expectations tied to long-term AI adoption and future execution. While Arm Holdings’ strategic positioning remains extremely compelling, aggressive expansion plans and supply-related uncertainties support a balanced approach.

ARM carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Recent Earnings Snapshots

Equifax EFX reported better-than-expected first-quarter 2026 results. EFX’s adjusted earnings per share of $1.86 beat the Zacks Consensus Estimate by 10.1% and increased 21.6% from the year-ago quarter. EFX’s revenues of $1.6 billion surpassed the consensus estimate by 2.3% and improved 14.4% year over year.

Waste Connections WCN posted impressive first-quarter 2026 results. WCN’s adjusted earnings of $1.23 per share outpaced the consensus mark by 3.4% and rose 8.9% from the year-ago quarter. WCN’s total revenues of $2.37 billion beat the consensus mark by 0.7% and increased 6.4% year over year.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).