03/23/2026 ValuEngine Weekly Market Summary & Commentary

Weekly Market Recap – Week Ending March 20, 2026

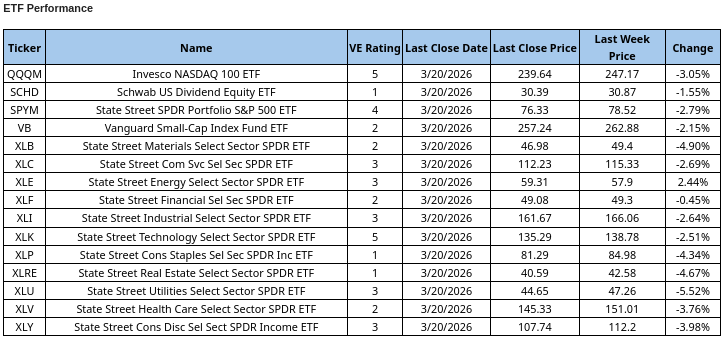

Markets experienced broad-based weakness this week, with most major ETFs and sector benchmarks declining as investor sentiment remained pressured by persistent inflation concerns and heightened geopolitical uncertainty. Growth-oriented indices such as the Invesco NASDAQ 100 ETF and broader market proxies like the State Street SPDR Portfolio S&P 500 ETF posted notable losses, while defensive sectors also failed to provide meaningful downside protection. Energy remained a relative outlier, supported by ongoing macro tailwinds, but overall market action reflects a cautious and risk-off environment where volatility continues to dominate investor positioning.

Trade ValuEngine supported portfolio strategies, www.ValuEngineCapital.com

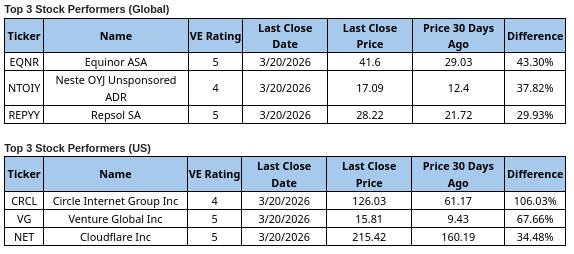

In the below tables we use major ETF’s as a proxy for some major indexes as well as each of the sector groups into which we divide the overall markets. Tracking these over time provides a more defined picture of the US markets than simply tracking major indexes. This is followed by notable individual stock movers over the past month, and finally our full strategy outlook.

Free Trial: Direct Access to ValuEngine Research on over 5,000 stocks and 700 ETFs HERE

Friday March 20 was a “triple-witching” event for options and futures expiration dates. Normally, that is a bullish sign for the markets. Nothing seems normal to most market participants at the moment. Perceived USA-instigated geopolitical chaos combined with a throng of economists warns that the inflationary ramifications will last longer and be higher than the Administration had indicated and any of them had previously imagined.

This is a dramatic shift away from the 7-month trend where the market had taken the cash flows of growth stocks to focus on value and non-mega-cap stock opportunities. Typically, this type of thematic market is rife with “panic selling” (although some might argue that in seemingly unprecedented environments such as this one, panic might be a logical response). We can discuss strategies that different types of investors might wish to consider.

Of course, accounts, funds and ETFs that need to be close to 100% invested by charter or prospectus will use sector rotation strategies to sell holdings in industries and sectors that have the most to lose in runaway inflationary environments. Specifically, the sectors generally considered most vulnerable include: Construction & Building Materials; Transportation & Logistics; Consumer Discretionary & Retail; Restaurants & Hospitality; and Manufacturing & Consumer Durables. The proceeds from such sales are usually reallocated to sectors that benefit and/or are least harmed from this environment. The sectors that actually benefit are Oil and Energy as well as Materials and Mining. When runaway inflation is accompanied by the drumbeats of war, Aerospace/Defense generally profits as well.

Those who follow this column know that there is a daunting consideration in shifting more assets into these three groups at this time. Our valuation model has the stocks and ETFs serving all three sectors rated among the most overvalued. Since these movements are cyclical, there will come a time that these shifts will reverse so active investors and market timers had best make plans to be very nimble. Less overvalued sectors to consider that are much less negatively impacted by inflation are: Finance; Healthcare; Utilities and Consumer Staples. As usual, buy-and-hold investors with at least a 10-year horizon are generally advised to ignore these shifts.

Sector shifting is not for everybody, especially when it comes to taxable investors with huge amounts of embedded capital gains. Many of these investors do not want to sell their existing positions but still want to hedge their exposures during what could be periods of protracted negative volatility. The most efficient way of doing this for large investors is to sell quarterly or monthly S&P 500 Index Futures. Not all investors have access to futures accounts or are equipped to handle them operationally. This is why most of today’s investors (by # of investors, not $) use inverse and even leveraged inverse ETFs to hedge a portion of their long exposure to stocks without having to sell and trigger capital gains.

We mention these products because over the years many investors who have gone this route, especially with the leveraged inverse products by ProShares, have reported disappointing results relative to expectations. SH is the ProShares Short S&P 500 ETF and SDS is the UltraShort S&P 500 ETF. Suppose you buy SDS on March 23 with the index at 6506 and sell it on June 23 with the index at 5204.8, down 20%. You might expect to have gained 40% on the sale of your position, before taxes of course. Odds are very high that you would be very disappointed.

Here is why:

- There is a daily reset mechanism. These ETFs reset their exposure to the benchmark daily to achieve their target inverse or leveraged inverse return. This means the 2x/3x inverse performance is only guaranteed for a single trading day, not over a week or month.

- There is a compounding effect known as volatility decay. When an index fluctuates up and down (volatile market), the daily compounding of returns causes the leveraged ETF to lose value even if the underlying index finishes lower than when the holding began. If an index drops but is very volatile, a 2x UltraShort fund may actually lose value due to the mathematical drag.

- These funds are expensive with an expense ratio of 0.91%. Compare that with the 0.02% that StateStreet SPDR S&P 500 Portfolio ETF, SPYM, charges for long-only exposure. The costs of trading these derivatives daily, combined with high management expense ratios, eat into the returns. Adding to these costs is the fact that daily re-balancing means the fund manager must sell or buy securities at the end of every day, incurring transaction costs and potentially locking in losses.

There is one other risk involved routinely with futures contracts called contango. This means that new daily contracts become more and more expensive with each passing day that the future gathers momentum. Under these circumstances, the ETF loses money as it rolls positions to the more expensive contracts.

All of this information is not intended to make the reader avoid using these instruments. They are efficient vehicles for hedging long exposures on a daily or even weekly basis. For longer holding periods, selling index options might be another course of action to consider. Finally, those currently holding Southwest Airlines (LUV) or Trivago Inc. (TRVG) should be made aware that both have just been downgraded to 2 (Sell) in the ValuEngine system.

In summary, these are challenging times. Hence, we were motivated to provide an educational rundown of choices to consider that is considerably longer than our usual strategy update in this space. We hope you found it useful.

www.ValuEngine.com (

www.ValuEngineCapital.com (

BLOG.VALUENGINE.COM for the full history of ValuEngine.com financial blog posts

____________________________________________________________________________

Existing subscribers alert: ValuEngine has launched a completely redesigned and new website! Please check it out at www.ValuEngine.com

Free trials available for new subscribers. Over 4,200 stocks and 600 ETFs covered.

Full Two Week Free Trial HERE

5,000 stocks, 600 ETFs, 16 sector groups, and 140 industries updated on www.ValuEngine.com.

Financial Advisory Services based on ValuEngine research available through www.ValuEngineCapital.com