VG vs. EQT: Which Natural Gas Stock Is the Better Buy Now?

In the energy space, Venture GlobalVG and EQT CorporationEQT highlight two fundamentally different business approaches. Over the past year, Venture Global stock has climbed 41.7%, outperforming both the broader subindustry’s 24.4% rise and EQT’s 20.3% gain. That said, price performance alone is not a sufficient indicator of long-term investment merit.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

A more meaningful comparison requires examining underlying business models, earnings visibility and exposure to macroeconomic forces. EQT primarily operates as a prominent natural gas producer in the Appalachian Basin, making its outcomes closely tied to domestic gas price movements. Venture Global, on the other hand, is focused on liquefied natural gas (LNG) exports, positioning it more directly within global energy trade flows.

EQT Set for Long-Term Growth, Near-Term Constraints Remain

The global transition toward cleaner energy sources continues to strengthen the long-term outlook for natural gas. Increased adoption of gas as a replacement for coal, along with rising energy demand from data centers and artificial intelligence infrastructure, is expected to support sustained demand growth. EQT, given its scale and resource base, is well-positioned to benefit from these structural tailwinds.

At the same time, global LNG markets remain supportive amid geopolitical uncertainty and tightening supply-demand balances. While EQT has some exposure to LNG markets, its core operations are still linked to domestic pricing benchmarks, which limit its ability to fully capitalize on stronger international pricing.

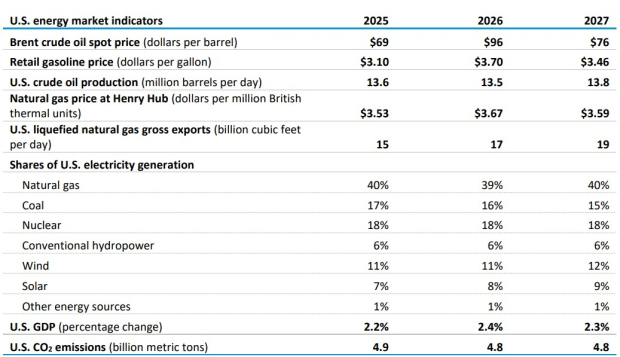

Per the EIA’s April 2026 outlook, Henry Hub natural gas prices are expected to average $3.67/MMBtu in 2026, slightly higher than $3.53/MMBtu in 2025. Meanwhile, U.S. LNG exports are projected to remain near capacity at around 17 Bcf/d, reflecting robust global demand. Although these trends support the broader industry, EQT’s earnings remain somewhat constrained by relatively stable U.S. prices compared to more volatile global markets.

While the company is pursuing greater exposure to LNG-linked pricing, much of the associated benefit is likely to materialize later in the decade, creating a timing mismatch between favorable long-term fundamentals and near-term earnings realization.

Image Source: Energy Information Administration (EIA)

Image Source: Energy Information Administration (EIA)

Venture Global’s LNG Expansion Provides Growth Visibility

Venture Global has emerged as a rapidly expanding LNG exporter, supported by multiple large-scale projects at different stages of development. Its Calcasieu facility is operational, Plaquemines is in the commissioning phase, and the CP2 project is under construction, providing a clear pathway for capacity growth.

A key differentiator is the company’s modular construction strategy, which allows for faster execution compared to traditional LNG developments. This approach enables earlier production timelines and has allowed Venture Global to generate cash flows even during the commissioning phase through early cargo sales.

The company also benefits from a strong base of long-term contracts, totaling approximately $134 billion and typically spanning around 20 years. These agreements provide stable cash flows through a mix of fixed liquefaction fees and market-linked pricing, offering both downside protection and participation in favorable pricing environments.

Valuation Snapshot

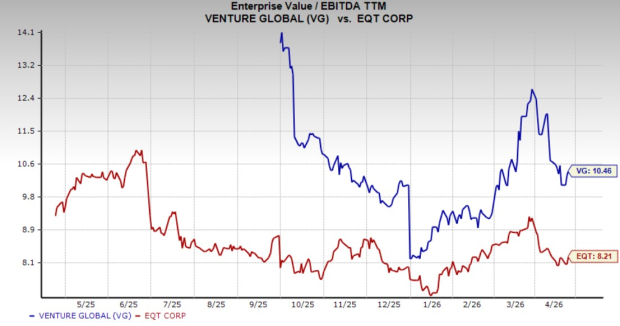

From a valuation standpoint, Venture Global trades at a premium relative to EQT. The stock currently carries a trailing 12-month EV/EBITDA multiple of 10.46 compared to EQT’s 8.21. This premium suggests that investors are assigning a higher value to Venture Global’s growth potential and more predictable cash flow profile.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Final Takeaway

Both Venture Global and EQT are positioned to benefit from the evolving global energy landscape, particularly the growing role of natural gas.

Given the current environment, the best bet now is Venture Global, which currently carries a Zacks Rank #2 (Buy). Those who have already invested in EQT can hold on to the stock. It currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).