Will Fiber Infrastructure Expansion Enhance Dycom's Growth Prospects?

Dycom Industries, Inc. DY is benefiting from rising fiber infrastructure activity as customers expand fiber-to-the-home networks and invest in long-haul and middle-mile builds. Broader deployment programs across multiple geographies are creating additional work opportunities, while multiyear customer plans provide a favorable backdrop for the Communications segment.

In the first quarter of fiscal 2027, Communications revenues reached $1.57 billion, reflecting organic growth of 24.7% year over year. Growth was driven by ramping fiber-to-the-home programs, higher long-haul and middle-mile fiber infrastructure builds, and expanding maintenance and operations services. Adjusted EBITDA increased 28% to $192.4 million, while the segment margin reached 12.3%. Fiber-to-the-home builds also ramped ahead of expectations during the quarter, aided by expansion into additional geographies and favorable seasonal conditions.

The demand environment extends beyond near-term project activity. Customers are pursuing multiyear fiber-to-the-home and long-haul build programs, pointing to a broader investment cycle across communications networks. Dycom is also expanding its digital infrastructure capabilities, linking outside fiber networks with data center connectivity. This wider service offering could help the company participate across more parts of the infrastructure buildout.

For fiscal 2027, Dycom expects Communications revenues of $6.03 billion to $6.2 billion, implying organic growth of about 12.6% to 15.8% from the prior year. The company also expects modest adjusted EBITDA margin improvement for the segment. With fiber-to-the-home activity ramping and long-haul and middle-mile projects adding another demand source, fiber infrastructure expansion appears positioned to remain an important factor in Dycom's growth prospects.

How Dycom Compares With Key Infrastructure Rivals

Dycom competes closely with MasTec, Inc.MTZ and EMCOR Group, Inc.EME in the infrastructure construction market.

EMCOR operates across electrical and mechanical construction, building services and industrial services markets, with strong exposure to mission-critical facilities and data center construction. The company benefits from broad geographic coverage, execution capabilities and a diversified project portfolio across multiple end markets. However, EMCOR’s business remains tied to the pace of large construction projects and customer capital spending across infrastructure sectors.

Meanwhile, MasTec maintains a diversified infrastructure platform spanning communications, power delivery, clean energy, industrial construction and pipeline markets. The company's broad service offering positions it to benefit from long-term investment trends such as AI-driven data centers, grid modernization and energy infrastructure expansion. At the same time, MasTec remains exposed to variability based on project timing and execution across multiple infrastructure segments.

Dycom's specialization in communications infrastructure and fiber network deployment provides a focused advantage as broadband expansion, fiber connectivity and AI-driven data center interconnection projects continue to grow. Long-standing customer relationships and expertise in wireline network construction support its market position. However, the company's performance remains closely linked to telecommunications investment cycles and customer network spending decisions.

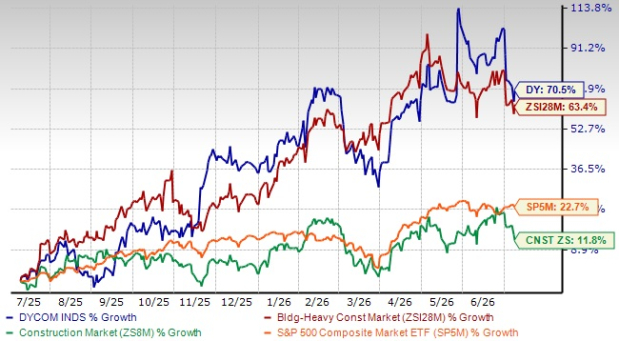

DY Stock’s Price Performance & Valuation Trend

Shares of this North America-based specialty contracting firm have gained 70.5% in the past year, outperforming the Zacks Building Products-Heavy Construction industry, the broader Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

DY stock is currently trading at a discount compared with the industry, with a forward 12-month price-to-earnings (P/E) ratio of 23.81, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of DY

Dycom’s earnings estimates for fiscal 2027 and 2028 have moved upward in the past 30 days to $16.35 and $19.95 per share, respectively. The estimates for fiscal 2027 and 2028 imply year-over-year growth of 36.6% and 22%, respectively.

Image Source: Zacks Investment Research

Dycom currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).