‘Point of No Return’: Mizuho Says Buy These 2 Energy Stocks Even if Middle East Tensions Ease

Back during the 1991 Persian Gulf War, comedian Jay Leno joked that oil prices had climbed so much that even the price of Oil of Olay had gone up. More than three decades later, the Middle East is once again rattling energy markets, although this time the picture is a bit more complicated.

Claim 55% Off TipRanks

- Unlock trusted, data-backed investing tools with TipRanks Premium, from analyst ratings and forecasts to breaking news and portfolio analysis.

- Discover high-conviction stock picks and new investing opportunities with the TipRanks Smart Investor Newsletter

Yes, crude prices surged when fighting involving Iran escalated and shipping through the Strait of Hormuz came under pressure. While oil has pulled back from its highs, prices remain significantly above pre-war levels as markets continue to weigh cease-fire negotiations, shipping disruptions, alternative export routes, and the risk of renewed escalation. Analysts have repeatedly raised oil forecasts in recent weeks, reflecting expectations that energy flows may take months to fully normalize even if diplomatic efforts eventually hold.

Among them is Mizuho analyst Nitin Kumar, who sees an attractive opportunity in energy stocks given his bullish outlook for oil and natural gas markets.

“The disruption to oil and product markets has exceeded our initial expectations in terms of both magnitude and duration. Critically, the global oil market seems to have gone beyond a point of no return such that even if there is a peace deal by June 30 (our base case), it could take 9 months for oil markets and even longer for product markets to normalize. Meanwhile, despite another weather-driven weak demand quarter for natural gas in 1Q26, both domestic and international gas demand are expected to grow well beyond supply forecasts. Against this bullish commodity outlook, the sector has retraced some of its earlier strength vs. the market, creating an attractive entry point in our view,” Kumar explained.

Kumar goes on to select two energy stocks to buy right now – shares that should continue to gain even if the Middle East tensions ease. As usual, we’ll turn to the TipRanks database to see how his picks stack up against the broader Wall Street consensus. Let’s dive in.

Gulfport Energy(GPOR)

The first Mizuho pick we’re looking at here is Gulfport Energy, one of the US energy industry’s independent oil and gas exploration and production firms. Gulfport, which is headquartered in Oklahoma City, has operations in the Anadarko Basin of its home state and in the Appalachians of eastern Ohio – two of North America’s important hydrocarbon-producing regions.

In the Anadarko Basin, Gulfport has 73,000 net reservoir acres in two segments, Woodford and Springer, of the SCOOP natural gas play. SCOOP is one of Oklahoma’s most important natural gas-producing formations and makes up approximately 19% of the company’s total production. The rest of Gulfport’s production comes from the Utica and Marcellus formations in the Appalachian Basin’s reach into eastern Ohio. Gulfport’s operations cover 208,000 net reservoir acres in the Utica formation and 20,500 net reservoir acres in the Marcellus. Both regions are known as some of North America’s most prolific natural gas production zones.

Gulfport finished 2025 with substantial proved reserves. These came to 4.3 Tcfe and were up 7% over 2024. As of December 31, some 57% of Gulfport’s proved reserves were considered developed.

In the last reported quarter, 1Q26, Gulfport’s revenue came to $437.5 million, up an impressive 122% year-over-year and beating the forecast by $53.7 million. At the bottom line, the company reported a GAAP EPS of $8.87, a figure that was $1.64 ahead of the estimates. The adjusted free cash flow in the quarter came to $118.9 million, a substantial increase from the $36.6 million reported for 1Q25.

Kumar, in his coverage of Gulfport for Mizuho, outlines a company whose operations validate investor interest.

“Although GPOR has screened well relative to gas-focused peers and even SMID-cap oily E&Ps on key metrics, our key concern was overall inventory depth that stood just above ~11 years at the end of F2024 and well below the gas peer average of >20 years. Management has narrowed this gap to peers in 2025 with a combination of organic exploration and a ~$100mm discretionary land spending program that was completed in 1Q26… With the inventory depth overhang mitigated and continuing momentum on efficiencies, we believe investors can focus on the strong FCF profile, resilient balance sheet, and commitment to cash returns via the opportunistic buyback… Given the recent pullback, the stock offers ~45% upside to our relatively unchanged NAV-based price target, making this a compelling entry point in our view,” Kumar opined.

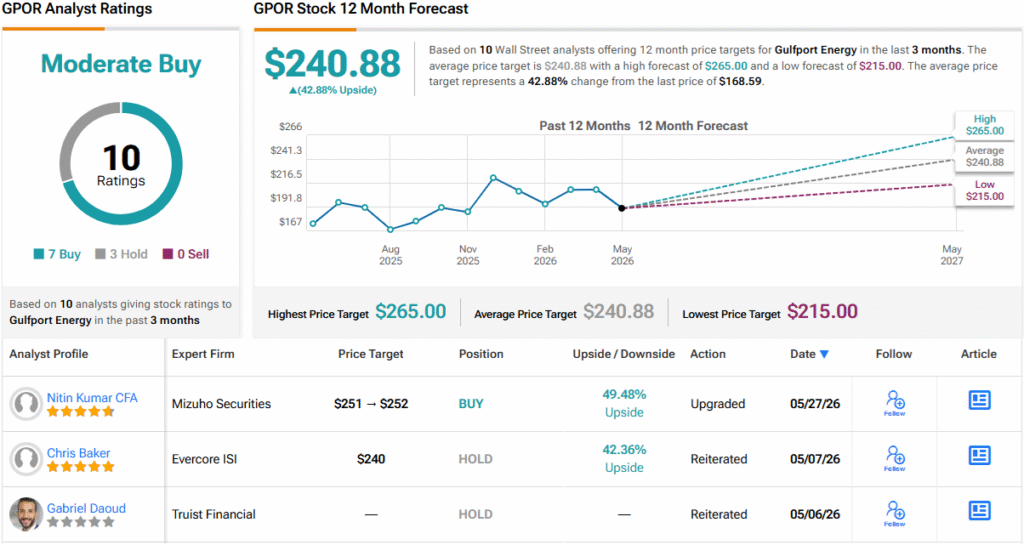

Getting down to the brass tacks, Kumar puts an Outperform (i.e., Buy) rating on the stock, along with a $252 price target. (To watch Kumar’s track record, click here)

Overall, Gulfport gets a Moderate Buy rating from the Street, based on 10 recent reviews that include 7 Buys and 3 Holds. The stock is currently priced at $168.59, and its average price target of $240.88 indicates room for a share price increase of ~43% in the coming months. (See GPOR stock forecast)

Par Pacific Holdings(PARR)

The next stock Mizuho is betting on is Par Pacific, a Houston-based energy company with operations in the Rocky Mountains, Pacific Northwest, and Hawaii. Par Pacific is a $2.8 billion company with three main operational segments: refining, logistics, and retail. In practical terms, the company has a network of refineries, terminals, pipelines, distribution centers, marine terminals, and rail lines, all moving fuel to the people who need it.

The company’s basic statistics tell the story: Par Pacific has 13 million barrels of storage capacity; 219,000 barrels per day of petroleum refining capacity; 549 miles of pipelines; and 121 fuel retail locations. The company operates its retail locations, which include convenience stores, under the 76, Hele, and nomnom brand names.

Refining is the company’s largest segment and generates the largest part of its operating income. Par Pacific owns and operates, among other facilities, the largest refinery in Hawaii, and its refinery segment had operating income in 1Q26 of $56.3 million. Logistics, the second-largest segment, saw operating income of $24.5 million, and the retail side generated operating income of $13 million.

Summing up the company’s performance, the 1Q26 release showed a top line of $1.82 billion, marking a 4.6% year-over-year increase and coming in roughly $40 million better than had been anticipated. The company’s GAAP earnings came to $1.10 per share, marking a solid turnaround from the ($0.57) reported in the first quarter of last year — though on an adjusted basis, EPS of $0.78 missed the $1.03 analyst consensus by $0.25. The company finished the quarter with $172.2 million in cash and other liquid assets.

For Kumar, Par Pacific stands out as a disciplined operator with a history of turning acquisitions and operational improvements into profitable growth.

“Recent results have demonstrated robust profitability and cash generation, reflecting both improved operations and favorable fuel margins in its niche markets. Over time, management has deftly executed acquisitions expanding refining capacity while advancing its own growth projects, while also returning capital via opportunistic share repurchases. Importantly, there is potential incremental value from Small Refinery Exemption outcomes, to which PARR is one of the biggest relative beneficiaries in our coverage. Even though PARR shares have outperformed the group year to date, we still see significant value relative to peers as, even after the rally, PARR trades at a discount on key multiples given its smaller-cap profile,” Kumar commented.

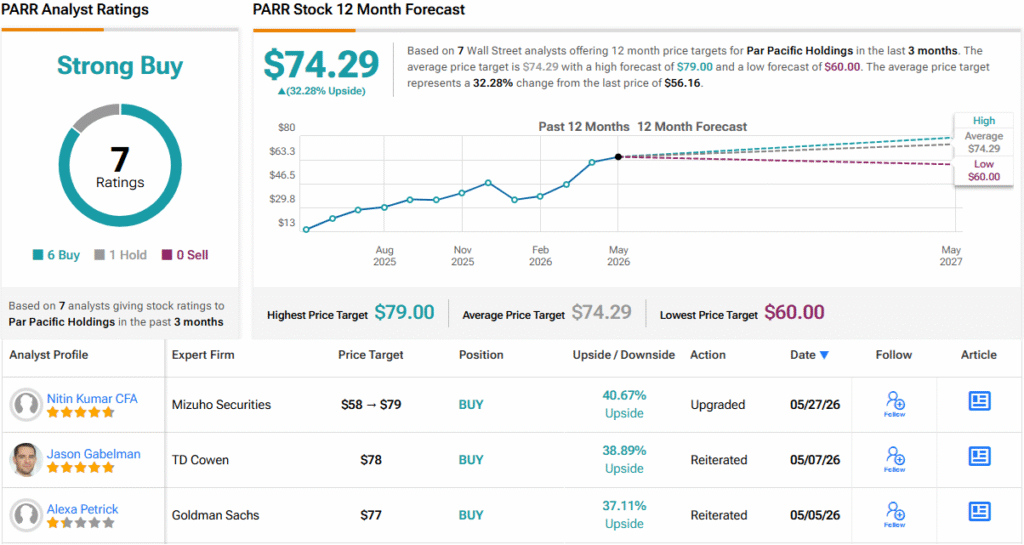

These comments support the Outperform (i.e., Buy) rating from the Mizuho expert, while his $79 price target suggests that the shares will appreciate by ~41% by this time next year.

Kumar’s bullish view is echoed across Wall Street. The stock earns a Strong Buy consensus rating based on 7 analyst reviews, with 6 Buys outweighing a lone Hold. At the current share price of $56.16, the average price target of $74.29 points to potential gains of about 32% in the year ahead. (See PARR stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.