Soft Crude Oil Prices Likely Ahead: What it Means for ExxonMobil

According to data from OilPrice.com, the price of West Texas Intermediate (WTI) crude is trading above $60 per barrel, down significantly from the year-ago level. The pricing environment was relatively more favorable a year ago, therefore hurting the upstream business of integrated energy players like Exxon Mobil Corporation XOM.

EIA projects the spot average West Texas Intermediate price for 2026 at $52.21 per barrel, lower than $65.40 for 2025. With XOM generating a king's size of its earnings from upstream operations, can it combat the prevailing softness in oil prices?

The advantageous assets where XOM is operating include the Permian, the most prolific basin in the United States and offshore Guyana resources. Although the assets have cost advantages, lower oil prices are likely to hurt profits. However, unlike many other companies, ExxonMobil can rely on its strong balance sheet.

XOM’s exposure to debt capital is significantly lower than that of the composite stocks belonging to the industry. The integrated energy giant can lean on its robust financials to navigate the low pricing environment, such as securing debt capital on favorable terms when the business scenario turns unfavorable.

CVX & EOG Can Also Brave Business Uncertainty

Chevron CorporationCVX and EOG Resources IncEOG are two leading energy companies with a strong presence in exploration and production activities. The softness in crude prices is also hurting the bottom line of both CVX and EOG.

Like XOM, CVX and EOG have strong balance sheets. Debt to capitalization of Chevron and EOG is relatively lower than the industry, suggesting a considerably lower exposure to debt capital. Hence, they can brave the uncertainty of the business environment.

XOM’s Price Performance, Valuation & Estimates

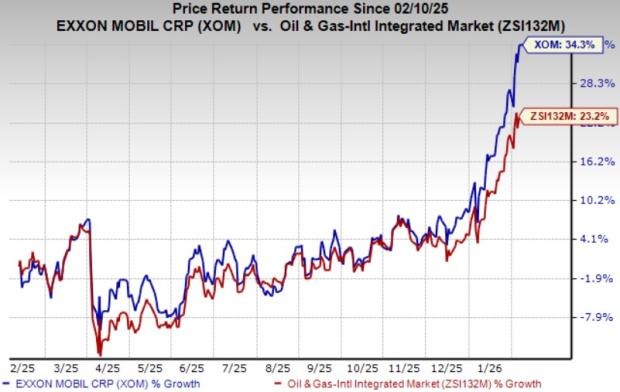

Shares of XOM have gained 34.3% over the past year compared with the 23.2% improvement of the composite stocks belonging to the industry.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

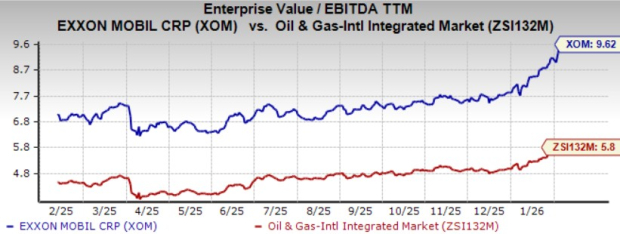

From a valuation standpoint, XOM trades at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 9.62X. This is above the broader industry average of 5.80X.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for XOM’s 2026 earnings has seen upward revisions over the past seven days.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

ExxonMobil currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chevron Corporation (CVX): Free Stock Analysis Report

Exxon Mobil Corporation (XOM): Free Stock Analysis Report

EOG Resources, Inc. (EOG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).