Can Quanta Justify Its Premium Multiple After a 79% Gain in a Year?

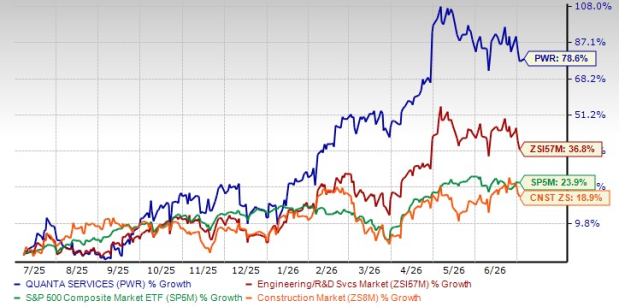

Quanta ServicesPWR has been one of the biggest winners in the infrastructure sector over the past year, with its stock soaring 78.6%. The rally has comfortably outpaced the Zacks Engineering - R&D Services industry's 36.8% gain, the Zacks Construction sector's 18.9% advance and the S&P 500's 23.9% rise. Investors have rewarded the company for consistently delivering strong earnings, expanding its backlog and positioning itself at the center of several long-term infrastructure trends.

PWR Price Performance (1 Year)

Image Source: Zacks Investment Research

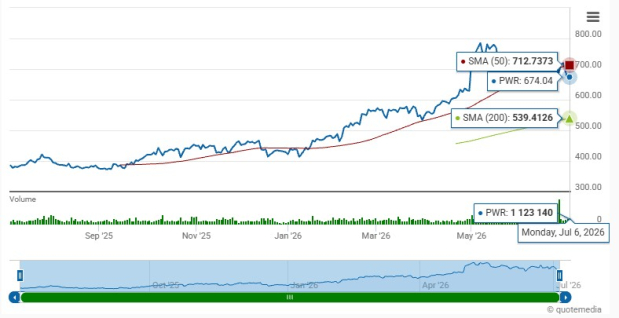

PWR's Technical Trend

Image Source: Zacks Investment Research

The stock's impressive performance, however, has come with a higher price tag. Quanta now trades at a forward 12-month price-to-earnings (P/E) multiple of 44.11X, significantly above the industry average of 29.8X. While Wall Street remains optimistic about the company's long-term prospects, investors now face an important question: Does Quanta's business outlook justify paying such a premium, or has much of its future growth already been priced into the stock?

PWR Valuation (P/E F12M) vs Industry

Image Source: Zacks Investment Research

The answer depends on whether Quanta can continue converting its industry-leading project pipeline into sustained earnings growth while maintaining strong execution. Let's take a closer look at what continues to support the investment case and the factors that could limit further upside.

Quanta's Growth Drivers Remain Strong

Quanta continues to benefit from one of the most attractive infrastructure spending environments in decades. Rising electricity demand, AI-driven data center construction, renewable energy integration, transmission expansion and electric grid modernization are creating significant opportunities across its end markets.

The company has evolved beyond being a traditional contractor into a provider of integrated infrastructure solutions. Its engineering expertise, skilled workforce, fabrication capabilities and supply-chain investments allow it to execute increasingly complex projects for utilities, hyperscalers and industrial customers. This integrated approach has strengthened customer relationships and enabled Quanta to participate earlier in customers' multiyear capital planning cycles.

Management also continues investing to support future demand. The company is expanding transformer manufacturing capacity and nearly doubling its off-site fabrication and logistics footprint, positioning itself to capitalize on accelerating investments in power infrastructure and AI-related projects. These investments should strengthen Quanta's competitive advantage as customers increasingly prioritize execution certainty and supply-chain reliability.

Strong Execution Supports Higher Earnings Outlook for PWR

Quanta's first-quarter 2026 results reinforced confidence in its long-term growth strategy. Revenues increased 26.3% year over year to a record $7.87 billion, while adjusted earnings per share (EPS) climbed to $2.68 from $1.78 in the prior-year quarter. Both the Electric Infrastructure Solutions and Underground & Infrastructure Solutions segments delivered margin expansion, highlighting disciplined project execution and favorable work mix. The company also ended the quarter with a record total backlog of $48.5 billion, providing excellent revenue visibility over the coming years.

Following the strong start to the year, management raised its full-year 2026 outlook. Quanta now expects revenues between $34.7 billion and $35.2 billion and adjusted EPS between $13.55 and $14.25, reflecting improved visibility across its utility, power generation and large-load infrastructure businesses.

Management remains equally optimistic about the longer term. At its recent Investor Day, Quanta outlined a strategy to more than double adjusted earnings power by 2030, supported by an estimated $2.4 trillion addressable market spanning utilities, power generation and large-load infrastructure.

Analysts also remain constructive. Over the past 60 days, the Zacks Consensus Estimate for 2026 EPS has increased from $13.87 to $14.03, representing expected growth of 30.5% from 2025. Revenue estimates point to 22.1% growth in 2026, followed by continued double-digit growth in 2027.

PWR EPS Estimate

Image Source: Zacks Investment Research

PWR Stock’s Premium Valuation Demands Continued Execution

Quanta's biggest challenge today is not demand but valuation. Despite trading below its 50-day moving average, the stock still commands a forward P/E multiple of 44.11X, substantially above the industry average of 29.8X. Such a premium reflects investor confidence that Quanta can sustain above-average earnings growth for several years.

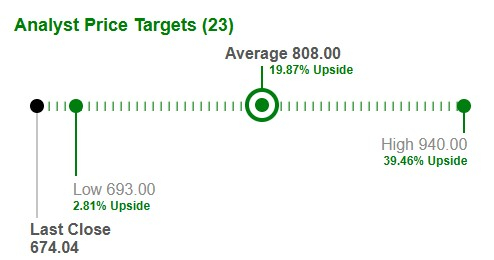

Wall Street's optimism remains evident. The stock carries an Average Brokerage Recommendation (ABR) of 1.37, with 22 of the 27 analysts rating it a Strong Buy. Analysts' average price target of $808.00 also implies roughly 20% upside from current levels.

Image Source: Zacks Investment Research

Nevertheless, premium valuations leave little room for disappointment. Any slowdown in backlog growth, project execution or margin expansion could pressure the stock more than lower-valued peers.

Macro Risks Could Create Near-Term Volatility

Although Quanta's long-term outlook remains favorable, several external factors could influence future performance.

Large infrastructure projects are often subject to permitting delays, regulatory approvals, adverse weather, supply-chain disruptions and changing customer schedules. Inflation, tariffs, labor shortages and higher interest rates may also increase project costs or delay customer capital spending.

Management acknowledged that weather, permitting, regulatory issues, trade policy, supply-chain conditions and broader macroeconomic uncertainty remain important variables affecting project timing and financial performance, even as underlying demand remains robust.

How Quanta Stacks Up Against Competitors

Quanta competes with EMCOR GroupEME, Sterling InfrastructureSTRL and Comfort Systems USA FIX across several infrastructure and mission-critical construction markets.

From a share price perspective, Comfort Systems has delivered the strongest performance, with shares rising roughly 240% over the past year. Sterling Infrastructure follows closely with a gain of 215.9%, while Quanta has advanced 78.6%. Although Quanta has significantly outperformed EMCOR, whose shares have gained 45.5%, it has lagged the exceptional rallies posted by Comfort Systems and Sterling Infrastructure.

Valuation paints a different picture. EMCOR trades at the lowest forward P/E multiple of 25.27X, suggesting a more modest growth premium. Sterling Infrastructure trades at 31.76X, while Comfort Systems commands 37.37X. Quanta's forward P/E of 44.11X is the highest among the four companies, indicating that investors assign the greatest premium to Quanta's earnings visibility, diversified business model and long-term infrastructure opportunities.

Should Investors Buy PWR Stock Now?

Quanta continues to execute at a high level. Record backlog, improving financial guidance, rising earnings estimates and strong demand across electric infrastructure, AI data centers and power generation provide a solid foundation for long-term growth. Management's investments in manufacturing capacity, supply-chain capabilities and integrated solutions further strengthen its competitive position for the coming decade.

However, the stock's premium valuation cannot be ignored. After nearly an 80% gain over the past year, investors are paying a substantial premium for Quanta's quality and growth prospects. While the business fundamentals continue to justify optimism, the current valuation reduces the margin of safety and makes flawless execution increasingly important.

Considering the company's attractive long-term outlook alongside its elevated valuation, the current Zacks Rank #3 (Hold) appears appropriate. Existing investors can remain confident in Quanta's multiyear growth story, while new investors may benefit from waiting for either a more attractive entry point or further earnings growth to better support the premium multiple. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>This article originally published on Zacks Investment Research (zacks.com).