How Strong Are Ford Pro's Fundamentals Amid 2026 Pressures?

Ford Motor Company’s F Ford Pro segment continued to demonstrate its role as a major profit driver for the company, generating more than $66 billion in revenues and $6.8 billion in EBIT with a double-digit margin in 2025. This performance came despite challenges such as tariffs, production disruptions linked to Novelis, normalization in U.S. industry pricing in more commoditized segments like government and delivery vans and a difficult macroeconomic and regulatory environment in Europe, where the business still recorded market-share gains, per the company’s fourth-quarter 2025 earnings transcript.

In the United States, the Transit posted record sales, rising 6% year over year in 2025, while Super Duty achieved its strongest sales in more than two decades, increasing 10%. Ford Pro has also continued to evolve its operations by diversifying revenue streams and expanding its high-margin service infrastructure, with paid software subscriptions growing 30% year over year in 2025.

Ford Pro EBIT in 2026 is expected to be in the range of $6.5 billion to $7.5 billion compared to $6.84 billion in 2025. In North America, Ford anticipates continued market-share growth in an industry that is expected to remain relatively flat, supported by conquest sales and a diversified customer base comprising roughly one-third large corporations, one-third small and medium-sized businesses and one-third government and rental fleets.

Ford Pro is strengthening its long-term durability by expanding its mix of profitable software and physical services globally through targeted customer strategies, demand-generation initiatives and specialized solutions. However, despite improving underlying fundamentals, the company expects 2026 results to face near-term pressure from the impact of Novelis-related issues, the ramp-up of the Oakville facility to increase Super Duty capacity in Canada and a tougher regulatory environment in Europe. F carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

F’s Price Performance, Valuation and Estimates

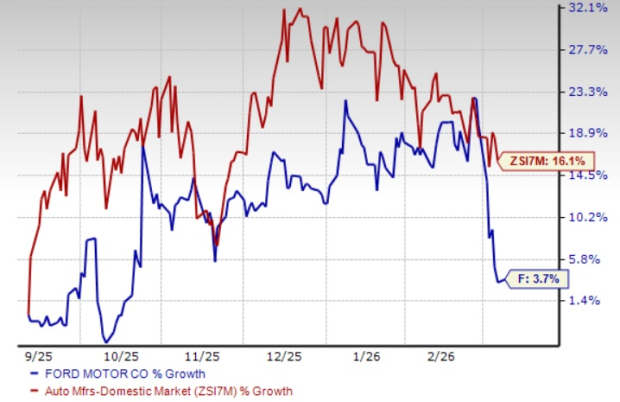

Ford has underperformed the Zacks Automotive-Domestic industry, General Motors CompanyGM and Tesla TSLA in the last six months. Its shares have gained 3.7% compared with the industry’s growth of 16.1%. Shares of General Motors and Tesla have gained 27.2% and 8.1%, respectively, during the same period.

Image Source: Zacks Investment Research

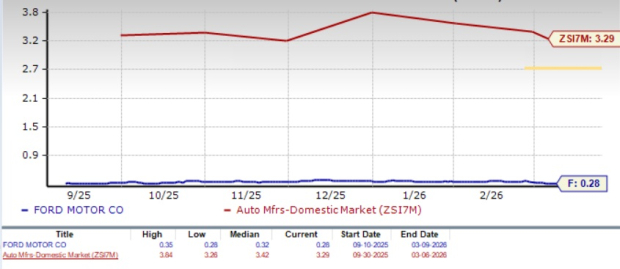

From a valuation perspective, F appears undervalued. Going by its price/sales ratio, the company is trading at a forward sales multiple of 0.28, lower than the industry’s 3.29. General Motors and Tesla are trading at forward sales multiples of 0.36 and 14.24, respectively.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Ford’s 2026 EPS has moved down a penny in the past 30 days. The Zacks Consensus Estimate for F’s 2027 EPS has moved up 4 cents in the past seven days.

Image Source: Zacks Investment Research

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ford Motor Company (F): Free Stock Analysis Report

General Motors Company (GM): Free Stock Analysis Report

Tesla, Inc. (TSLA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).