Is SJM Stock a Value Buy or a Neutral Consumer Staples Pick

The J. M. Smucker Co. SJM offers a familiar consumer staples mix: discounted earnings valuation, sizable free cash flow and brands with room to grow.

The stock still stops short of a clear buy case. Fiscal 2027 sales visibility is weak, and parts of the portfolio need cleaner execution before investors can lean more aggressively into the valuation gap.

The J. M. Smucker Company Price, Consensus and EPS Surprise

The J. M. Smucker Company price-consensus-eps-surprise-chart | The J. M. Smucker Company Quote

Why SJM Looks Cheap on Earnings

SJM trades at 11.7X forward 12-month earnings, below 14.14X for the Zacks sub-industry, 16.91X for the broader Zacks sector and 21.76X for the S&P 500.

That discount is not isolated. Over the past five years, the stock has traded between 9.11X and 18.27X, with a median of 12.33X. The $123 price target reflects 12.4X forward 12-month earnings, leaving the stock framed as inexpensive but not deeply mispriced.

How Smucker Cash Flow Supports the Case

Cash generation gives SJM one of its better supports. Fiscal 2026 free cash flow reached $1.2 billion, up from $816.6 million in the prior year, while cash from operations rose to $1.5 billion.

That helped fund $720 million of debt repayment and $464.7 million of dividends. Management also projects about $1 billion of free cash flow in fiscal 2027 and expects net debt to adjusted EBITDA to move toward about 3X by fiscal year-end, improving flexibility after the Hostess acquisition.

Where SJM Still Has Growth Engines

The bullish case is not only about valuation. Uncrustables reached $1 billion in annual sales, added about 3 million households over the past year and still has household penetration of only 27%.

Cafe Bustelo gives the coffee portfolio a faster-growing platform, while Away From Home adds channel diversification across schools, workplaces, healthcare, lodging and convenience stores. General Mills Inc.GIS and The Kraft Heinz CompanyKHC remain relevant packaged-food comparisons because investors are also weighing mature brands against category growth and execution quality.

Image Source: Zacks Investment Research

Why Smucker Still Deserves Caution

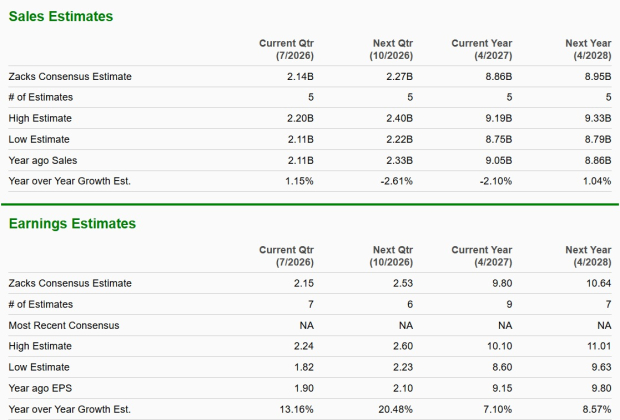

Fiscal 2027 net sales are expected to decline 3-4%, reflecting lower net price realization and weaker volume/mix. That matters because fiscal 2026 growth relied heavily on pricing, while fiscal 2027 needs broader volume progress.

Sweet Baked Snacks remains the clearest issue. Fiscal 2026 segment sales fell 18%, and fourth-quarter sales still declined 5%. Pet Foods is uneven as well, with Meow Mix growth offset by weaker dog snacks. Higher selling, distribution and administrative expenses, projected to rise about 5%, may also limit operating leverage.

What Makes SJM a Hold Rather Than a Buy

SJM has enough support to avoid a bearish call. The valuation is below peer and market benchmarks, cash flow is healthy, debt reduction is visible and priority brands still give management credible growth levers.

The buy case needs better top-line proof. Until lower pricing, mixed volume trends, Sweet Baked Snacks weakness and pet recovery risk look more contained, SJM fits a neutral consumer staples setup rather than a more aggressive value call.

How SJM Signals Could Confirm the Stance

The bottom line is balanced. SJM’s discounted valuation and cash generation support patience, but weak sales visibility and portfolio repair keep the investment case from becoming decisively constructive.

Investors would naturally compare the Neutral framing with the stock’s current Zacks Rank and Style Scores. A favorable Value Score would reinforce the valuation angle, while the Growth Score, Momentum Score and VGM Score would help indicate whether growth quality and market timing support the same view. The Zacks Rank remains the first screen for near-term earnings estimate trends, with Style Scores serving as complementary signals rather than stand-alone reasons to buy.

SJM currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).