The Investment Case for Tesla After $4.3B Team-Up With LG Energy

In a bid to further boost its thriving energy storage business, TeslaTSLA is collaborating with South Korea’s LG Energy Solution to buy $4.3 billion worth of lithium iron phosphate (LFP) battery cells. These cells will be manufactured in the Lansing, MI, factory, starting in 2027.

The facility was originally part of a joint venture between General MotorsGM and LG Energy. However, as General Motors scaled back EV investments amid slower-than-expected adoption, it exited the project, allowing LG Energy to repurpose the plant for new customers like Tesla.

The rationale behind Tesla’s deal with LG Energy is to secure a domestic battery supply and reduce reliance on China. Tesla’s energy storage business is increasingly exposed to tariffs on imported batteries. Without a local supply of LFP cells, the company would either have to absorb higher costs or pass them on to customers, both of which could hurt growth.

The partnership ensures American-made LFP cells will power Tesla’s Megapack 3 systems. By locking in domestic supply, Tesla is directly addressing a key bottleneck — battery availability — while improving cost visibility. If executed well, this could make its energy segment an even more compelling part of its long-term growth story.

But does this deal make Tesla stock worth buying right now? Let’s take a closer look.

TSLA’s Energy Storage: The Real Growth Story

Tesla’s energy generation and storage business is emerging as a major growth engine, driven by strong demand for Megapack and Powerwall systems. Over the past three years, energy storage deployments have grown at a remarkable 168% CAGR.

This momentum comes as electricity demand surges, particularly from data centers and AI infrastructure. In 2025, Tesla reported record deployments of 46.7 GWh, up 49% year over year. Growth is expected to continue with the rollout of Megapack 3 and the new Megablock solution, both set to be produced at Tesla’s Houston Megafactory.

To support this expansion, Tesla has been aggressively securing battery supply. In late 2025, it signed a $2.1 billion deal with Samsung SDI for LFP cells produced in Indiana.

Combined, Tesla’s agreements with LG Energy and Samsung SDI represent more than $6.4 billion in committed battery supply. This underscores strong confidence in the long-term trajectory of its energy storage business. The company also expects to recognize $4.96 billion in deferred revenue this year from ongoing energy projects, more than double 2025 levels.

Financially, the segment is delivering solid results. Energy generation and storage revenues rose to $12.7 billion in 2025, up 27% year over year, accounting for 13% of total revenues versus 10% in 2024. Gross profit climbed to about $3.8 billion, up 44%, with margins near 30%, making energy Tesla’s highest-margin business.

Tesla’s EV Slowdown and AV Ambitions Raise Risks

While Tesla is gaining traction in energy storage, its core EV business is under pressure. Deliveries declined for the second straight year in 2025, falling more than 8% after a 1% dip in 2024, reflecting softer demand and intensifying competition.

Against this backdrop, CEO Elon Musk is repositioning Tesla as a broader technology company, with a growing focus on AI, autonomous driving and robotics. However, the company faces formidable competition in autonomy, where it lags Alphabet’s GOOGL Waymo.

Waymo operates at Level 4 autonomy, enabling fully driverless operation in select areas. Tesla, by contrast, remains at Level 2, which still requires active driver supervision. The gap is also evident in scale. Tesla’s fleet has logged nearly 700,000 paid miles to date (as highlighted in the last earnings call), while Waymo is already delivering more than 450,000 paid rides per week in the United States, underscoring a significant technological and operational lead.

At the same time, Tesla is ramping up investments aggressively. Capital expenditures are expected to exceed $20 billion in 2026, sharply higher than about $8.5 billion last year. With EV growth slowing and contributions from AI and robotaxis still years away, this raises near-term financial pressure and execution risk.

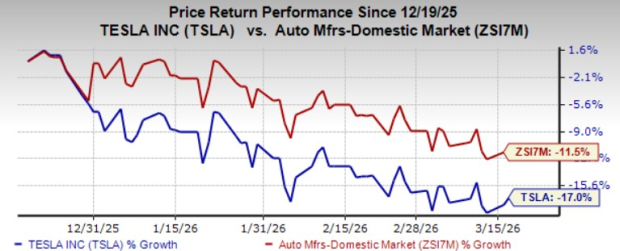

TSLA Price Performance, Valuation & Estimates

Over the past three months, shares of Tesla have declined 17%, underperforming the industry.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

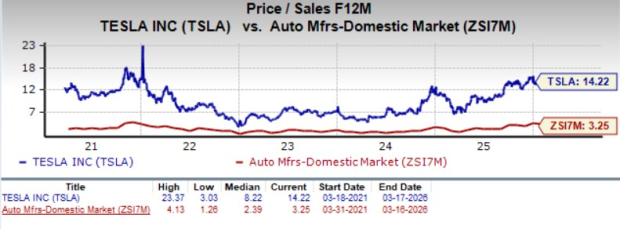

Based on its price/sales ratio, the company is trading at a forward sales multiple of 14.22, way higher than the broader industry and its own 5-year average. Tesla’s valuation has historically remained disconnected from near-term fundamentals, but that does not eliminate downside risk. Much of the optimism surrounding its long-term autonomy and AI bets is already priced in. TSLA carries a Value Score of F.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Tesla’s EPS has been southbound over the past 90 days.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Our Take

Tesla is clearly building a compelling long-term narrative, with its energy storage business emerging as a high-growth, high-margin pillar supported by improving supply chain visibility. However, near-term risks are hard to ignore. A slowing EV business, rising capital intensity and an uncertain timeline for monetizing AI and autonomous driving keep the risk-reward balanced rather than compelling.

While the LG Energy deal strengthens the energy thesis, it is not enough to offset execution risks elsewhere. With a Zacks Rank #3 (Hold), Tesla warrants patience rather than fresh buying.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

General Motors Company (GM): Free Stock Analysis Report

Tesla, Inc. (TSLA): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).